Price Recap

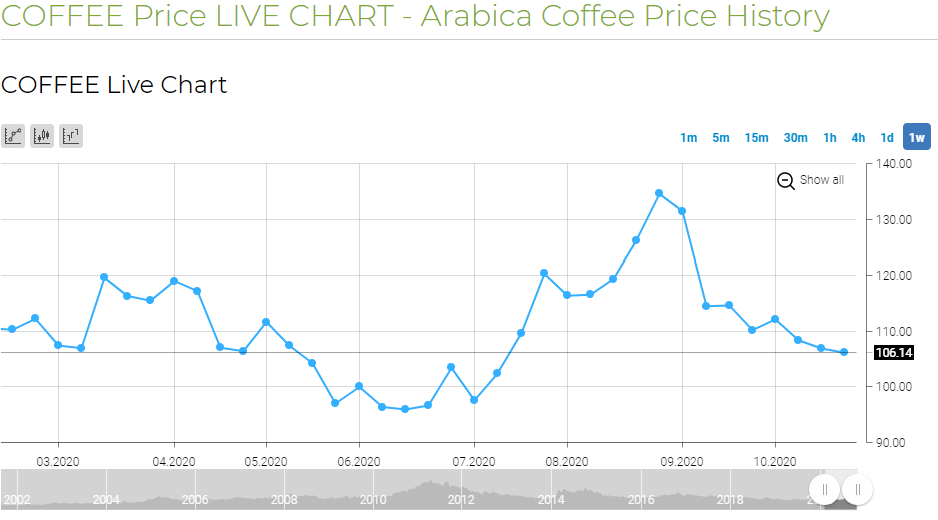

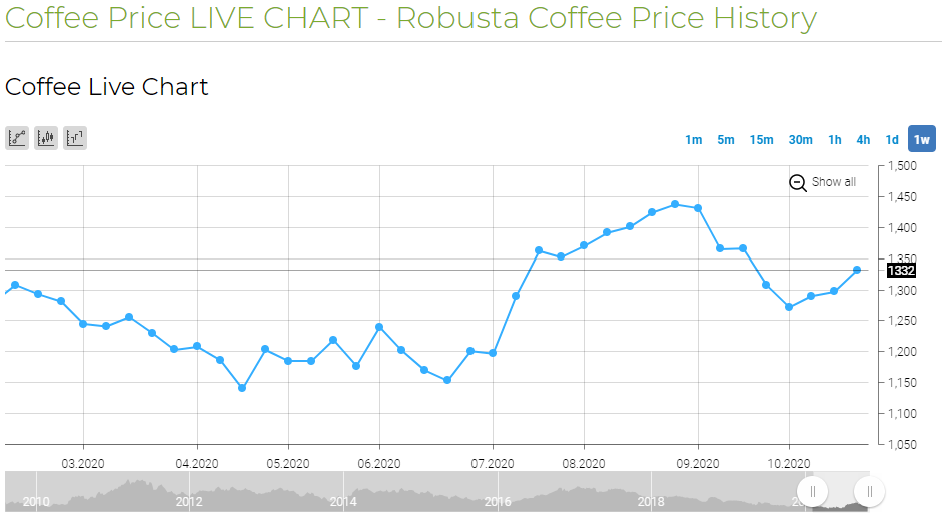

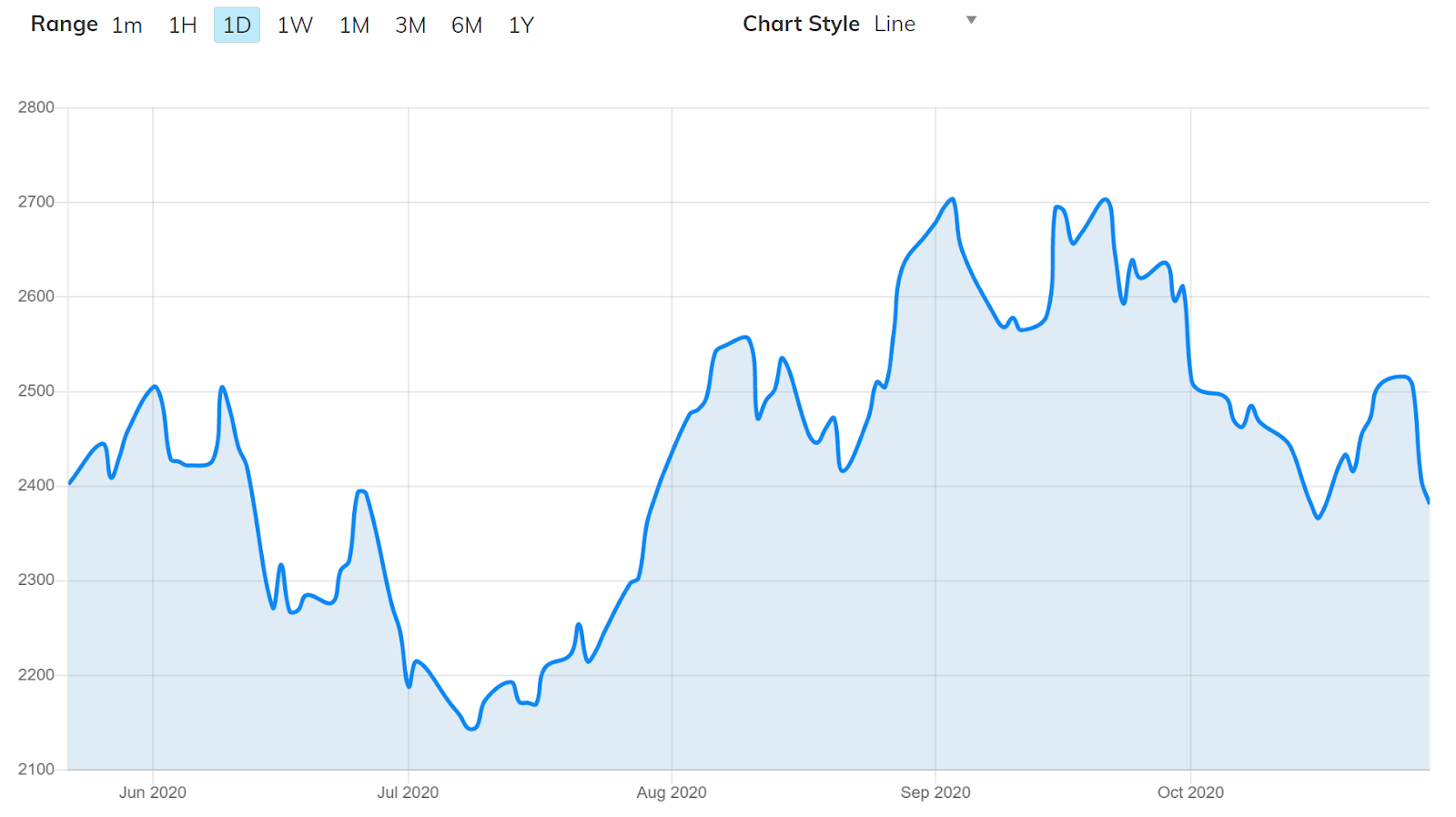

CFDs future Arabica coffee in USD/100 pounds |  CFDs future Robusta coffee in USD/metric ton |

| Source: IFCmarkets | Source: IFCmarkets |

|

| CFDs future cocoa in USD/metric ton |

| Source: Avatrade |

Both commodities, cocoa, and coffee beans experienced sudden drops in price at the end of the last summer. From USD 2703/MT in mid-September, the cocoa fell to USD 2381/MT on the 29th of October (-11.91%). The tendency is even more dramatic for Arabica coffee beans. The price drop reached -21.11% between early-September and end-October. However, Robusta coffee saw its price increase slightly between October 5th and October 29th (+4.95%).

These variations can be explained by the arrival of the second wave COVID-19. For the two last months, the spread among the population gained in intensity and with it the number of restrictions around the world. Naturally, the market is suffering from a demand contraction due to the closure of restaurants, businesses, and the recent lockdowns in several countries.

Futures and Cost Curves

For these two commodity futures, we can notice dramatic changes in December compared to the following months. Regarding the coffee, after the initial December drop, the curve is a contango. About the cocoa, the curve is harder to analyze due to several consecutive months of heavy curve variations.

future coffee in USD/100 pounds future coffee in USD/100 pounds |  future cocoa in USD/metric ton future cocoa in USD/metric ton |

