Alexandra

LNG – Bulletin 3 – January 2021

Price movement, demand & supply analysis

We can see on the graph above that the price of Natural traded on the Henry hub benchmark was traded at 2.77 $ per Million BTu on the 5th of January 2021. As expected due to the high seasonality of this commodity, the price is increasing during the winter period where the household consumption is at its highest. Moreover, the worldwide demand for LNG on the Asian market is skyrocketing this year due to an intense cold-weather. However, even if the prices are increasing over the winter period due to an increase of the worldwide demand, the prices tend to converge and decrease within this global market because technological improvement (fracking) have attracted more and more players thus decreasing the production cost of this commodity.

Futures:

The coupled cost decline and regional shifts in demand and supply regarding LNG is the main driver for a strong forecast growth in this market. Liquefaction of natural gas has been around for over a hundred years but technological improvements and new energy consumption trends have transformed the market. China and Europe will continue to experience increasing deficits in their natural gas production whereas North America will show a strong gas surplus resulting in growing LNG exports around the world. Another aspect of LNG is that global liquefaction and regasification capacity will improve and grow together more than the double of today’s levels. Furthermore, due to increasing average shipping distance, tankers transporting LNG will increase their gas transport market share and tonne-miles shipping is expected to quadruple.

A therm (thm) equals 100’000 British thermal units (Btu).

Here the main change and point of observation is the increase in prices for future deliveries between February 2021 and February 2022. Indeed, recent important increases in demand due to cold snap, especially in Asia where we find the three biggest liquefied natural gas world importers, have led to a significant appreciation of short-mid term LNG prices traded as of 6th January 2021. But on a longer term, prices converge again on a lower basis.

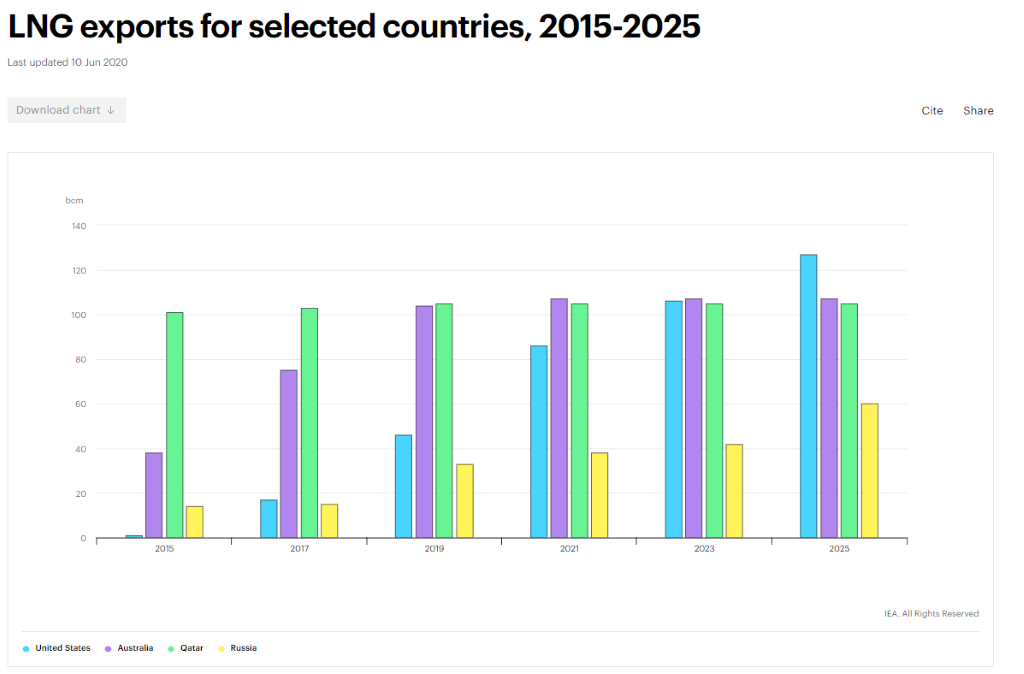

On the previous graph, we can observe the evolution of gas exports by destination from Australia. The main part of the Australia LNG is exported to those following three countries: China, Japan and South Korea. According to the other graph we can see that Australia is going to surpass Qatar as the world’s largest liquefied natural gas exporter. This is mainly due to the fact that Australia’s newly commissioned projects ramp up and operate at full capacity (Wheatstone, Ichthys and Prelude floating LNG projects). Another interesting aspect is concerning the increase of export from the U.S which is expecting to be the country leader by 2025. Five projects are under construction totaling 47.8 MMtpa of liquefaction capacity. More than 30 additional LNG export projects have been proposed for the development of LNG export.

Recommendation:

Since for this coming winter market is expected to go in backwardation for the coming months with the analysis made by NGSA, we recommend selling now and do not store the commodity. In addition, as we are in the second wave of the COVID-19 LNG market is becoming uncertain as every commodity we can only plan for the coming month.

Bibliography

Henry Hub Natural Gas Spot Price, [no date]. [online]. [Viewed 7 January 2021]. Available from: https://ycharts.com/indicators/henry_hub_natural_gas_spot_price

Asia LNG Prices Skyrocket as Buyers Scramble for Supplies Amid Cold Snap, Power Shortages, 2021. Natural Gas Intelligence [online]. [Viewed 7 January 2021]. Available from: https://www.naturalgasintel.com/asia-lng-prices-skyrocket-as-buyers-scramble-for-supplies-amid-cold-snap-power-shortages/

U.S. Energy Information Administration (EIA), [no date]. [online]. [Viewed 7 January 2021]. Available from: https://www.eia.gov/naturalgas/weekly/#tabs-supply-3

LNG supply and demand, [no date]. [online]. [Viewed 7 January 2021]. Available from: https://eto.dnvgl.com/2019/lng-supply-and-demand

UK Natural Gas Futures Curve, [no date]. ERCE [online]. [Viewed 7 January 2021]. Available from: https://www.erce.energy/graph/uk-natural-gas-futures-curve/

LNG exports for selected countries, 2015-2025 – Charts – Data & Statistics, [Viewed 7 January 2021]. IEA [online]. [Viewed 7 January 2021]. Available from: https://www.iea.org/data-and-statistics/charts/lng-exports-for-selected-countries-2015-2025

Australia Exports By Country, . [online]. [Viewed 7 January 2021]. Available from: https://tradingeconomics.com/australia/exports-by-country

3rd Bulletin : North American Oil

Price movement recap

Oil prices have surprisingly increased in the first week of January. It happened after Saudi Arabia said its oil production will be cut by 1 millions barrels per day in addition to OPEC+’s reduction. Crude oil prices are influenced by Energy Information Administration’s (EIA) and the American Petroleum Institute’s (API) reports.

