World’s corn and wheat production is bigger-than-expected while Australia is drying up!

WHEAT:

Australian Wheat:

Australia will import its first shipment of wheat in 12 years as a drought dramatically decreased the output of the grain world’s fourth largest exporter forcing it to buy cargoes from Canada. Many farmers have been forced to delay planting or to choose to sow into dry soils with a higher risk of crop failure. Australia’s forecasters announced in March that production would rally 40 percent however little rains, private forecasters trimmed their estimates. Australia’s traditional customers such as Indonesia (the world’s second biggest importer of wheat) have turned to Russia and Ukraine to buy record volumes.

World’s Wheat:

The Black Sea region, Europe and North America are expecting an increased production (bigger than expected) for the 2019/20 crop which will be harvest around the middle of this year, likely depressing prices.

Trade war and USDA’s aid to farmers:

The USDA recently paid 8.52 billion dollars to farmers designed to offset losses from trade tariffs by China and as talks fell short last week, the Trump administration is working on a second aid program to support farmers. The commodities that received aid were of course soybeans and, corn, wheat, cotton and sorghum.

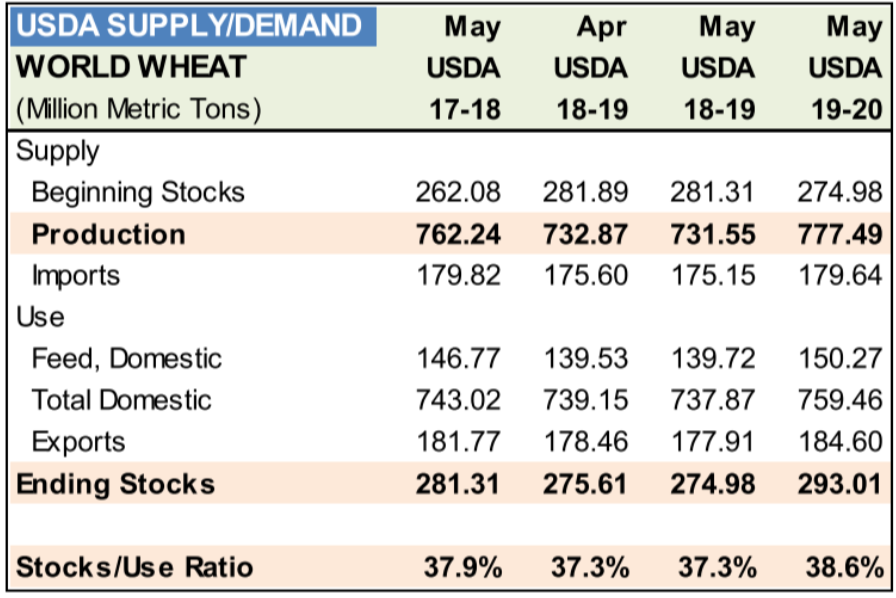

Wheat global production is also high

As shown in the graph, the expected production of wheat for the harvest 19/20 is higher than the 2 past years with 777.49 mio MT for 19/20, 731.55 mio MT for 18/19 and 762.24 for 17/18.

This has result of a current ending stock higher than usual with 293 mio MT.

Many different producing countries are currently having trouble to sell their grains such as the US. Indeed, Dan Roose, president of the US commodities said “We’re swimming in grain.”

US corn grower are currently facing financial difficulties

As previously explained, many farmer in the US are highly impacted by the trade war between China and the US.

Due to this situation, US corn growers are putting pressure on Trump for a better traitement of his USD 15bio China trade aid plan.

To face this issue, M. Trump has previously made a consequent subsidy to his farmer of 8.52 billion of USD. However, the National Corn Growers Association sent out a call to action urging farmers to tell Trump that the 1 cent-per-bushel payment that growers received under the prior market facilitation payments wasn’t enough.

Trump has announced on Friday that he will take in consideration the opinion of the farmers. He has recently asked the Agriculture Secretary Sonny Perdue to work on a plan for solving this issue.

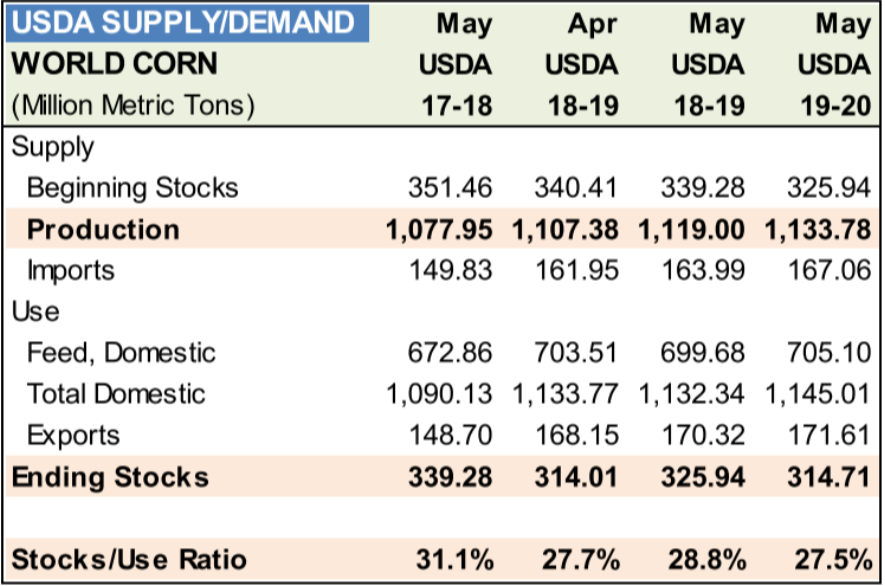

Corn supply remains stronger than previous years even with the US recent flood problems

Even though the recent problem in flood in the US which was supposed to lead to a decrease in the future crops, it seems that the production has slightly risen from 1’119 Mio MT in may 18-19 to 1’133 mio MT in may 19-20 in the world. The US hasn’t been really impacted by the recent floods and has done even better than last year. On a world basis it seems that most countries are doing well with the production of corn except Ukraine which has increased the quantity planted of Wheat and decrease the amount planted of corn.

