Asian Prices vs European Benchmark

Prices on the Asian market have decreased below the European benchmark for the first time since the US started exporting LNG in 2016.

We can easily observe a drastic fell for the LNG prices since the autumn 2018, and especially on the next friday, according the Financial Times, prices collapse due to the current higher seasonal temperatures as well as the recent restarting of Japan nuclear industries and the storage in North Asia still full.

Also, important buyers mainly located in Japan, Taiwan and India, have decreased their demand of cargo deliveries leading the Asian JKM price to $4.429 per million British thermal units, the lowest since April/May 2016 with $5,86 per million Btu. In that sense, China, an other large LNG buyer, is currently more interested for purchasing LNG forward contracts rather than on the spot market for immediate delivery. Prices have also been affected by rising LNG supply, which grew by 12 per cent in February from a year ago, according to consultants Energy Aspects.

As Asian LNG prices have been at their weakest in three years so far this winter, U.S. cargoes have found home in Europe, which has been the top buyer of U.S. LNG this winter season. Indeed, the market has been inundated with supplies coming onstream from the United States, Russia and Australia.

However, a cyclone heading for north western Australia may disrupt LNG loading there,clearing the loading port at Dampier and Ashburton, according to Pilbara Port Authority.

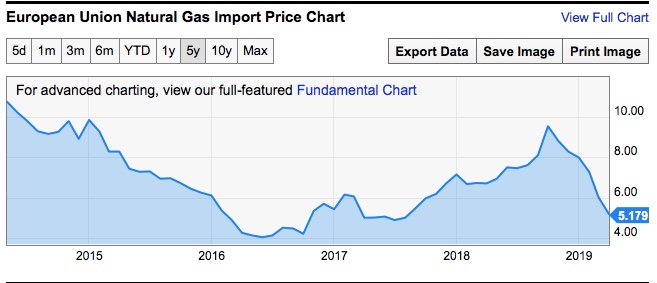

To compare, see below the European LNG benchmark price.

Europe LNG Market is Becoming an increasingly important market.

For some LNG analysts and industry officials, Europe is becoming an important LNG demand market after 2021 especially due to the decline of the natural gas production in northwest Europe, meanwhile that the global LNG supply will growth.

Indeed, the Netherlands is reducing their production at the huge Groningen field, aiming to terminate production by 2030. The UK and Norway may also see drops in natural gas exports.

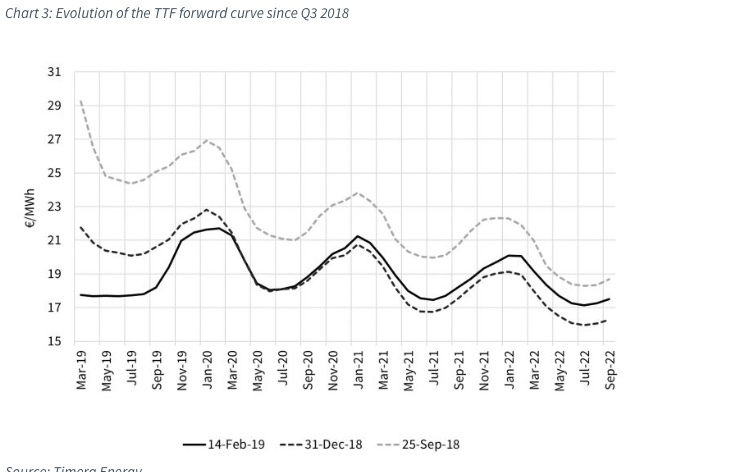

Forward Curve only for European Countries ( Dutch market )

Since December 2018, the futures price falls on the TTF curve ( Title Transfer Facility, is a virtual trading point for natural gas in the Netherlands).

Excepting for a warmer spring than normal, Europeans tend to store gas inventory and so conducting a global decrease of futures prices.

Therefore, we remark a low sharp movement in the front months of the TTF curve.

We can mention that the gas forward curve represents a price indicator for energy prices evolution and futures expectations.

Indeed, the relationship between gas and coal plants in European power markets will be the key price barometer on the European demand side.