https://www.eia.gov/dnav/pet/PET_PRI_SPT_S1_W.htm

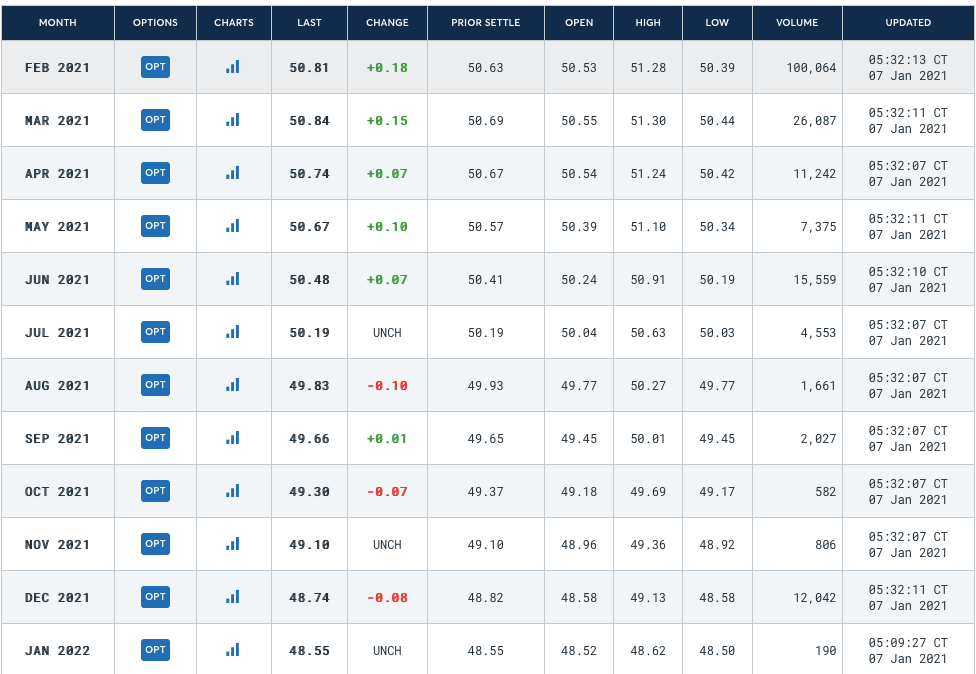

Forward curve 07.01.21

Currently the future market for WTI is quite flat but with a small trend of Backwardation: opposite of contango. The spot price for delivery now is higher than today’s price for delivery in the future. Demand is greater than supply now. So, people are ready to pay a premium for delivery today. It sends a message to suppliers: supply me! don’t store! Don’t store!!

This may be due to the uncertainty about the current global economic condition and the fact that COVID cases have risen during the Christmas holiday. But at the same time, recent vaccines are starting to bring some hope about the market.

Therefore it explains the current feeling of uncertainty about the market.

https://www.cmegroup.com/trading/energy/crude-oil/light-sweet-crude_quotes_globex.htm

Inventory levels

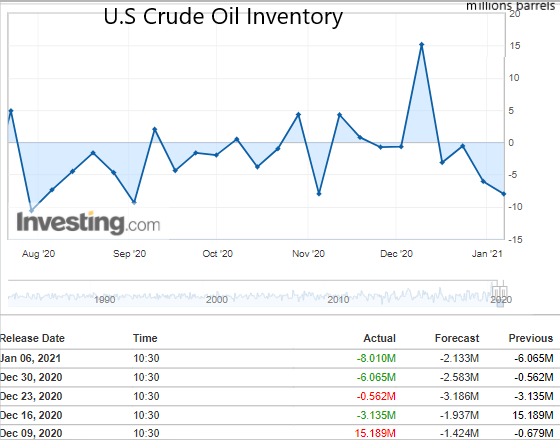

According to the Energy Information Administration, there was a draw of 8 million barrels in 2020’s last week. This news made oil prices rise. This report was done the day after the American Petroleum Institute’s approximation was a draw of 1.66 million barrels, but accompanied by a significant gasoline inventory build and middle distillates of respectively 5.47 and 7.14 million barrels.

United States Crude Oil Inventories (investing.com)

Recommendation

Due to the encouraging news about vaccines the market seems to have seen the worst. Different pictures are present in the main shale oil industry. As most producers do not break even at current rates, some are pessimistic about their future. Others are positive, and among analysts there is also a possibility that the EIA and the industry itself are purposely gloomier than they need to be in order to get OPEC+ to continue its production cuts in order to keep prices higher.

Although prices have been helped by these cuts, volatility exists because not only supply decides where the industry goes, but also demand, which is arguably a far more significant factor right now. And the future remains highly unpredictable when it comes to demand, as Forbes’ David Blackmon noted in a recent post.

In the United States, the pandemic is still raging, vaccines are provided much slower than expected, and this means that the long anticipated return to normal will come longer than many hoped, even in the oil and gas sector, if it ever does. It will inevitably be all about cost and competition again, just as it was during the last crisis in the oil industry. Last time, with substantial support from oilfield service providers, U.S. shale pulled it off, and it ended up leading the boom in U.S. oil production that turned the nation into the biggest producer in the world. The first signs of what is to come later this year will be presented and whether the industry will be able to rebound as strongly from this crisis.

https://oilprice.com/oil-price-charts/45

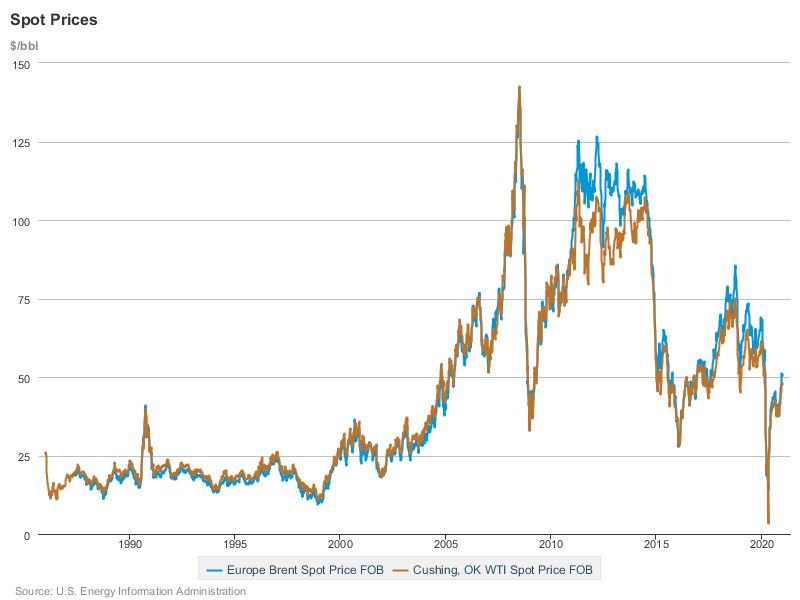

Compared to our last bulletin where the price was at $44.70 and now raising to $50.72 per barrel (price today for delivery in early January) the recommendation was to be long (buy) for the next 3-6 months and still the same as of today. The future consumption of oil is expected to rise continuously throughout the year, since the arrival of the pandemic’s protection and the limitation of production. The market being well supplied will be contango. Prices are going up month after month. Therefore it will be interesting to buy and sell in future contracts with the higher price from the market to cover also the storage costs.

Bibliography

SLAV Irina, 2021 Oil Jumps On Major Crude Inventory Draw [online] [Viwewd 6 January 2021] Available from: https://oilprice.com/Energy/Energy-General/Oil-Jumps-On-Major-Crude-Inventory-Draw.html

SLAV Irina, 2021, U.S. Oil Executives Cautiously Optimistic About 2021 [online] [viewed 7 January 2021] Available from https://oilprice.com/Energy/Energy-General/US-Oil-Executives-Cautiously-Optimistic-About-2021.html

PETROLEUM & OTHER LIQUIDS [online] [viewed 6 January 2021] Available from https://www.eia.gov/dnav/pet/PET_PRI_SPT_S1_W.htm

CRUDE OIL – OVERVIEW [online] [viewd 6 January 2021] Available from https://www.cmegroup.com/trading/energy/crude-oil/light-sweet-crude_quotes_globex.htm

SLAV Irina, 2021, Oil Jumps On Major Crude Inventory Draw[online] [viewed 7 January 2021] Available from https://oilprice.com/Energy/Energy-General/Oil-Jumps-On-Major-Crude-Inventory-Draw.html