The Ending stock of corn remains in the average in comparison from last years. It is 2 months before the harvest period of corn which happens from July to september.

Trader point of view

From a trader’s point of view, because there is an increase in production compared to last year, prices for the next harvest have decreased. So, trading companies have interest to sell their stock and are actively concerned by this price change, because they have bought their products more expensive than they are currently worth. And if we compare last year’s prices at the same time, we see that there is a very clear loss. For example, the spot price approximately worth 440 cent per bushel last year compared to 376 at the same time last year for corn.

As you can see above, forwards curves for wheat and corn are quite special as they are always/often in contango.

This fact is due that it has to always cover the cost of carry to give the incentive to the farmer to keep growing this agricultural product. May to July are the only months when the contango becomes less steep for wheat.

This is due to the harvest period and the market is full of new crop. However for the corn, it is from July to September that the supply become huge and takes over the demand.

Finally, when the market become more bullish as the demand is higher, the forward curve becomes in backwardation. This feature is very typical for agricultural goods.

On 14th May 2019, the project of Exxon Mobil to develop business of LNG in Mozambique was approved by the country’s government. Exxon Mobil, the U.S. oil giant, took charge of the East African LNG project’s onshore operations following a $2.8 billion deal with Italy’s Eni in 2017. This project called “The Rovuma LNG project” is expected to produce, liquefy and market natural gas from three reservoirs located in the Area 4 block offshore Mozambique.

Qatargas and its vessel in the Panama Canal

Qatargas, the world’s largest LNG producer, announced on the 13th of May 2019 that Al Safliya, a Q-Flex vessel with a cargo carrying capacity of 210,000 cbm of LNG, completed the 82-kilometer transit on May 12th through the Panama Canal. This is the first Q-Flex type carrier and the largest LNG vessel (315 meter long and 50 meter wide) to transit the Panama Canal. As a reminder, the Panama Canal was expanded in 2016 through the completion of new Neopanamax locks, thereby allowing LNG vessels to pass through the canal.

In April 2018, the Panama Canal Authority announced it would accommodate vessels up to 51.25 meters wide opening the prospect for Qatargas’ Q-Flex vessels to transit. The transit of Al Safliya through the Panama Canal creates future opportunities for the 31 Qatari Q-Flex vessels, allowing them to discharge cargoes in the Pacific Basin and then proceed to the Atlantic basin to load their next cargo.

Chevron and Anadarko Petroleum merger

On the 9th pf May, 2019, Chevron which operates in Australia for LNG, has decided to has decided to back out of the Anadarko Petroleum takeover deal. Chevron will not make a counterproposal concerning the merger agreement with Anadarko and will allow the four-day match period to expire, so Chevron thinks that Anadarko will terminate the merger agreement.

Michael Wirth, Chevron’s chairman and CEO, stated that “Winning in any environment doesn’t mean winning at any cost. Cost and capital discipline always matter, and we will not dilute our returns or erode value for our shareholders for the sake of doing a deal”. If the merger agreement is cancelled, Anadarko will be required to pay Chevron a termination fee of $1 billion.

China raises tariffs on US LNG imports

On Monday this week, China

announced that they will arise tariffs on US LNG imports from 10% to 25%. This

decision will be effective on the first of June.

With this announcement, Big

LNG companies like Cheniere Energy and Tellurian have no significant fear about

this tariffs’ raising, as there will be no major impact on their ability to

sell LNG around the globe outside China. However, this will benefit United

States’ foreign competitors as Russia whose goal is to expand their offer to

Europe and China.

Surely, this 25% tariff means that there will be no longer China consumers for US LNG. The biggest impact would be on projects for which contracts have not been signed yet. Indeed, companies seeking to finance LNG plants have to first obtain long-term commitments from customers. Consequently, it will be more difficult to negotiate long-term contracts.

Underlying the importance of

the LNG market in the United Stated, President Donald Trump visited earlier

this week the newly constructed LNG terminal in Louisiana, named Cameron.

This visit marked the start of the LNG production as an achievement and a great offer for several thousands of employees. Cameron LNG whose mother entity is Sempra Energy, is one of five LNG projects Sempra Energy is developing in North America; In addition, Cameron LNG shareholders are currently discussing a possible extension of the initial project, already authorized by the Federal Energy Regulatory Commission.

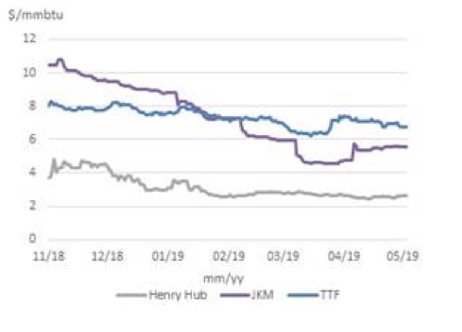

Henry Hub vs TTF vs JKM

Regarding the TTF market prices (the Dutch Title Transfer Facility) :

The Dutch Market has shown higher LNG imports over the last few months essentially from Russia, Norway and other places via liquefied natural gas tankers. Reacting from the decrease of Asian demand, the TTF market has implemented different projects. Moreover, a big majority of new LNG deals within Europeans markets is increasingly referencing to the Dutch market and also used in Asian trades. The weight of this market is getting higher due to the euro prominence gaining in energy trading. Finally, with uncertainties about Brexit the UK activity trading is turning on the Dutch Title Transfer Facility, as the market is surging.

