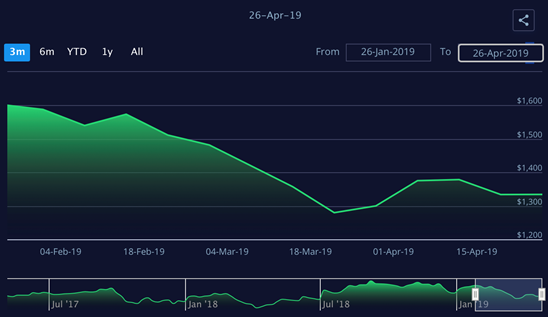

On the 26th of April the freight price is at 1’334 USD, Going up 4.22%, it has stabilized in the region of 1’300 and 1’400 USD since our last bulletin.

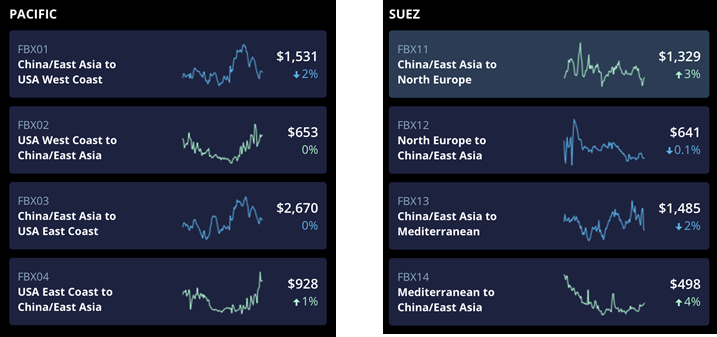

As we can see on these graphs, there has been little movement. many routes haven’t changed much. The highest movers has been Mediterranean to China/East Asia which went up 4%, after a sharp decrease lasting a few months.

Looking at the Pacific graph, we can see that going from USA to Asia is becoming more expensive whereas the other way back is declining in price.

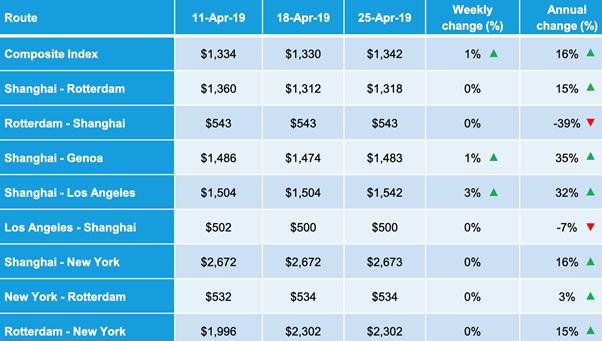

As we can see again on this graph, there hasn’t been much change in nearly a month but we can see that most prices have increased when looking at annual changes except Shanghai which has decreases.

Transporting LNG is very profitable

A global quest for cleaner energy has fired up demand for liquefied natural gas (LNG). Over a dozen different companies, including energy majors BP and ExxonMobil, trading house Trafigura and gas utility Centrica are already looking to charter boats for the winter, according to four shipping industry sources, months earlier than usual. Energy firms are trying to avoid getting stuck without ships on charter for the winter, when cold weather typically drives up trade in LNG and, consequently, transport costs.

The market for LNG freight trade is relatively new and many companies are reluctant to talk about trading strategies, which are still being developed. Some specialists see LNG shipping as a commodity of its own, many companies are starting to trade LNG Freight.

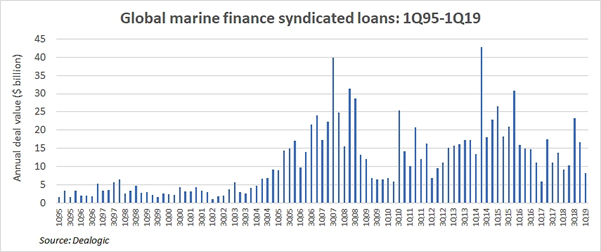

What sinking ship finance means to future ocean freight markets

The securities sales by U.S.-listed ship owners and global marine syndicated loan activity being the two significant indicators of vessel finance, are both currently flashing warning light. This will consequently impact the ocean freight markets both in the short and long-run.

Furthermore, in 2018, U.S. –listed ship owners made only $650 million from sales of common stocks whereas it was $4.6 billion in profits generated from common-equity offerings 2014. The reason of this was that shipping stocks have been traded below the “net asset value”.

Another reason of sinking ship finance is that shipping bank-debt availability has been squeezed by the implementation of regulations under the Basel III protocol and impending implementation of Basel IV. There are indeed at least three reasons that ship finance is very important to ocean freight markets.

- Transparency: the more listed owners there are, the more information is delivered to the cargo market on dominant rates. Despite, the availability of various freights rate indices (e.g. Baltic Dry Index), the actual rate obtained by ship owners are often different from the benchmark rates.

Reliability: in terms of cargo-transport reliability, ship financing is significant e.g. inability of cash increase will lower ship maintenance spending and this will therefore drive to ship breakdowns.

- Rates: the major consequence of ship financing availability on ocean freight pricing is the more access of vessel finance, the newer vessels will be built, the more available ships on the market (more capacity), and this will therefore lower future rates for cargo shippers. The effect on freight rates is mainly seen in the wet and dry bulk markets unlike container shipping as the latter large number of orders is “government-sponsored”.

Finally, when the capital become more expensive and difficult to find, the returns indeed have to cover expenses. As the capital costs are rising in the shipping market, the capacity would ultimately have to decline in relation to cargo demand, and freight rates would have to increase accordingly.

New shipping rules leave oil traders strangely paralyzed

IMO 2020 regulations promoting Low-Sulphur fuels throw up plenty of unknowns Regarding the effect of IMO 2020 on fuel price –

On one side, there are analysts and traders who believe the regulation will lead to a spike in diesel prices that potentially feeds through to crude oil markets, making energy prices higher across the board. Some even forecasting a recession as a result.

On the other hand, others think these fears are exaggerated because they assume that refineries have been aware of the coming shift for years and the best run groups will have put plans in place to increase output of diesel-style fuels (which will prevent a short in supply therefore a lower increase in price than expected in case of undersupply).

In addition to that, there is also the explanation about the number of ships that may fit Sulphur-removing scrubbers to their engines as a solution, allowing them to keep using cheaper, dirtier fuels without flouting the rules. However, this is expected to be only around 4 percent of the global shipping fleet.

The International Energy Agency forecast earlier this month that demand for High-Sulphur fuel oil, commonly used in shipping, could fall 60 per cent in one year, while demand for very low Sulphur shipping fuel — a diesel-like product — could double to 2m b/d. But nine months out from crunch time, despite the debate, the oil market still feels strangely paralyzed by indecision.

This uncertainty could potentially explain the stabilization of price of freight that we mention in this bulletin, as traders are more hesitant to enter new deals. Deals may be made on a smaller scale as an attempt to reduce risk, which makes less of an impact and leave the price to stabilize.

Sources:

https://www.ft.com/content/c486bfe6-4b05-11e9-bbc9-6917dce3dc62