Cotton – Bulletin N° 3

News & Price fluctuations

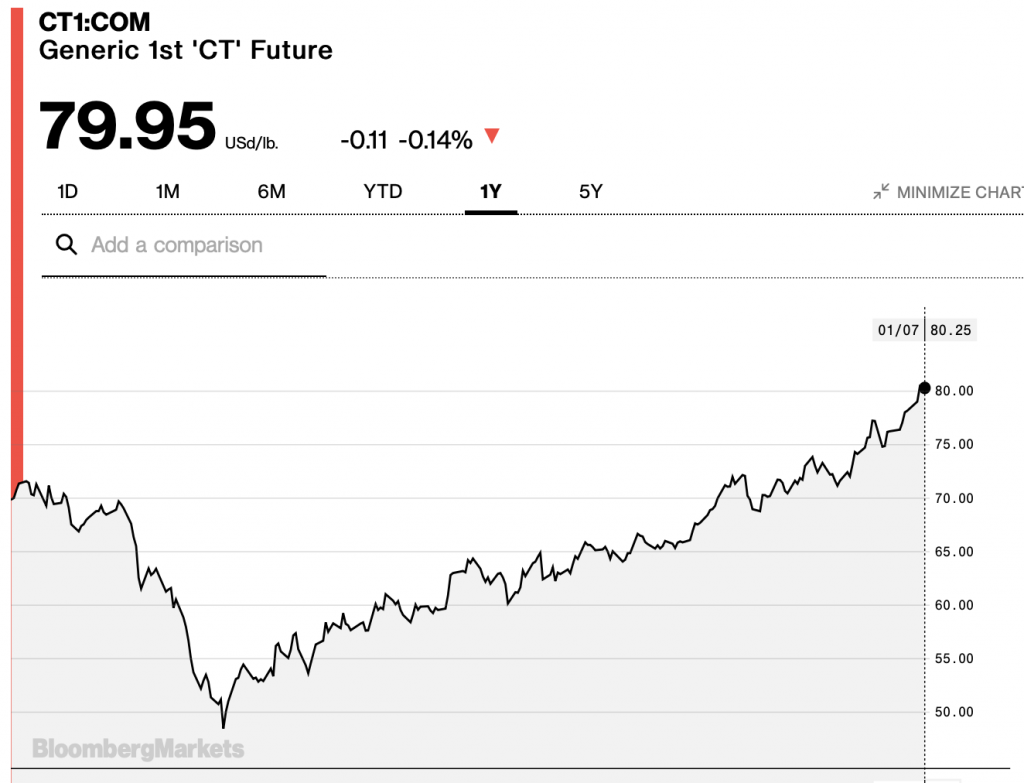

Cotton price (7th January 2021 : 80.25$) is higher than at the same time last year and it is at its highest level in nearly two years, thanks to a lack of rainfall in key-growing regions that has reduced expectations for the current crop. The U.S. Dept. of Agriculture expects the smallest domestic crop in five years. We can also add the recent scandal on forced labour in China (which produces 85% of China’s cotton and 20% of the global supply) that has put off many clothing makers and the US has banned China’s cotton in response to the scandal. All these events explain the rise in price of Cotton.

Cotton Supply & Demand

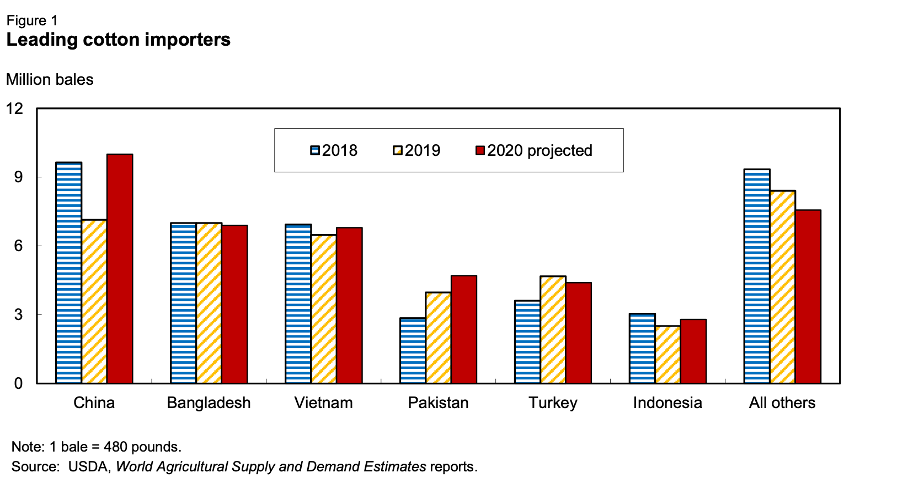

According to the latest estimate of the US Department of Agriculture made in December 2020, the imports of cotton are projected at 43.2 million bales which is 7.4% above last season. This major increase is mainly due to China which increases its imports due to higher local prices.

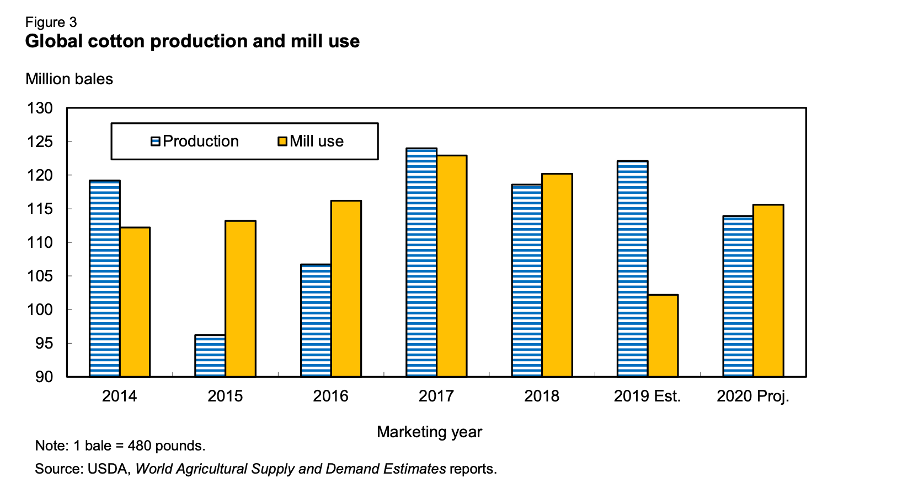

Production is projected at 113.9 million bales which is 8.2 million bales less than last season. The major reductions are in the United States, Brazil and Pakistan because of severe weather issues such as droughts, floods, hurricane, and so on that resulted in many abandoned acres.

Consumption is projected to increase by 13% to 115.6 million bales in 2020/21. This is mainly due to the fact that Covid-19 and the slowdown of the world economy it has caused, has led to a major reduction in world cotton demand in year 2019/20, so it is quite easy to perform better in 2021. Nevertheless, Covid-19 has not disappeared yet, and therefore 2021 brings its lot of uncertainties as well, even though the hope created by the vaccine has led to more optimistic projections for 2021, these projections are still below the volumes from previous years that were over 120 million bales.

World stock of cotton are expected to decrease in many countries this season mainly because of the above-mentioned reasons, but it will be partially offset by an increase in production in India. China’s stock continues to decrease, nevertheless it remains the largest cotton stockholder in 2020/21 accounting for 37% of global cotton stocks.

The latest cotton supply and demand estimates show that world cotton stocks are projected to decrease by 2% in 2020/21 to 97.5 million bales against 99.4 million bales in 2019/20.

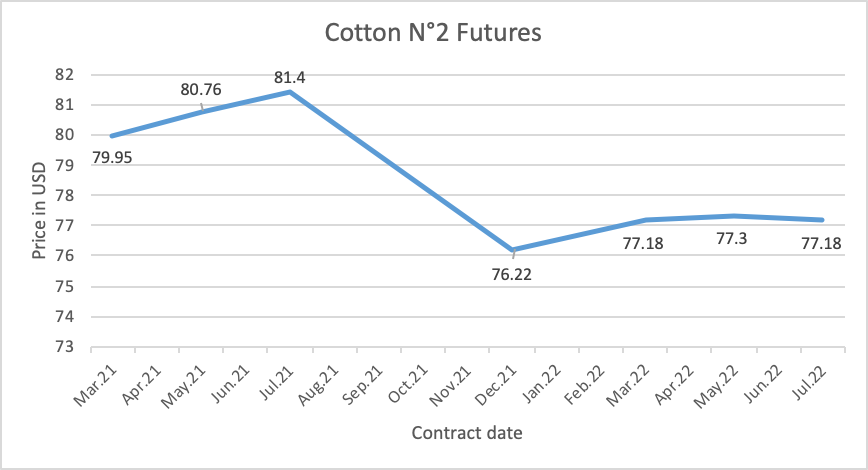

This could explain our future curves which is in contango till July 2021 and ends up in backwardation between July and December 2021. It could be explained by the fact that as we have seen demand will be higher than supply in 2020/21. We might imagine that till July 2021 the contango is explained by the fact that the 2019 crop will still be available until then.