For the Henry Hub American market prices

For the first time, at the same day, the Lower 48 States of USA has received gas deliveries in 6 LNG exports facilities including the 4 new ones in Louisiana named Cameroun and the two others in Georgia (the Kinder Morgan’s Elba) and in Texas Freeport LNG which they are preparing to begin production. The main observable consequence is the oversupply of LNG over the USA territory depending of those facilities. On the other hand, a dozen other second-wave projects that are actively being developed for service in the early- to mid-2020s will raise the supply.

Regarding the JKM Japan Korea Market prices

Asian spot prices for liquefied natural gas (LNG) are following European gas prices up, this week for the first time since last December. Additionally, as the trade war is currently open between China and the USA, tariffs on liquefied natural gas (LNG) imports from the United States would raise.

TTF forward curve

We can see a contango situation in the beginning and followed by a slight backwardation.

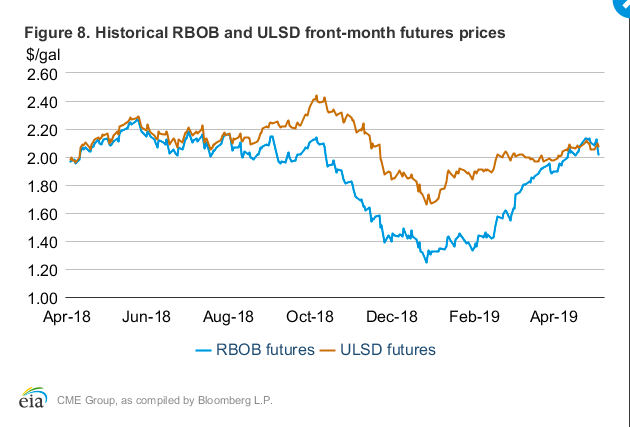

The RBOB futures market is actually in backwardation due to the seasonal pattern of gasoline. The price of gasoline and the demand for gasoline tend to rise during April / May resulting from a different kind of gasoline produced, so the fact that the market is in backwardation makes total sense.

Regarding ULSD futures market, the market is in contengo, the market is well supplied and it is less impacted by the seasonal pattern.

The shutdown of Russia’s Druzhba pipeline

Due to the discovery of the contamination of Russian crude on April 2019, the Russian government has been forced to shut the Druzhba pipeline which pumps 1 million barrels per day of crude, which represents 1% of global supply going to Germany, Poland, the Czech Republic, Slovakia, Hungary, Ukraine and Belarus. Oil from Ust- Luga (a Russian port), has also been contaminated with organic chloride which is a chemical compound used for oil extraction that can damage refining equipment. The Russian supply problems will lead to an increase on oil price and decrease production from the world’s second largest exporter of crude.

Approximately 10 crude tanker with 1 million tonnes of oil, worth more than $500 million still looking for buyers as the oil is contaminated. Vitol, Glencore and Trafigura bought the biggest number of cargoes loaded from the Russian Baltic port of Ust-Luga in late April. According to Reuters, two or three cargoes were also taken by Total and BP trading units. The sellers involved are Rosneft, Russneft, Surgut and Kazakh firms, according to the loading schedules from Ust-Luga port. Buyer such as Eni, Exxon Mobil, Royal Dutch, Shell, PKN and Repsol have refused to take the oil into their refining infrastructure.

The Russian oil supply issue and the unsold cargoes from Ust-Luga could create a supply shortage in Europe and probably increase gasoline and diesel price in the future . The Russian government has promised to fix the quality issue faced by its oil production but nothing has been done since this declaration. The biggest European Terminal in Amsterdam told customers they would not accept any crude coming from russia with organic chloride above 50 ppm.

The acquisition of Anadarko by Chevron or Occidental

On 12th of April 2019, one of the biggest and most productive oil field in the United States called Anadarko has received a merger offer from Chevron. A few weeks later, Occidental, a petroleum company, four times smaller than Chevron has offered a takeover bid superior to Chevron’s offer. Occidental offered to pay $76 per share in cash and stock which represent about 17 percent more than what Chevron agreed to pay to Anadarko ($65 per shares). Occidental’s superior offer has been seen from many wall street analysts as not realistic as Chevon had better revenues. This new offer has raised the stakes in what would be the biggest takeover in the global oil industry in three years.

However, this bidding war has taken another turn when Warren Buffett, an American business magnate considered as one of the most successful investor in the world has announced that he will invest $10 billion to Occidental acquisition of Anadarko. In the deal, Buffet would receive 100’000 shares and 8% annual dividend. On Monday 6 of May 2019, Anadarko Petroleum board said that it intended to reject its first takeover bid, Chevron, as Occidental Petroleum came with a better offer. The combination of Occidental and Anadarko would generate more than 1.4 million barrels of oil per day

U.S. to Clamp Down on Iranian Oil Sales, Risking Rise in Gasoline Prices

Over the last few months, the Trump administration has an aggressive plan to ultimately end the exportation of Iranian oil from other nations, especially China and India. This move is entirely driven by politics since the aim of the Trump administration is to starve the country in order to drastically alter the government and its position in the Middle-East. The core tactics and the american nations was to implement economic sanctions.

