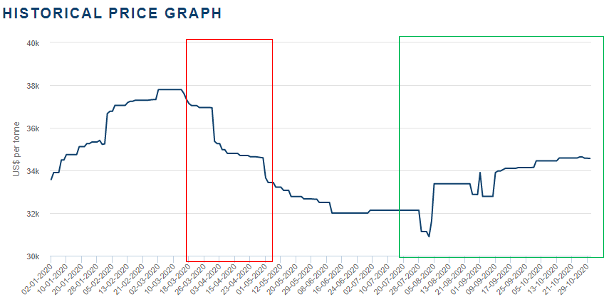

Price fluctuation

A decrease in oil price could result in an opportunity to produce more cotton at a lower price as the shipping and harvesting parts are high oil consumers. We can clearly see how the worldwide lockdown in March has lead to a huge drop in cotton’s prices.This crash is explained by the economy worsening off, and customers are less likely to buy cotton-based items. Furthermore, countries may have stopped stockpiling which could have led to artificially inflated prices that we had during the earliest month of 2020. Government policies and sustainable programs trying to shield the farmers and textile industries could have a big impact on production costs and may cause this uncertainty. Bad weather in some regions also influenced cotton prices, especially when there are drought periods as this year, which produce an automatic decrease in the price because of production issues.

After this crash, we can see that the price of cotton slowly recovered to the same level than before the pandemic, this may be explained by the countries trying to relaunch their economy by easing their restrictions on population. However, we can see that the price dropped again in October-November which could be linked to the current situation where many European countries re-entered in a lockdown.

Supply and demand dynamic of the commodity:

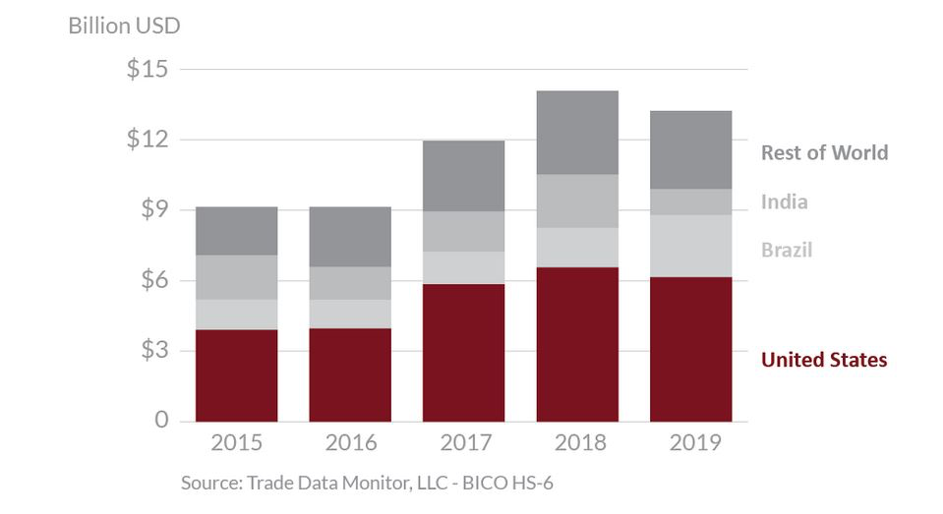

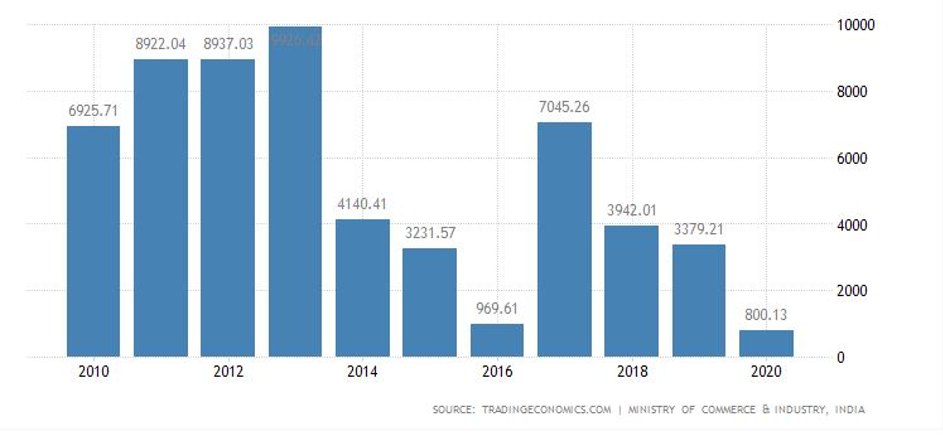

On a global scale until the end of 2019 the exports of cotton were stable. But in 2020 the cotton industry has been hit hard by the Covid-19 pandemic, large cotton producer such as India has seen its exports decreased to 800.13 USD Million in 2020 against 3379.21 USD Million in 2019.