Recommendations

The recent events concerning forced labour and the fact that USA has banned China’s cotton affects the price on the rise. That is why we need to have a close look at what is happening in these countries and how the market will change with the covid19 pandemic.

Futures prices are arising at least until July 2021 where it will be valued at 81.4 USD, so the best action to take for now is to go long on cotton investment.

Bibliography

BATHA, Emma, 2020. China accused of forcing 570,000 people to pick cotton in Xinjiang. Reuters [online]. 15 December 2020. [Viewed 4 January 2021]. Available from: https://www.reuters.com/article/china-cotton-forced-labour-trfn-idUSKBN28P2CM

CAMPICHE, Dr Jody, 2020. GOODBYE 2020: Cotton Outlook Hinges on Economic Recovery, Demand. Cotton Grower [online]. 28 December 2020. [Viewed 5 January 2021]. Available from: https://www.cottongrower.com/market-analysis/goodbye-2020-cotton-outlook-hinges-on-economic-recovery-demand/

Cotton Market Fundamentals and Monthly Cotton Price Outlook, [no date]. [online]. [Viewed 4 January 2021]. Available from: https://www.cottoninc.com/market-data/monthly-economic-newsletter/

Cotton No. 2 Futures | ICE, [no date]. [online]. [Viewed 5 January 2021]. Available from: https://www.theice.com/products/254/Cotton-No-2-Futures/data?marketId=5739902&span=2

Cotton Prices Rise as Lack of Rain Shrinks Crop – WSJ, [no date]. [online]. [Viewed 4 January 2021]. Available from: https://www.wsj.com/articles/cotton-prices-rise-as-lack-of-rain-shrinks-crop-11609764658

CT1 Commodity Quote – Generic 1st “CT” Future – Bloomberg Markets, [no date]. [online]. [Viewed 7 January 2021]. Available from: https://www.bloomberg.com/quote/CT1:COM

ICAC, [no date]. [online]. [Viewed 6 January 2021]. Available from: https://icac.org/News/NewsDetails?NewsId=2336&YearId=2020

WWW.FIBRE2FASHION.COM, [no date]. Global cotton prices now exceed pre-pandemic levels: USDA. [online]. [Viewed 5 January 2021]. Available from: http://www.fibre2fashion.com/news/textile-news/global-cotton-prices-now-exceed-pre-pandemic-levels-usda-271380-newsdetails.htm

Soybean – Bulletin 3 – 2021

PRICE MOVEMENTS & INVENTORY LEVEL

Source: Trading Economics

Source: CME Group & USDA

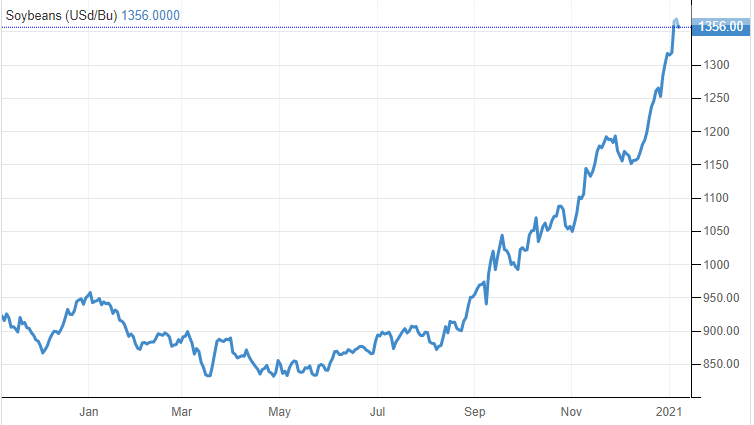

The current situation of the soybean market is that the US soybean prices are still increasing and are likely to continue in 2021. This increase is due to the fact that exports are still growing and that China shows a strong demand.

The graphs above confirm our statement from the last Bulletin, meaning that the supply is tight because of the end of the both major suppliers’ harvest, Brazil and US. Additionally, as already said, the production of soybeans in Brazil and Argentina is uncertain because of the La Niña phenomenon. Without forgetting the global pandemic crisis.

China is the most important US soybean buyer as they account for over 58% of total export according to the USDA. Additionally, China is expected to continue its intense purchasing as the country is expected to totally recover from the African swine fever disease.

US soybeans prices are expected to continue its increase as the domestic crushing are rising and the ending stock will be lowered.

The demand for soybean meal-based animal feed has increased because of meat exports and soybean oil increased because of the rise of biodiesel purchases.

As a reminder, the agreement between the United States and China suggests that China will buy at least 36.5Bn US$ worth of American agricultural product in 2020.

GLOBAL WARMING AND LA NIÑA

As we have seen this year, the harvest of soybeans has been altered by La Niña, which is a meteorological condition responsible for the low level of rainfalls resulting in a delayed plantation. The underlying issue might be more complex though, since global warming is known to be an accelerator of La Niña. In fact, scientists do not seem to have a definite answer, but the phenomenon could take place more frequently and be more pronounced, which could make the soybean production – and ultimately supply – even more uncertain in the next few years.

Since La Niña takes place in the Pacific Ocean and, one solution to meet the demand needs – and thus avoid price levels going through the roof – could be an increase in production in other major producing countries located elsewhere, for example in India and China, which could partially ensure its increasing local demand. One issue persists though, which is the fact that China is also hit by La Niña. Fortunately, analyses have shown that, over the long run, La Niña events tend to operate at the advantage of grain productivity in China. Moreover, The United States, which are the second largest soybean producers, could also increase the supply to balance the uncertainty ruling over Latin American countries.

Of course, increasing production requires a certain level of technological advance. It also requires a larger number of producers, which is why this process would require investments and government subsidies.

SUBSTITUTES

The primary uses of soybeans are food, biofuel and flour.

Soybeans are used for feed because they have a high concentration of proteins with ~48%. One of the substitutes for this use could be corn even though it has a much lower concentration of proteins with ~9%. Moreover, corn is cheaper than soybean. For a bushel of soybeans it costs US$ 12.64, which is three times the price of corn, US$ 4.51. Furthermore, instead of using soy flour, it can be replaced by wheat flour.

In order to replace the biofuel made by soybean, they can instead use crude palm oil but it is more expensive than soybean and has major negative effects on the environment like deforestation.

We can find some substitutes to soybean but none of them has better elements than this commodity.

RECOMMENDATION

Prices will continue to increase due to the high demand and slow supply. Moreover, the supply is uncertain since there are weather issues in Latin America. Another point we have to take into account is the tariffs between US and China with the election of Joe Biden who said that it was a failure and wants to do a full review of the agreements.

For all of these reasons, we recommend going long over the next month since the supply is uncertain but also low.