| Source: Barchart | Source: Barchart |

Supply and Demand Dynamic

Coffee

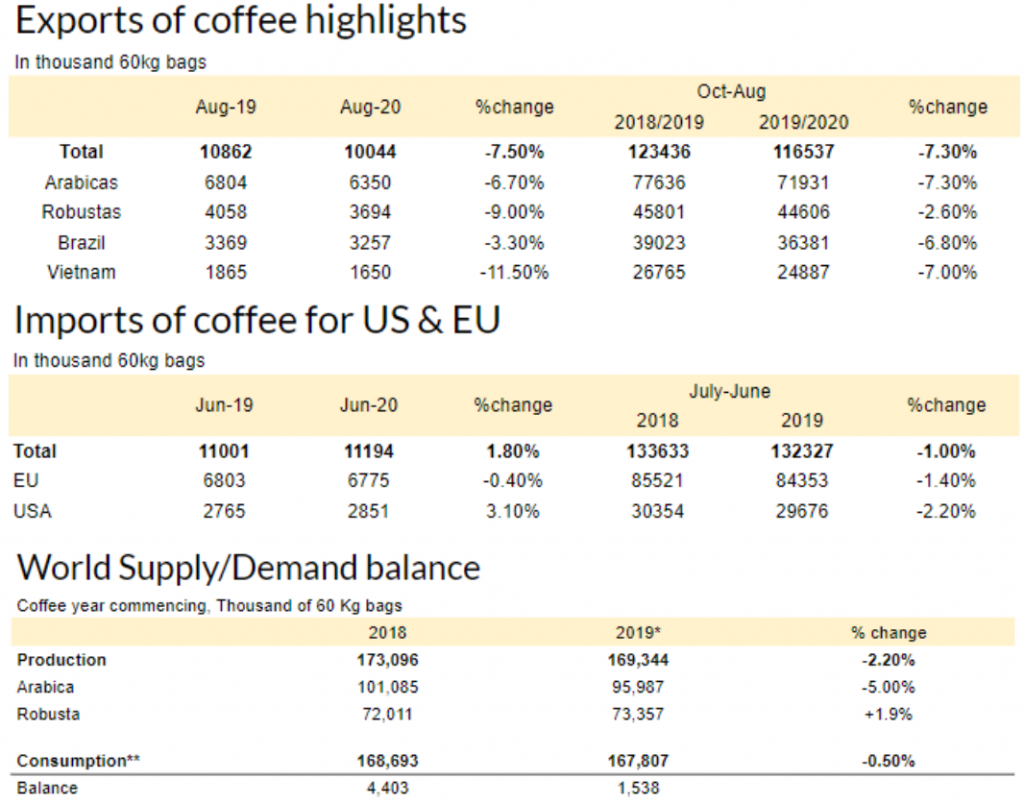

On the supply side, the USDA has revised its forecast for 19/20. The world production is forecasted 2.4 Mio. bags below last December estimate to 166.9 Mio.bags. This is following revised yield due to weather conditions and some damages. Exports are down by 3.4 Mio. Vietnam revised yield accounts for most of the reduction in both production and exportable supplies.

For 20/21 season is set to break records driven by Brazil with an increase of 9.1 Mio bags amounting 176.1 Mio. bags. This surge is based on good weather conditions prevailing in most coffee regions possibly resulting in a higher yield of the harvest.

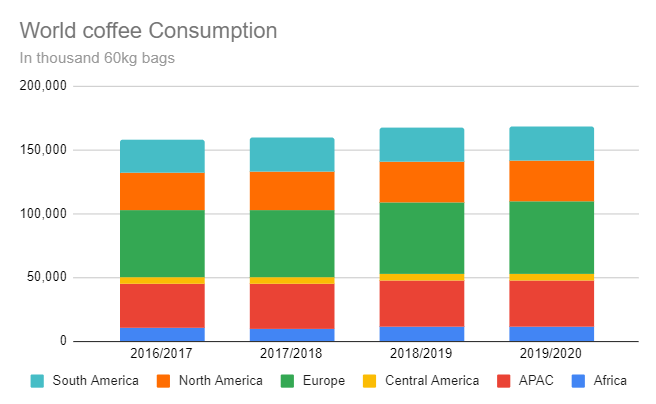

The yearly demand for 2020, both the US and Europe markets have been revised lower due to low consumption and stocks build-up. The US by 1.2 Mio. to 25 Mio. and Europe by 0.5 Mio. to 47.5 Mio.

For 2021, both markets are set to each be up 2.0 Mio. bags from this year latest forecast. The EU would consumption reaches 49.5 Mio. bags. The ending stocks are expected to increase to 14.5 Mio. bags. On the US side, the total import would arise to 27.0 Mio. with ending stocks increasing 0.5 Mio. bags to 7.0 Mio bags. According to the USDA, the coffee market will be in surplus for season 20/21.

Cocoa

At the end of the 19/20 cocoa season, Côte d’Ivoire production reached 2.0 Mio Ton, down 4.8% YoY. The exports are down 2%. The start of 20/21 season, Ghana and Côte d’Ivoire announced a surge in farm gate prices. Up 28% and 21% YoY respectively. There are potential risks in exports linked to end of November election in Côte d’Ivoire.

Demand, based on grinding data, is down 4.7 YoY in EU for 3rd quarter, might indicate that demand is not recovering. This decline is not as important as during the 2nd quarter of 2020 (16.3%). This is attributed to COVID-19 crisis.