While other countries have completely stop their purchases from Iran such Taiwan, Italy and Greece, other countries have long continued their businesses with the country just as usual, such as the aforementioned China and India.

One of the byproduct of this course of action has been the increase in the price of gasoline specifically. When referring to the price of gasoline in America, global head of energy analysis at the Oil Price Information Service, Tom Kloza has stated that “Last summer didn’t go above $3 a gallon as a national average, but this summer, if we don’t have Iranian oil we probably do go over $3”. This clearly displays the high dependance the US has with Iran. The country has planned some sort of counter solution with their own blend of gasoline which is expensive in response to the already expensive regular gasoline already in the market.

Glencore cuts 2019 copper production market as

has been lowered following severe flooding in Australia and also due to security

failure that led to a 7 percent drop in production for the 1st

quarter.

Furthermore, the mining sector has been worried

and under pressure due to his exposure to environmental and political risk. The

presence in countries viewed as high risk like Democratic Republic of Congo,

might damage the company reputation.

Indeed, Glencore’s Katanga Mining unit which

produce copper and cobalt in the Democratic Republic of Congo had to stop is

production after detecting radiation and Glencore had to install a plant in

order to remove the contamination. The Katanga Mining Unit just restarted.

Rio Tinto has discovered a potential mine of

copper-gold-silver in Winu in Australia. This is a potential boost for the

company growth. If it is not a Tier 1 asset, Rio Tinto will move to another

exploration project.

Even though the new projects, Rio Tinto believe

that the cooper market will go into a deficit as electric vehicle boom and

bigger power grids will boost demand while supplies will remain constrained.

However, analysts at CRU (commodity research unit), think that thanks to major mining projects like Anglo’s Quellaveco, Teck’s Quebrada Balance and many others, the copper market will be in a small surplus market and it will go short in 2023.

Trade news:

Despite price drop , copper still created desire. Indeed, the electric car and renewable energies have revived interest in this metal. An electric vehicle contains four times more copper than a conventional vehicle. Wind and solar power generation also requires a lot of copper. Several transactions have been announced in recent weeks by giants in the sector. BHP, the world’s leading mining group has acquired an interest in an exploration company, SolGold which has one of the most promising projects in the sector today. China’s number three copper miner, Zijin Mining, has taken over Serbia’s largest mine. Anglo American had previously chosen to launch a $5 billion mining project in Peru.

Futures Forward Curves

previous

Current

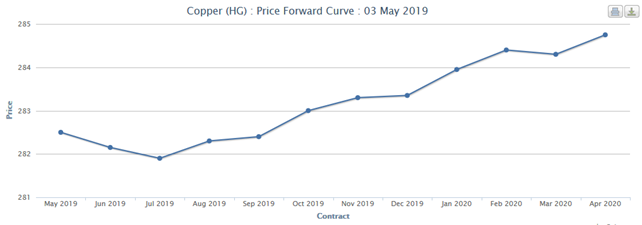

By comparing 2 forward curves above, we can notice some changes in the copper market. In the previous curve, the market was in the contango directly from April, meaning that the there was an oversupply situation. In the current curve, we are in backwardation. The market turns from a bearish to bullish market to an undersupply situation.

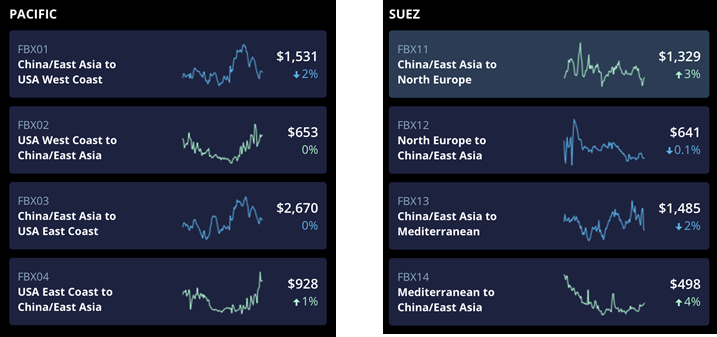

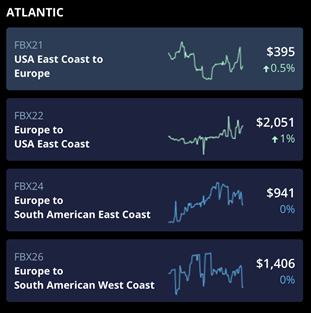

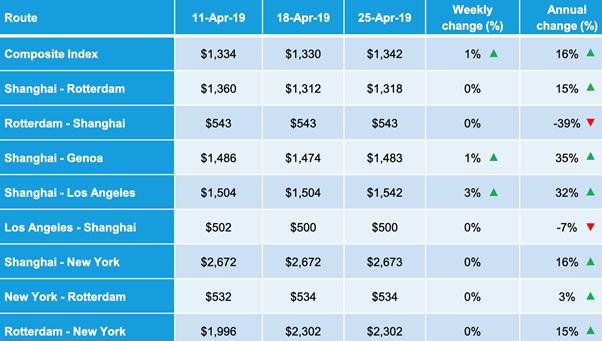

On the 26th of April the freight price is at 1’334 USD, Going up 4.22%, it has stabilized in the region of 1’300 and 1’400 USD since our last bulletin.

As we can see on these graphs, there has been little movement. many routes haven’t changed much. The highest movers has been Mediterranean to China/East Asia which went up 4%, after a sharp decrease lasting a few months.

Looking at the Pacific graph, we can see that going from USA to Asia is becoming more expensive whereas the other way back is declining in price.