REFERENCES

China’s November soybean imports from U.S. surge one year after trade deal, 2020. Successful Farming [online]. [Viewed 29 December 2020]. Available from: https://www.agriculture.com/markets/newswire/update-1-chinas-nov-soybean-imports-from-us-surge-on-year-after-trade-deal

Commodities 2021: US soybean prices likely to rise on high exports, tight stocks | S&P Global Platts, 2020. [online]. [Viewed 29 December 2020]. Available from: https://www.spglobal.com/platts/en/market-insights/latest-news/agriculture/122220-commodities-2021-us-soybean-prices-likely-to-rise-on-high-exports-tight-stocks

CONSTABLE, Simon, [no date]. Bad Weather Could Hurt Soybean Crops, Lifting Prices. [online]. [Viewed 29 December 2020]. Available from: https://www.barrons.com/articles/bad-weather-could-hurt-soybean-crops-that-will-help-lift-prices-51608676202

Corn Prices – 59 Year Historical Chart, [no date]. [online]. [Viewed 29 December 2020]. Available from: https://www.macrotrends.net/2532/corn-prices-historical-chart-data

Explosive soybean price picture forming, analyst says, 2020. Successful Farming [online]. [Viewed 29 December 2020]. Available from: https://www.agriculture.com/markets/analysis/explosive-soybean-price-picture-forming-analyst-says

Palm oil and soy oil for biofuels linked to high rates of deforestation – new study | Transport & Environment, [no date]. [online]. [Viewed 29 December 2020]. Available from: https://www.transportenvironment.org/press/palm-oil-and-soy-oil-biofuels-linked-high-rates-deforestation-new-study

snd_cbt.pdf, [no date]. [online]. [Viewed 29 December 2020]. Available from: https://www.cmegroup.com/trading/agricultural/files/ht_charts/snd_cbt.pdf

Soybean Prices – 45 Year Historical Chart, [no date]. [online]. [Viewed 29 December 2020]. Available from: https://www.macrotrends.net/2531/soybean-prices-historical-chart-data

Soybeans | 1977-2020 Data | 2021-2022 Forecast | Price | Quote | Chart | Historical, [no date]. [online]. [Viewed 29 December 2020]. Available from: https://tradingeconomics.com/commodity/soybeans

Brazilian soybean planting slowest in a decade despite rains: AgRural | S&P Global Platts, 2020. [online]. [Viewed 29 December 2020]. Available from: https://www.spglobal.com/platts/en/market-insights/latest-news/agriculture/101920-brazilian-soybean-planting-slowest-in-a-decade-despite-rains-agrural

Geosys How is La Niña impacting Brazilian and Argentina crops?, 2020. UrtheCast [online]. [Viewed 29 December 2020]. Available from: https://www.urthecast.com/how-is-la-nina-impacting-brazilian-and-argentina-crops/

LEMONICK, Michael D., [no date]. Global Warming May Worsen Effects of El Niño, La Niña Events. [online]. [Viewed 29 December 2020]. Available from: https://www.climatecentral.org/news/is-texas-toast

LI, Yanyun, STRAPASSON, Alexandre and ROJAS, Oscar, 2020. Assessment of El Niño and La Niña impacts on China: Enhancing the Early Warning System on Food and Agriculture. Weather and Climate Extremes. 1 March 2020. Vol. 27, p. 100208. DOI 10.1016/j.wace.2019.100208.

Group 3 – K

Maxime DOLLA, Mahona PENNA, Romane POUCHON

Battery Material Bulletin n°3

Nickel in batteries

There are two classifications of batteries: primary batteries which are disposable meaning for single-use and secondary batteries which can be recharged and reused. Nickel is an essential component for the cathodes of many secondary battery designs, including lithium-ion (Li-ion) batteries that power much of the electric vehicle revolution.

Using nickel in car batteries offers greater energy density and storage at a lower cost, delivering a longer range for vehicles, currently one of the restraints to electrical vehicle uptake.

Further advances in nickel-containing battery technology mean it is set for an increasing role in energy storage systems, helping make the cost of each kWh of battery storage more competitive. It is making energy production from intermittent renewable energy sources such as wind and solar replace fossil fuels more viable. The challenge is that the wind doesn’t blow, and the sun doesn’t shine on demand. This is why batteries are being deployed to capture energy and release it when required, helping stabilize the complex and widespread electricity infrastructure.

The demand for nickel comes predominantly from the stainless-steel industry. Only 5 to 8 percent of the demand for nickel comes from batteries. However, the type of nickel separates the market. Indeed, to make stainless steel both Class 1 and Class 2 nickel can be used. For the battery industry, on the other hand, the type of nickel used is extremely important. It defines the quality and performance of the batteries. The battery industry can only use Class 1 nickel.

At best only 46 percent of the world’s nickel (Class 1) production can be used in batteries.

According to McKinsey, the global demand for Class 1 nickel could skyrocket. They expect the demand to increase from 2.2 million metric tons to 3.5 to 4 million metric tons by 2030.

A scarcity of sulfide deposits is contributing to a looming shortage of Class 1 nickel.

The current challenge is then to nearly double the supply of Class 1 nickel while meeting environmental, social, and corporate governance requirements. Indeed, the industry received a clear signal when Tesla’s Elon Musk stated that he would award a “giant contract for a long period of time if you mine nickel efficiently and in an environmentally sensitive way”.

Cobalt

Supply and demand outlook for Europe: From mining to recycling, is it going to be sufficient to counter the growing demand in batteries?

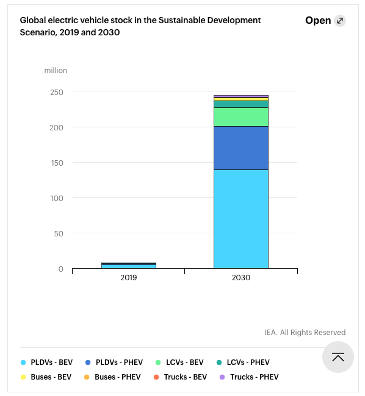

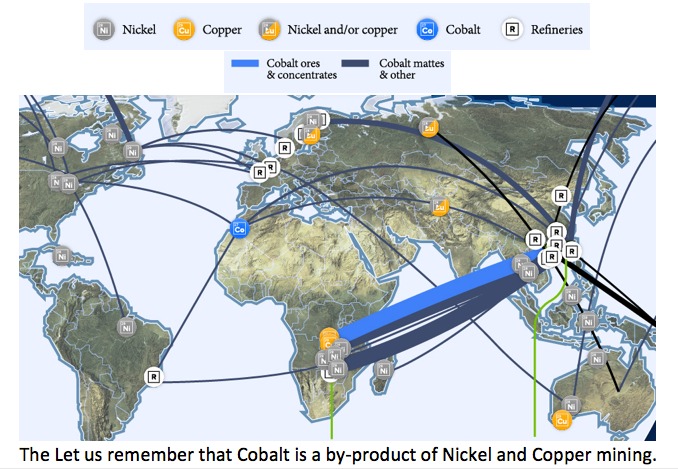

The EU has launched several project for mining exploration in order to depend less on the CHINA-DRC supply chain. In the long term, Cobalt is bound to become a fundamental resource as the EVs and electronical device market are growing every year (The number of EVs is expected to reach 250mio by 2030 compared to 8mio in 2019). Quick reminder: DRC stands for about 55% of the global raw Cobalt supply and China stands at an astonishing 80% of refined Cobalt supply. We had also seen that 8 out of the 14 main cobalt refineries are based in China.

https://www.iea.org/reports/global-ev-outlook-2020

We had seen in the previous bulletin that Canada, other than being one of the biggest Cobalt producers had built the very first North American Cobalt refinery for export and is doing mining exploration over the country in order to find new resources of Cobalt[1] and to disrupt the CHINA-DRC monopoly over the supply chain.

Image source from: https://www.visualcapitalist.com/ethical-supply-the-search-for-cobalt-beyond-the-congo/

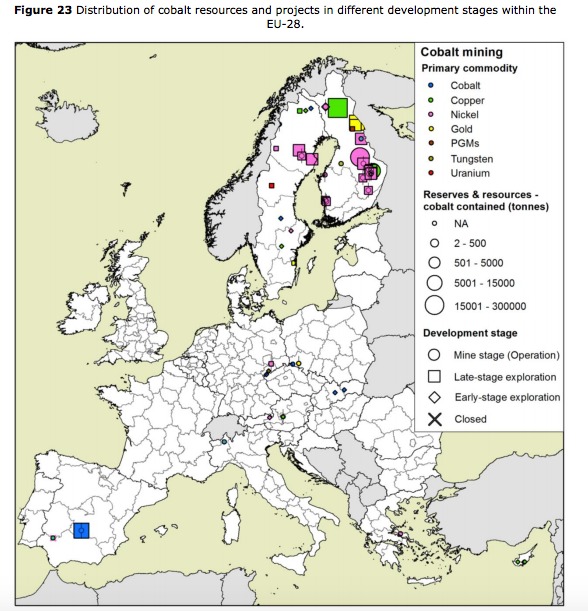

What about the EU?