Investment of different stakeholders

Chinese state shipbuilding company and Norway-based DNV GL classification society have unveiled a project to develop the world’s largest liquefied natural gas (LNG) carrier with a capacity of 270,000 cubic meters. which will be run on LNG thanks to the royal Dutch shell and tokyo Gas agreement.

Chevron second biggest oil company are investing in unconventional resources in the permian basin, the goal is to use produce 600’000 barrels a day in the end of 2020, and reach 900’000 barrels by the end of 2023 some of that will go to the LNG plant and around the world to serve the growing demande

Source for forward curve :

Other sources :

https://www.ft.com/content/9c485852-4cb6-11e9-bbc9-6917dce3dc6

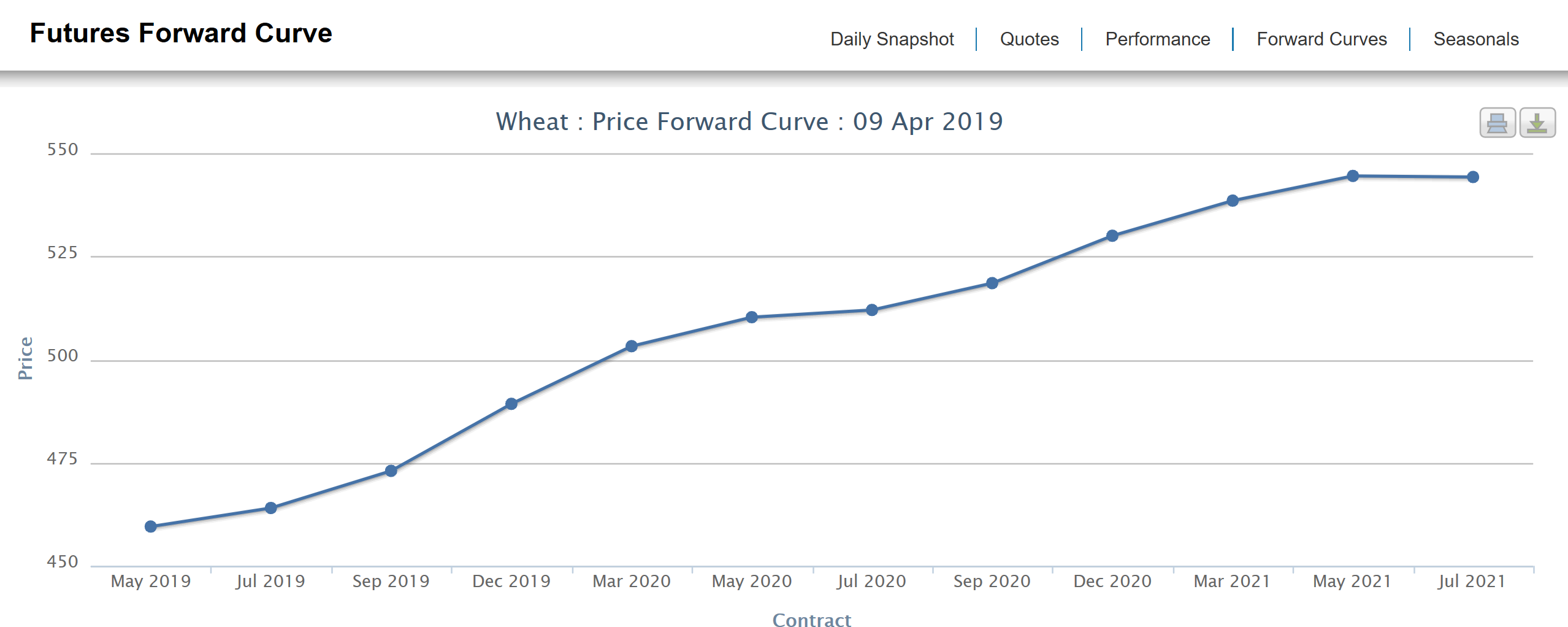

Figure 4: $/bushel

Figure 4: $/bushel