As we can see again on this graph, there hasn’t been much change in nearly a month but we can see that most prices have increased when looking at annual changes except Shanghai which has decreases.

Transporting LNG is very

profitable

A global quest for cleaner energy has fired up demand for

liquefied natural gas (LNG). Over a dozen different companies, including energy

majors BP and ExxonMobil, trading house Trafigura and gas utility Centrica are

already looking to charter boats for the winter, according to four shipping

industry sources, months earlier than usual. Energy firms are trying to avoid

getting stuck without ships on charter for the winter, when cold weather

typically drives up trade in LNG and, consequently, transport costs.

The market for LNG freight trade is relatively new and many

companies are reluctant to talk about trading strategies, which are still being

developed. Some specialists see LNG shipping as a commodity of its own, many

companies are starting to trade LNG Freight.

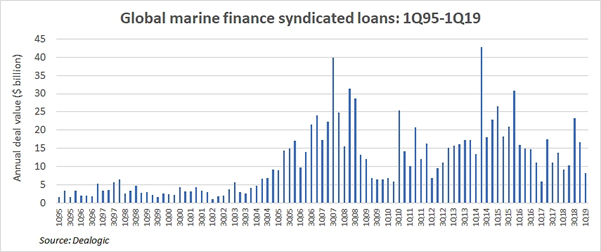

What sinking ship finance means to future ocean freight markets

The securities sales by U.S.-listed ship owners and global marine syndicated loan activity being the two significant indicators of vessel finance, are both currently flashing warning light. This will consequently impact the ocean freight markets both in the short and long-run.

Furthermore, in 2018, U.S.

–listed ship owners made only $650 million from sales of common stocks whereas

it was $4.6 billion in profits generated from common-equity offerings 2014. The

reason of this was that shipping stocks have been traded below the “net asset

value”.

Another reason of sinking ship finance is that shipping bank-debt availability has been squeezed by the implementation of regulations under the Basel III protocol and impending implementation of Basel IV. There are indeed at least three reasons that ship finance is very important to ocean freight markets.

Transparency: the more listed owners there are, the more information is

delivered to the cargo market on dominant rates. Despite, the availability of

various freights rate indices (e.g. Baltic Dry Index), the actual rate obtained

by ship owners are often different from the benchmark rates.

Reliability: in terms of cargo-transport reliability, ship financing is significant e.g. inability of cash increase will lower ship maintenance spending and this will therefore drive to ship breakdowns.

Rates: the major consequence of ship financing availability on

ocean freight pricing is the more access of vessel finance, the newer vessels

will be built, the more available ships on the market (more capacity), and this

will therefore lower future rates for cargo shippers. The effect on freight

rates is mainly seen in the wet and dry bulk markets unlike container shipping

as the latter large number of orders is “government-sponsored”.

Finally, when the capital become more expensive and difficult to find, the returns indeed have to cover expenses. As the capital costs are rising in the shipping market, the capacity would ultimately have to decline in relation to cargo demand, and freight rates would have to increase accordingly.

New shipping rules leave oil traders strangely paralyzed

IMO 2020 regulations promoting Low-Sulphur fuels throw up plenty of unknowns Regarding the effect of IMO 2020 on fuel price –

On one side, there are analysts and traders who believe the

regulation will lead to a spike in diesel prices that potentially feeds through

to crude oil markets, making energy prices higher across the board. Some even

forecasting a recession as a result.

On the other hand, others think these fears are exaggerated

because they assume that refineries have been aware of the coming shift for

years and the best run groups will have put plans in place to increase output

of diesel-style fuels (which will prevent a short in supply therefore a lower

increase in price than expected in case of undersupply).

In addition to that, there is also the explanation about the

number of ships that may fit Sulphur-removing scrubbers to their engines as a

solution, allowing them to keep using cheaper, dirtier fuels without flouting

the rules. However, this is expected to be only around 4 percent of the global

shipping fleet.

The International Energy Agency forecast earlier this month that

demand for High-Sulphur fuel oil, commonly used in shipping, could fall 60 per

cent in one year, while demand for very low Sulphur shipping fuel — a

diesel-like product — could double to 2m b/d. But nine months out from crunch

time, despite the debate, the oil market still feels strangely paralyzed by

indecision.

This uncertainty could potentially explain the stabilization of price of freight that we mention in this bulletin, as traders are more hesitant to enter new deals. Deals may be made on a smaller scale as an attempt to reduce risk, which makes less of an impact and leave the price to stabilize.

According to an article from Reuters, a coffee centre near Dubai’s Jebel Ali port has been opened which offers the opportunity to store and to process coffee beans in the Middle East.

Being modern and able to handle up 20’000 tonnes of coffee beans annually in bulk or in speciality (equivalent to $100 million according to Sanjeev Dutta, executive director for commodities at DMCC), this coffee centre is equipped of temperature-controlled facility for coffee beans, and offers infrastructure and services for the processing and the delivery.

The advantage of this coffee centre is that it is the only one located in the Middle East. Thanks to this advantage, coffee traders could use this centre as a distribution hub for the region and get a bigger margin in the redistribution of their coffee beans.

The purpose of The Dubai Multi Commodities Centre (DMCC) is to attract major coffee trading house, as well as small and medium players in the coffee market, to bring and deal their business in this new coffee centre.

Indeed, in our opinion, this would increase the revenue of the center by receiving the payment of the storage costs paid by traders. Moreover, the concerned port in Dubai will have a competitive advantage compared to the other ports of the region because, traders could use this new center as a storage point and could distribute easily coffee beans in different volumes in the region.