If we look at the map above, we can see that the EU has refineries but not a lot of production. Its few mining areas are situated in Finland. Here is a map of the mining places and the projects put in place by the EU in order to counter the future shortage of the commodity.

https://publications.jrc.ec.europa.eu/repository/bitstream/JRC112285/jrc112285_cobalt.pdf

(Between exploration and actual start of operation, a time frame of 10 years can occur)

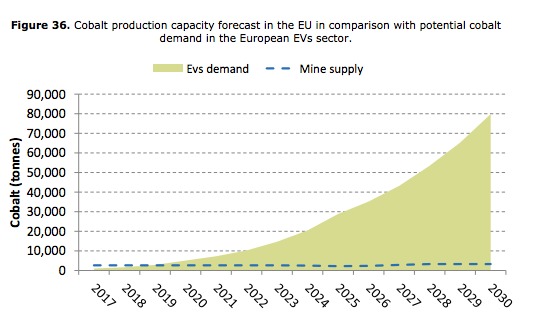

The EU cobalt demand is increasing over time and we can clearly see that it cannot supply itself currently making it highly dependent on the other suppliers.

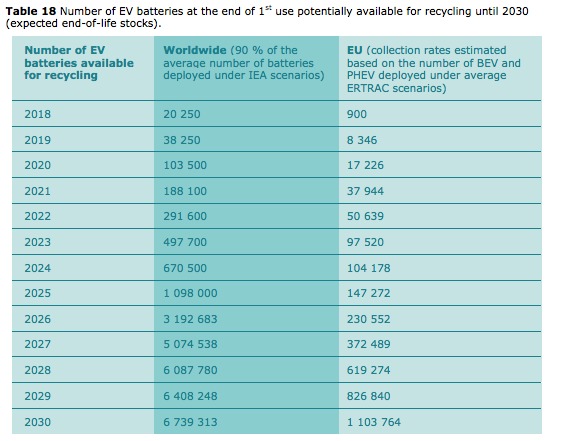

While waiting for the cobalt mining discoveries, the EU is trying to concentrate its effort in battery recycling. Right now, there is not enough old battery supply to make it really viable, but looking at the forecast of the EV market, recycling will definitely become an important source of cobalt supply. The estimate rate of used battery collection is 90%.

https://publications.jrc.ec.europa.eu/repository/bitstream/JRC112285/jrc112285_cobalt.pdf

The estimations in the table assume an average lifetime of 8 years for each vehicle battery placed on the market. The potential amounts of recycled cobalt generated from old vehicles deployed in the EU are estimated at 500 tonnes in 2025 and may amount, on average, to 5 500 tonnes in 2030. This would mean that in 2030, the recycling could provide for about 10 % of European cobalt consumption in the EVs sector (see graph figure 36 above).

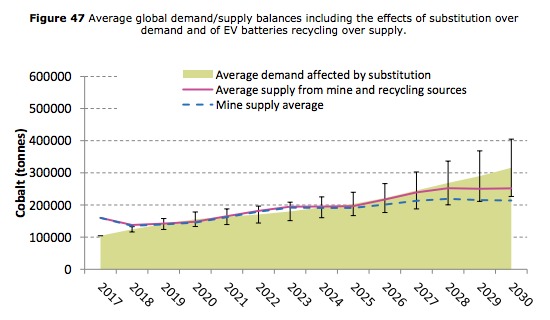

World cobalt demand may be subject to a growth rate of between 7 % and 13 % depending on the cobalt forecast usage for different areas (EVs, alloy, etc.). Between 2017 and 2030, the average cobalt consumption will amount at about 220 000 tonnes in 2025 and 390 000 tonnes in 2030. In the EU, cobalt demand will amount to 53 500 tonnes in 2025 and increasing to 108 000 tonnes in 2030.

Global

https://publications.jrc.ec.europa.eu/repository/bitstream/JRC112285/jrc112285_cobalt.pdf

Global

https://publications.jrc.ec.europa.eu/repository/bitstream/JRC112285/jrc112285_cobalt.pdf

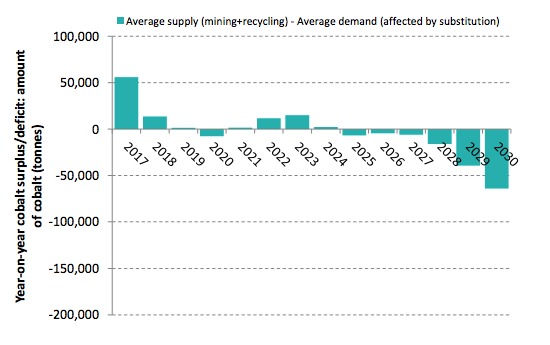

The report forecast a cobalt shortage in 5 years’ time. We can foresee an increase in the price of the Cobalt worldwide and mostly in the EU. Commodity companies such as Glencore (no1 in Cobalt mining) knowing this will surely profit to put higher margins as the product will become scarce.

Sources:

https://www.mining.com/chart-chinas-stranglehold-on-electric-car-battery-supply-chain/

https://campus.hesge.ch/commodity-trading/?p=1271

https://publications.jrc.ec.europa.eu/repository/bitstream/JRC112285/jrc112285_cobalt.pdf

https://publications.jrc.ec.europa.eu/repository/bitstream/JRC112285/jrc112285_cobalt.pdf

https://publications.jrc.ec.europa.eu/repository/bitstream/JRC112285/jrc112285_cobalt.pdf

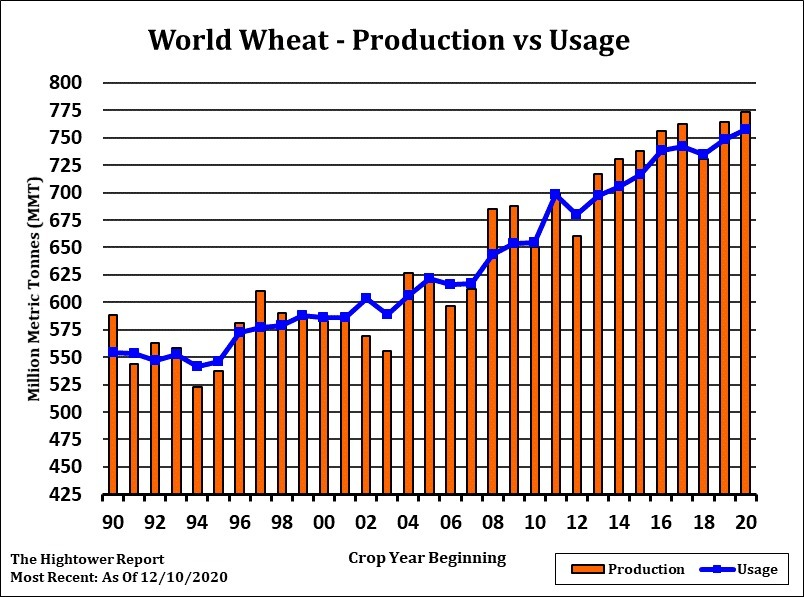

Bulletin#3 – The largest exporter of wheat reducing exportation

By Lyticia Wouguia, Christopher Delfin, Piratharsan Poologanathan

Russia imposes export tax and quota

Russia, one of the world’s largest wheat exporters, recently issued a list of orders aimed at stabilising domestic food prices, including a grain export quota and wheat export tax. These new measures will start from 15th February 2021 until 30th June 2021. The government introduced a quota for overseas shipments of wheat, rye, barley and corn limiting exports to 17.5 million tonnes. In addition, along with that quota, they also implemented a wheat export tax of 25 euros or 30.40 US dollars per tonne. Furthermore, if export volumes are higher than the quota, the tax for wheat would rise to 50% of the customs price or 100 euros per tonne, whichever is higher.