According to the World Trade Organization, the World (based on available data for countries and represents 90% of world trade) cotton exports in March 2020 decreased by 12.5% while it decreased by 34.6% in April 2020 compared to the same months in 2019.

Global Cotton Export

India’s cotton Export (in tonnes)

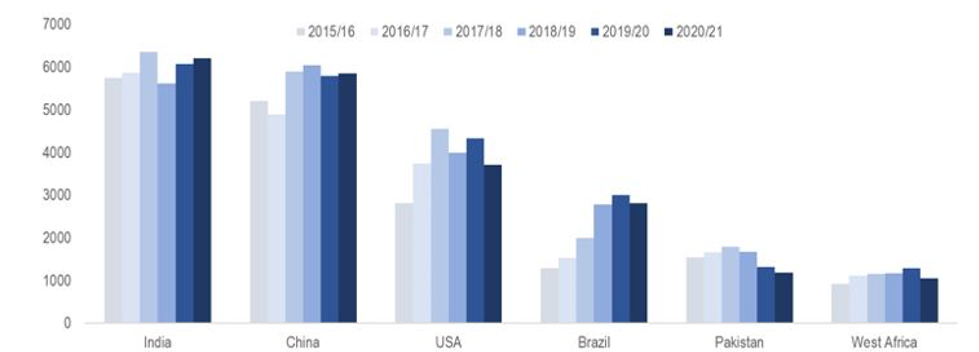

In contrast we can see that the cotton production has been more or less steady in India, China and USA but Brazil has seen a growth in its production since 2017 because the state of Mato Grosso has started to heavily grow cotton. It went from approximately 2000 tons to 3000 tons in a year. The cotton supply chain suffers from Covid, trade tensions and weak global economy and this is why most of the producing countries will see their production decrease for the 2020/21 projection.

Production Changes in Major Regions from 2015/16 to 2020/21 (tonnes per country)