Until now, the coffee beans in bulk that have already gone through this coffee centre were from South America and East Africa. However, the location of this centre is interesting and well-positioned for coffee traders who deal with Asian producers such as coffee producers from India or Indonesia.

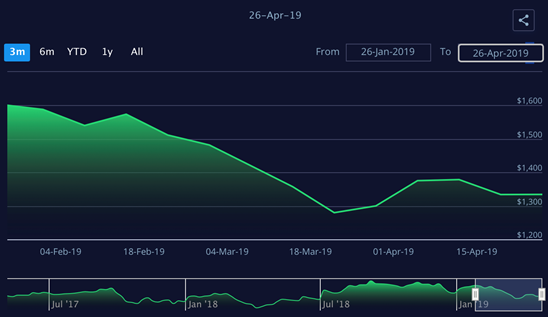

Coffee at all time low in 13 years

The coffee is traded at an all-time low of 93 cents a pound for the Arabica (spot prices US April 2019). The cost of production should be around $1,20 to $1,50 per pound for the many small producers to breakeven. In Guatemala, farmers are abandoning the farms while Colombians are turning into Cocoa production. The problem is that the market is largely driven by the Brazilian coffee (about ¼ of the world’s coffee trade). The oversupply from the country (62m in 2018) made the price drop low. Moreover, the Brazilian Real has depreciated, pushing them to export even more: the coffee is traded in dollars, which gives the incentives to Brazilian farmers to export and get more money from it.

What would be a coffee trader’s position right now while the price of coffee is historically falling? As we know, traders are hedging their physicals with futures. As we know too, traders are long physical and short futures. Let us remember that traders are not trying to get money from the futures, but trying cancel out the risk.

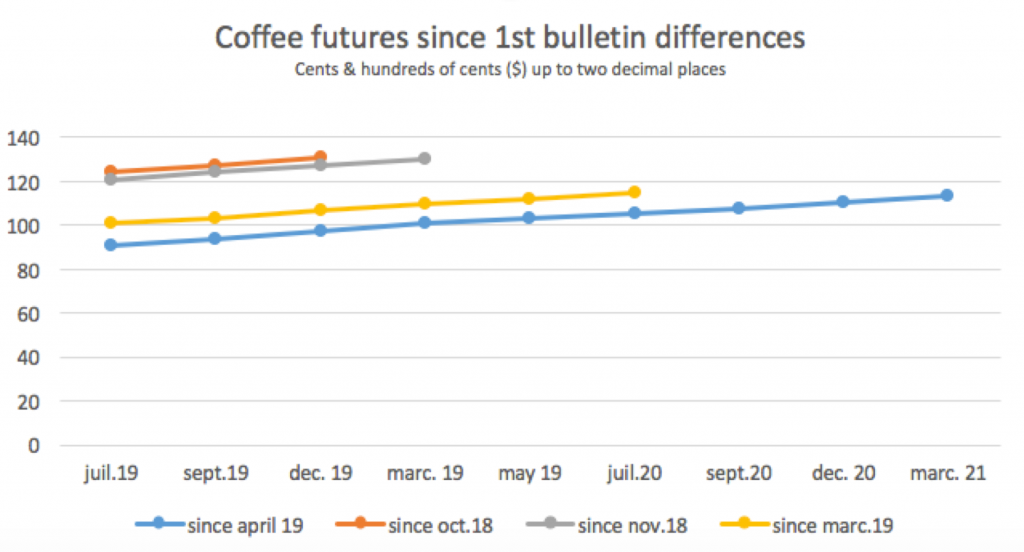

Futures comparison since beginning of the semester:

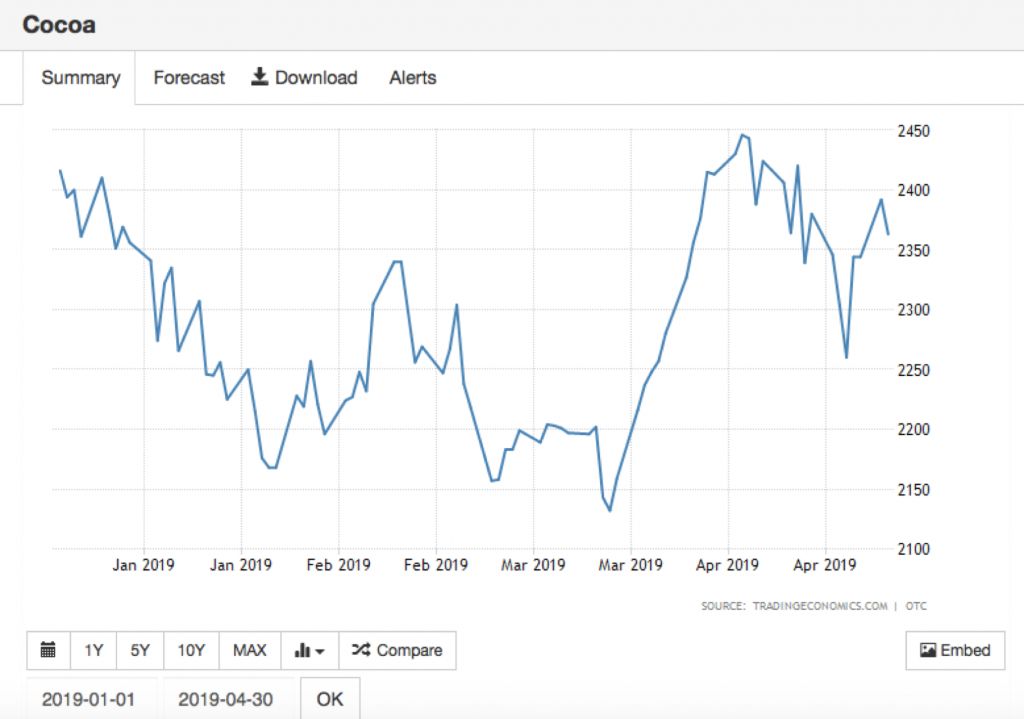

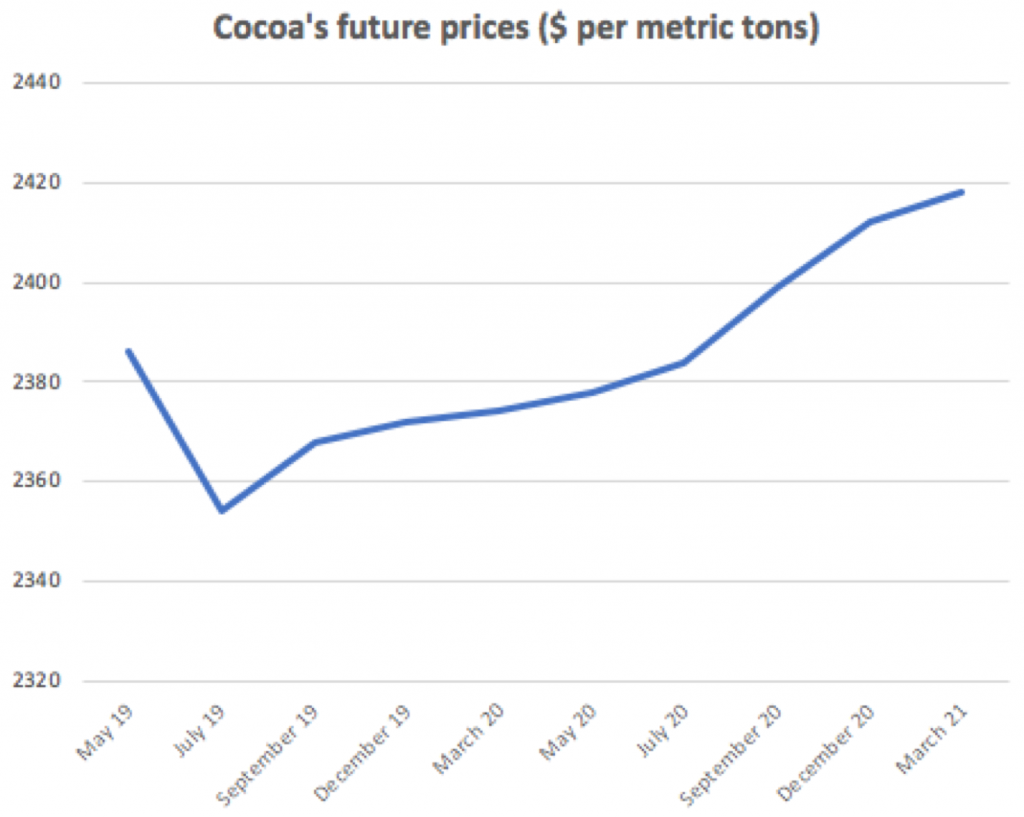

Cocoa’s spot and future price

Cocoa’s spot price / price in $ per MT

Cocoa’s future price

For the month of April 2019, the spot price of cocoa was equal to USD 2’368per MT, and is higher than the future price which is equal to USD 2’354per MT.

By referring to the cocoa’s future curve which shows the 10 metric tons’ future contract, the current cocoa market is in backwardation since the future curve is downward. Having the cocoa’s future price lower than the spot price, it means that currently the worldwide demand for cocoa is high, and the cocoa market is a bullish market. The reason of this high demand might be the end of the crop’s season of cocoa.

Small case study

First, we are a small company trading cocoa. Our aim is to develop the chocolate business in Asia, mainly in China. We are seeking either to buy or to grow more cocoa plantation and we are searching which country would be the best for us to buy or invest.

Actual China importation

At the beginning, we analysed the actual importation of cocoa from China in 2018, in order to understand what is the actual demand.

We saw the total import in 2018 equal to 4’125 thousand tons. Therefore, the China importation represents 0.8 percent, not even 1 percent of the total importation of cocoa. This data confirms us that there is a market to develop in this region.

From where to import?