The figure below are the futures prices in the black sea wheat market. There is a steady increase in the beginning of the year until May, which makes the market in a normal curve. The reason behind the increase is partially due to the new measures which were mentioned in the previous paragraph. As the regulation is from Feb-June, the tax could reduce Russia’s wheat export which makes the futures prices higher in those months. Another reason for high prices is due to low wheat production caused by prolonged dry weather and a strong demand from global buyers. The bad weather condition has disrupted and delayed planting of the major wheat producing and exporting countries.

Black sea wheat futures

Turkey grains import tax cut likely to be extended

The Turkish government decided to suspend tariffs on wheat, maize and barley at the end of October in order to support its domestic milling market against a backdrop of rising international prices and concerns about local food security. The suspension is expected to end in early calendar year 2021. But as the Covid-19 pandemic continues to threaten domestic supplies, it seems likely that import tariffs will remain lifted at least until the end of the current crop year, on 30 June 2021.

The extension of the tax reduction until next year would allow importers more time to reap the benefits of this measure, as the Turkish lira depreciates in value – caused by inflation and concerns about the Covid-19 recession. Indeed, Covid-19 has increased the costs of international wheat supply for Turkish buyers in recent weeks.

Demand

The global demand is increasing due to several reasons. The main importer’s countries are increasing the amount of wheat entering their land. The global consumption has reached 757.8 million for 2020 and 2021. Even though the production has increased by 1.2 million to reach the record global production at 773.7 million. It is not enough to reach the demand of certain countries. Indeed, China, for example, has increased their demand. It is mainly explained by the need to feed livestock. China is not the only one to increase, Pakistan as well has raised the import. Furthermore, the world ending stock is expected to lower for 2020/21.

Supply

Due to the increasing demand, the supply is looking for larger producers. As explained in the previous bulletin, the australian production is expected to increase. Russia’a production has also increased. Nevertheless, in order to protect the local farmer from raising prices, they will impose a tax on export in the near future. Canada’s wheat production has a slight increase in their production.

Recommendation

Due to the new measures, this has triggered volatility in global wheat prices. A trader should look for different markets in order to make profit and avoid the uncertainties. It is also important to check for trends in the industry and futures markets as demand keeps on increasing. In our opinion, it is better to lock in prices today before the regulations come into effect in mid-February.

Sources:

https://www.barchart.com/futures/quotes/KF*0

https://www.argusmedia.com/en/news/2157551-turkey-grains-import-tax-cut-likely-to-be-extended

http://dtn.agfax.com/index.cfm?show=62&subtype=5

https://www.usda.gov/oce/commodity/wasde/wasde1220.pdf

https://www.cmegroup.com/trading/agricultural/wheat-reports.html

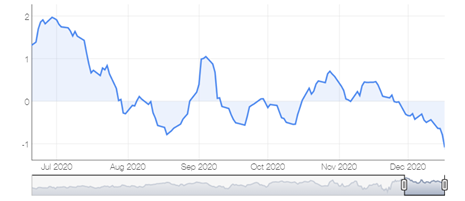

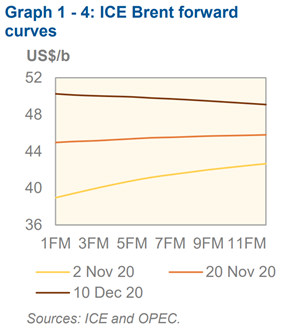

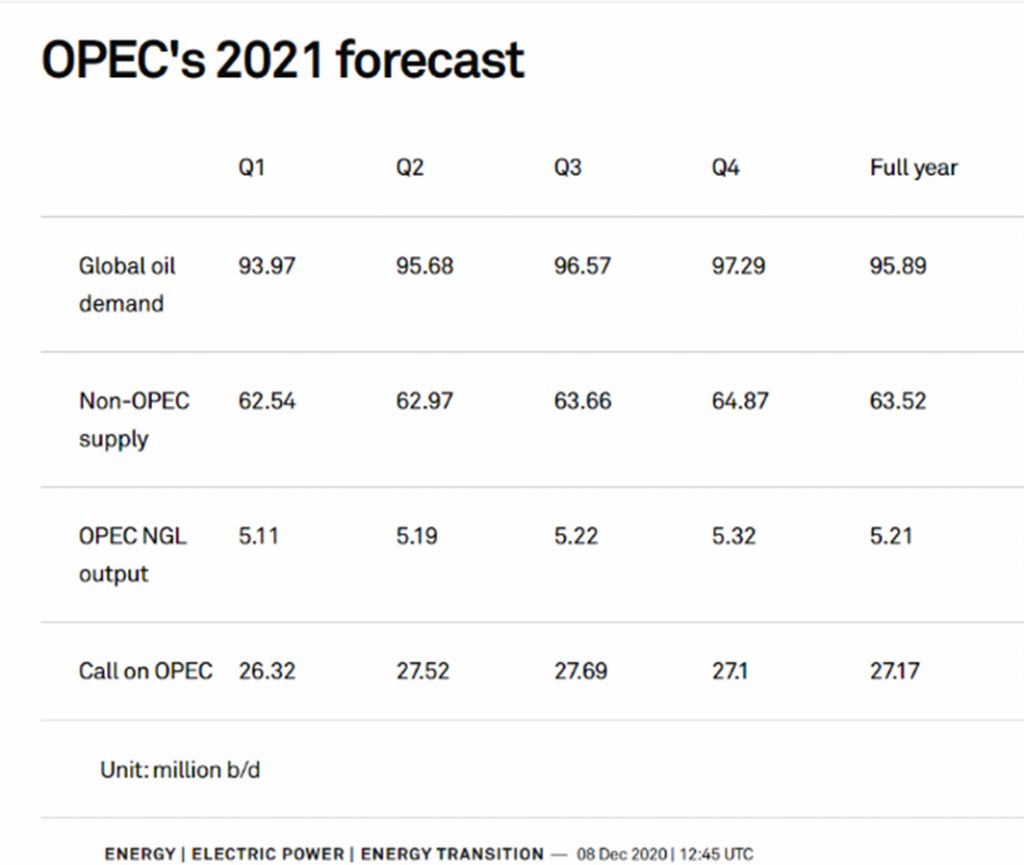

Hope for a vaccine, and OPEC+ new terms impact on Russian Crude. Weekly bulletin #3

Price mouvement

At the OPEC+ meeting on 30 November, it was decided to increase production by 500,000bp each month from January if the situation allows it at their next meeting in early January. The hope of a positive vaccine has a beneficial effect on the continuing rise in the benchmark prices.

On the oil market, the demand from Asia remains strong but prices are constrained by low refinery margins, increased production and still high stocks. Uncertainties regarding oil demand remain high. Forecasts expecting a decrease by the end of the year followed by an increase in the course of 2021.

Source: https://oilprice.com/oil-price-charts/block/1

Differentials

Since the end of November, the differential in price between Brent (light sweet) and Urals (medium sour) has returned to a discount because supply is stronger than demand.

Source: https://www.neste.com/investors/market-data/urals-brent-price-difference

Forward curves

The sustained recovery of the Libyan supply, the weak demand from European refiners and the context of mobility restrictions maintained the contango of November. Then the strong demand from Asia, which reduced unsold volumes and the optimism of a vaccine enabled the contango to be flattened, ending up on backwardation for the December forecasts.

Source:https://www.opec.org/opec_web/en/publications/338.htm

Demand and supply key drivers

What will be driving the market for the next weeks is the evolution of the new OPEC+ agreements, that were established the 3rd of December, they decided to gradually increase production from January, and meet monthly afterward. Russian production was around 10 million barrels per day in November, which was at a low compared to the previous year, mostly due to the cuts. Production will still be reduced to 8.99 million B/D in December, followed by a gradual increase of 500,000 B/D starting January. Demand is indeed expected to rise, but that remains to be seen, as it heavily relies on the pandemic evolution, and the vaccine efficiency, whose fast approval and testing created a price rally. Nevertheless, analyst have lowered their forecast for 2021.