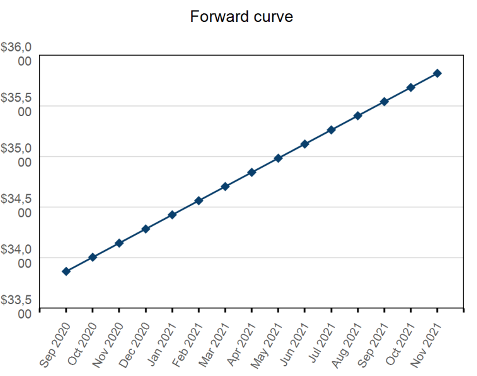

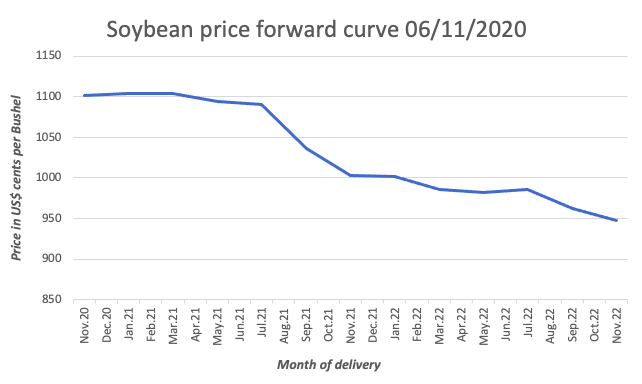

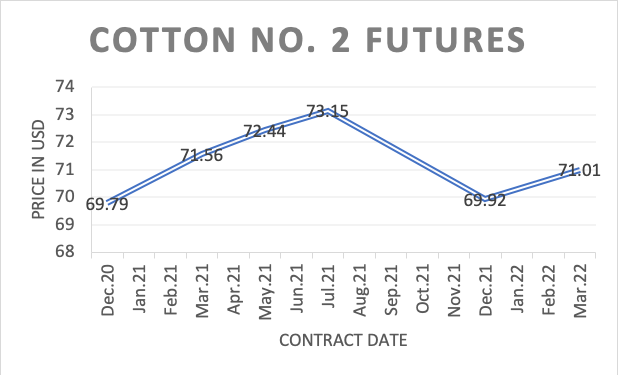

Forward Curve

The cotton futures prices are going to be on the rise until July 2021 (73.310). Right now we are in a contango situation (Price on the 9th of Novembre 2020 : 69.0) and it may go further up with the lesser uncertainty surrounding the COVID-19 pandemic but we can also see a trend from December to July the price is on the up it’s in correlation of the harvesting periods of the different producers.

Recommendations:

As long as the Coronavirus will remain active across the world, the demand should stay week. Indeed, due to this current situation, it becomes hard to shop due to the active lockdowns in several countries and a lot of people became unemployed. Therefore, the demand for cotton should remain week in the next few months while the supply is projected to outpace demand by 500’000 tonnes. Our recommendation for the next months will be to buy in order to make a profit by selling three months later.

Sequeira Reny, Tiago Marques & Nicole Peytregnet

BIBLIOGRAPHY

5 factors affecting cotton prices – Materials Risk, [no date]. [online]. [Viewed 7 November 2020]. Available from: https://materials-risk.com/5-factors-affecting-cotton-prices/

agric_report_e.pdf, [no date]. [online]. [Viewed 7 November 2020]. Available from: https://www.wto.org/english/tratop_e/covid19_e/agric_report_e.pdf

CERTI-PIK, U. S. A., [no date]. Understanding the Factors That Determine Cotton Prices. [online]. [Viewed 7 November 2020]. Available from: https://certipik.com/2018/07/understanding-the-factors-that-determine-cotton-prices/

Cotton | 1913-2020 Data | 2021-2022 Forecast | Price | Quote | Chart | Historical, [no date]. [online]. [Viewed 7 November 2020]. Available from: https://tradingeconomics.com/commodity/cotton

Cotton 2019 Export Highlights | USDA Foreign Agricultural Service, [no date]. [online]. [Viewed 8 November 2020]. Available from: https://www.fas.usda.gov/cotton-2019-export-highlights

Cotton No. 2 Futures | ICE, [no date]. [online]. [Viewed 12 November 2020]. Available from: https://www.theice.com/products/254/Cotton-No-2-Futures/data?marketId=5673519

Cotton, [no date]. European Commission – European Commission [online]. [Viewed 8 November 2020]. Available from: https://ec.europa.eu/info/food-farming-fisheries/plants-and-plant-products/plant-products/cotton_en

Covid-19 and the Cotton Sector: Adapting and Innovating at Farm Level, [no date]. Better Cotton Initiative [online]. [Viewed 8 November 2020]. Available from: https://bettercotton.org/blog/covid-19-and-the-cotton-sector-adapting-and-innovating-at-farm-level/

CT1 Commodity Quote – Generic 1st “CT” Future, [no date]. Bloomberg.com [online]. [Viewed 7 November 2020]. Available from: https://www.bloomberg.com/quote/CT1:COM

India Exports of Cotton | 1996-2020 Data | 2021-2022 Forecast | Historical | Chart, [no date]. [online]. [Viewed 7 November 2020]. Available from: https://tradingeconomics.com/india/exports-of-cotton

Pakistan Steps Up Imports of Farm Goods to Curb Soaring Prices, 2020a. Bloomberg.com [online]. [Viewed 7 November 2020]. Available from: https://www.bloomberg.com/news/articles/2020-10-01/pakistan-on-shopping-spree-for-farm-goods-in-pricey-world-market

Pakistan Steps Up Imports of Farm Goods to Curb Soaring Prices, 2020b. Bloomberg.com [online]. [Viewed 8 November 2020]. Available from: https://www.bloomberg.com/news/articles/2020-10-01/pakistan-on-shopping-spree-for-farm-goods-in-pricey-world-market

Sécheresse, [no date]. Le climat aujourd’hui et demain [online]. [Viewed 8 November 2020]. Available from: https://blogs.letemps.ch/dorota-retelska/category/secheresse/

What Determines the Price of Cotton?, 2018. Barnhardt Purified Cotton [online]. [Viewed 8 November 2020]. Available from: https://barnhardtcotton.net/blog/what-determines-the-price-of-cotton/