Recommendation

Coffee

For coffee, based on falling consumption and production in 2020, the rising stocks in consuming countries as well as low-cost oil, the coffee price is expected to remain stable. For the longer term, the oversupply capacities of producing countries with uncertainties in consumption for the largest market might decrease prices further crossing the 1 USD/lb threshold.

Cocoa

Like coffee, cocoa demand and the pace of re-opening of economies is the critical question. Therefore short term price, as well as long term, is expected to remain stable at 2300-2500 USD/Ton due to exports falling. The backwardation situation might be corrected by COVID-19 with continuous low demand.

Quentin Pilloud, William Béguin & Vincent Stalder

DiscLAIMER

This publication is for your information only and is not intended as an offer, or a solicitation of an offer, to buy or sell any investment or other specific product. The analysis contained herein does not constitute a personal recommendation or take into account the particular investment objectives, investment strategies, financial situation and needs of any specific recipient. It is based on numerous assumptions

reference

Aboa, Ange. “Ivory Coast Struggling To Sell 2020/21 Cocoa Mid-Crop”. Reuters, 2020, https://www.reuters.com/article/instant-article/idUSL8N2HK4BE. Accessed 29 Oct 2020.

Carey N, Naidu R, Cavale S. Coffee, ketchup and Nike Air Max: it’s the COVID consumer economy. Reuters. https://www.reuters.com/article/us-health-coronavirus-consumer-pricing-i-idUSKBN25S4SB. Published 2020. Accessed October 28, 2020.

COFFEE Price Live | Arabica Coffee Price | Arabica Coffee Chart | IFCM. Ifcmarkets.com. https://www.ifcmarkets.com/en/market-data/commodities-prices/coffee. Published 2020. Accessed October 28, 2020.

Coffee Price Live | Robusta Coffee Price | Robusta Coffee Chart | IFCM. Ifcmarkets.com. https://www.ifcmarkets.com/en/market-data/commodities-prices/robusta. Published 2020. Accessed October 28, 2020.

Cocoa CFD – Cocoa Trading Conditions | AvaTrade. AvaTrade. https://www.avatrade.com/trading-info/financial-instruments-index/commodities/cocoa. Published 2020. Accessed October 28, 2020.

Coffee Prices and Coffee Futures Prices – Barchart.com. Barchart.com. https://www.barchart.com/futures/quotes/KCZ20/futures-prices?timeFrame=daily. Published 2020. Accessed October 28, 2020.

Cocoa Prices and Cocoa Futures Prices – Barchart.com. Barchart.com. https://www.barchart.com/futures/quotes/CC*0/futures-prices?timeFrame=daily. Published 2020. Accessed October 28, 2020.

ICCO. COCOA MARKET REVIEW SEPTEMBER 2020. 2020, https://www.icco.org/statistics/monthly-review-of-the-market.html. Accessed 29 Oct 2020.

ICO. Monthly Coffee Market Report – September 2020. London, 2020, http://www.ico.org/documents/cy2019-20/cmr-0920-e.pdf. Accessed 29 Oct 2020.

ICO. Monthly Export Statistics (Members & Non-Members) – August 2020. London, 2020, http://www.ico.org/prices/m1-exports.pdf. Accessed 29 Oct 2020.

ICO. Imports Of Coffee By Selected Importing Countries – June 2020. London, 2020, http://www.ico.org/prices/m4-imports.pdf. Accessed 29 Oct 2020.

ICO. Coffee Production By Exporting Countries. London, 2020, http://www.ico.org/prices/po-production.pdf. Accessed 29 Oct 2020.

ICO. World Coffee Consumption. London, 2020, http://www.ico.org/prices/new-consumption-table.pdf. Accessed 29 Oct 2020.

Ny Cocoa Closes At A 2 Week Lows On Concern Pandemic Lockdowns Will Curb Cocoa Consumption – Barchart.com. Barchart.com. https://www.barchart.com/story/futures/quotes/CC*0/futures-prices/533051/ny-cocoa-closes-at-a-2-week-lows-on-concern-pandemic-lockdowns-will-curb-cocoa-consumption. Published 2020. Accessed October 28, 2020.

Terazono E, Munshi N. Choc waves: how coronavirus shook the cocoa market. Financial Times. https://www.ft.com/content/37aa0ac8-e879-4dc2-b751-3eb862b12276. Published 2020. Accessed October 28, 2020.

USDA. Coffee: World Markets And Trade. Washington, 2020, https://apps.fas.usda.gov/psdonline/circulars/coffee.pdf. Accessed 29 Oct 2020.UBS. Agriculture: Food Price Risks Emerge. Züirch, 2020. Accessed 29 Oct 2020.