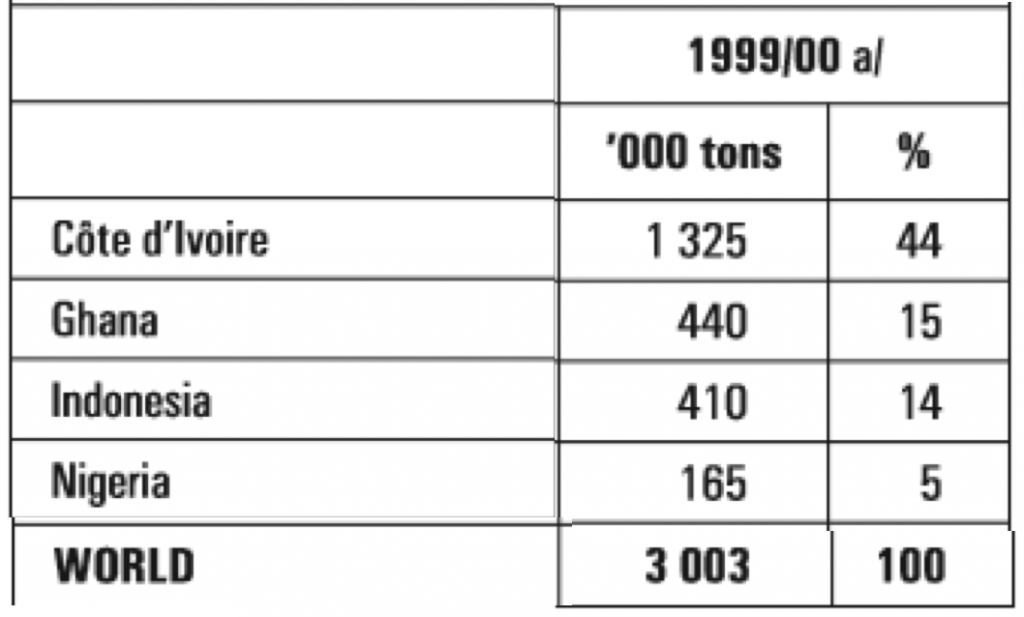

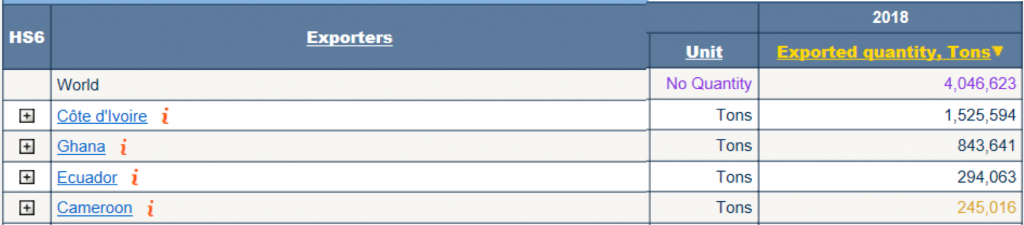

In order to get a better understanding of the exporting countries and the actual trends, we did an analysis of the 4 biggest exporting countries comparing their productions between 2000 and 2018.

In 1999/2000

In 2018

What appeared at the first glance is the global production which increased from 2000 to 2018 from 3’003 thousand tons to 4’046 thousand tons.

We are facing an increase of more than 25 percent in 18 years. We can see that Côte d’Ivoire kept the first place and even increased its production.

Ghana doubled its production which show that they heavily invested in cocoa production and also that is a profitable business.

In contrary, Indonesia which is the closest country between the one above to China decrease from 410 thousand tons in 2000 to only 27 thousand tons in 2018. It appears that around 2012, following bad crops with small beans and many dead trees, Indonesia stopped their cocoa production for palm oil which request much less work as stated in the article from Reuters in 2012 “Indonesia’s “Frankentrees” turn cocoa dream into nightmare”.

Then by looking at the 10 biggest exporters in 2018, all of them are either from east Africa or Latin America except Malaysia which is the closest country from China with a constant increase in production since is 2014 reaching in 2018 a total of 155 thousand tons representing a little bit less than 4 percent of the global production.

Cocoa production in Malaysia

Malaysia seems not new in this business and had 9% market share in 1990 but surprisingly like Indonesia in 2012, their production crashed in less than 3 years as shown below.

The global exports of cocoa beans decreased from 9% in 1990 to 2% in 2000 This crash in production for 2 main raisons. The first one isby loss of production due to pests and diseases, and the second one was to benefit from the value added resulting from manufacturing its downstream products

Why there is a new growing trend in cocoa production?

Malaysia doesn’t only benefit from low production cost but also from a structure to process the beans. Indeed, based in the Peninsula can be found grindings and manufacturing plant for cocoa.

There is also another attributable of Malaysian cocoa which is the special characteristic of the high melting point of the Malaysian cocoa butter. This is advantageous for chocolate products in warm countries.

In conclusion, due to the following attributes stated above and to the proximity of Malaysia to China, I would definitely advice to invest in their cocoa plantation to supply the future demand from China.

Sources

REUTERS, 2019. “Dubai’s DMCC in talks with major coffee traders for new coffee centre”. Reuters(online) February 18th, 2019. Consulted on April 30th, 2019. Available at:

THE ICE, 2019. “Cocoa’s future price”. Future contract July 2019. April 30th, 2019 Available at: https://www.theice.com/products/7/Cocoa-Futures/data?marketId=5546320

Cocoa, a guide to trade practices (developed partly by the WTO)Consulted on April 30th, 2019. Available at: http://www.intracen.org/uploadedFiles/intracenorg/Content/Publications/Cocoa%20-%20A%20Guide%20to%20Trade%20Practices%20English.pdf

ITC – International Trade Center. Consulted on April 30th, 2019. Available at: https://www.trademap.org/(S(n0bt52420brwnhk2djmqtk01))/Country_SelProductCountry_TS.aspx?nvpm=1%7c458%7c%7c%7c%7c1801%7c%7c%7c4%7c1%7c1%7c2%7c2%7c1%7c2%7c2%7c1

Reuters, Indonesia’s “Frankentrees” turn cocoa dream into nightmare https://www.reuters.com/article/us-cocoa-indonesia/indonesias-frankentrees-turn-cocoa-dream-into-nightmare-idUSBRE89E1DA20121015

Supply and Demand Model for the Malaysian Cocoa Market Consulted on April 30th, 2019. Available at: https://mpra.ub.uni-muenchen.de/…/11.Supply_and_Demand_Mo…

Traders wake up to cost of coffee crisis, Financial times, consulted on April 2019, available at: https://www.ft.com/content/21907ea6-5f98-11e9-a27a-fdd51850994c

{kind=link}