Russia has recently signalled it is bracing for a drastic decline in oil demand, as they think consumption peaked already and that the long term is subject to high risk. This situation might well totally change how Russia will operate, as they intend to switch to greener energy, such as hydrogen. As a matter of fact, companies, such as Gazprom, intend to be producing the clean energy in four years. Russia has already made a roadmap of how they intend to swap from oil to hydrogen, and this will surely change the soviet’s economy drastically.

However, there are some good news, as 50% of the easing in the OPEC+ cuts will benefit Russia and Saudi Arabia, meaning they will be able to produce more, though this also means demand will be affected, and recover more slowly in Q1 of 2021.

Finally, the second lockdown keeps on influencing demand, and this will continue as the World is going through societal shifts concerning travels. Gasoline and diesel demand being at 90% of their usual levels and jet fuel only at 50% are indicators of this situation. This being said, Asia, who favours Russian crude such as ESPO, has been less affected by the second lockdown and is a key player regarding the demand, with countries like China still importing big quantities of crude oil.

As for stock levels, they are as planned difficult to come by for Russia. However, a global overview show how they rose during those last months in the world.

Source: https://www.eia.gov/outlooks/steo/report/global_oil.php

Recommandations:

On the short term, we recommend to have a long postition as the current measures taken by the OPEC+ organisation are working. However, on the medium to long run, we advise to remain cautious and see how the easing in the production cuts will affect the market, as well as the pandemic evolution with the new vaccines. It is also important to verify if the backwardation will remain before taking any decisions.

Sources:

Oil price charts. Consulté le 14 décembre

https://oilprice.com/oil-price-charts/block/1

Brent crude oil review. Consulté le 15 décembre

https://www.cmegroup.com/trading/energy/crude-oil/brent-crude-oil.html

Urals Brent price differences. Consulté le 16 décembre.

https://www.neste.com/investors/market-data/urals-brent-price-difference

Monthly oil market review. Consulté le 16 décembre

https://www.opec.org/opec_web/en/publications/338.htm

“OPEC – Monthly Oil Market Report” Consulté le 16 Décembre

https://www.opec.org/opec_web/en/publications/338.htm

“Russian Energy Minister Sees 2 Million Bpd OPEC+ Output Increase In April” Consulté le 16 Décembre

https://oilprice.com/Energy/Energy-General/Russian-Energy-Minister-Sees-2-Million-Bpd-OPEC-Output-Increase-In-April.html

“Oil prices rise on vaccine hopes, ship explosion at Saudi Arabia” Consulté le 16 Dévembre

https://energy.economictimes.indiatimes.com/news/oil-and-gas/oil-prices-rise-on-vaccine-hopes-ship-explosion-at-saudi-arabia/79717728

“Russia’s Nov oil output steady on month at 10 mil b/d”. Consulté le 13 Décembre

https://www.spglobal.com/platts/en/market-insights/latest-news/oil/120220-russias-nov-oil-output-steady-on-month-at-10-mil-bd

“Russia braces for permanent decline in oil demand”. Consulté le 13 Décembre

https://oilprice.com/Energy/Crude-Oil/Russia-Braces-For-Permanent-Decline-In-Oil-Demand.html

“The OPEC Mission to balance oil markets is just getting started”. Consulté le 14 Décembre

https://oilprice.com/Energy/Energy-General/The-OPEC-Mission-To-Balance-Oil-Markets-Is-Just-Getting-Started.html

China impacting the world

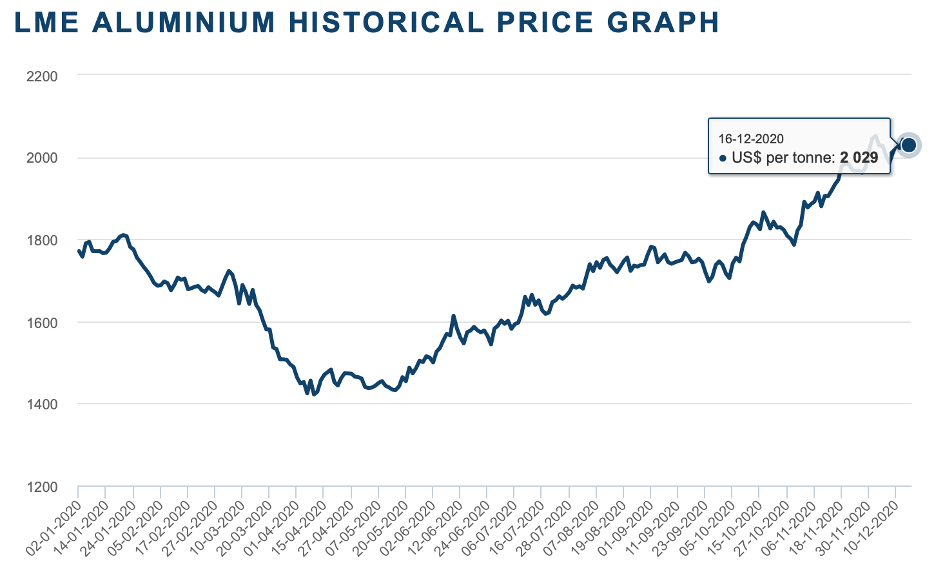

Price movement recap

Prices on LME are still above what they were before the COVID-19 lockdown in March 2020 but remain lower than on SHFE. China’s demand is very strong and has consequently seen domestic prices increase. Not forgetting the government injecting money to re-boost the economy, especially in the infrastructure sector.

This price increase has led to a boost in output, which was 3.18 million tonnes in November, an increase of almost 9% compared to November 2019. The current price is encouraging smelters in China.

In addition, there is a Chinese need for automobile production which has also led to an increase in aluminium price.

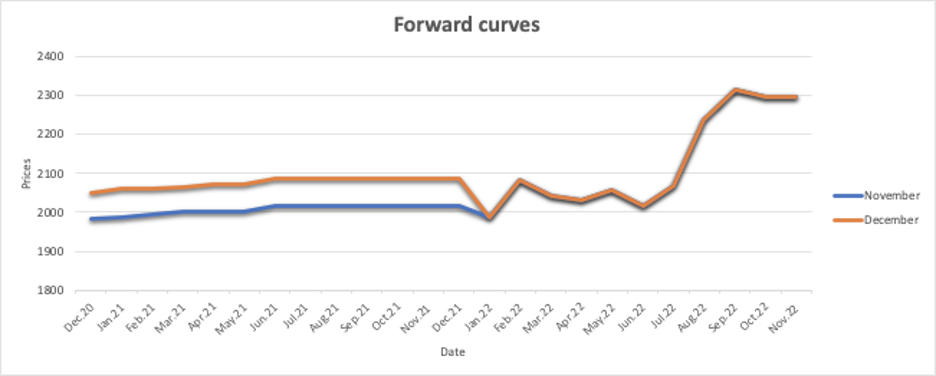

Forward curve

The price has increased compared to the previous month for the same delivery period.

For the following year, the curve is almost flat in a small contango, demonstrating an uncertainty that the curve can shift at any time. As it does not increase substantially we could argue that it may not cover the costs of financing and storage for delivery in the upcoming months.

Supply and demand dynamic

From the supply side, an increased focus is given to the can’s recycling sector meaning secondary aluminium is expected to take more and more space in supply. Robert Budway, president of Can Manufacturers Institute said that: “More than 90 percent of these recycled cans get turned into aluminium sheets used to make new beverage cans. These used cans plus other scrap metal create an average recycled content rate of 73 percent, which is exponentially higher than any competing substrate.” In parallel, more and more companies such as UC Rusal, Russian Federation major aluminium company, are focusing on making their smelter more sustainable by obtaining certifications by the Aluminium Stewardship Initiative.

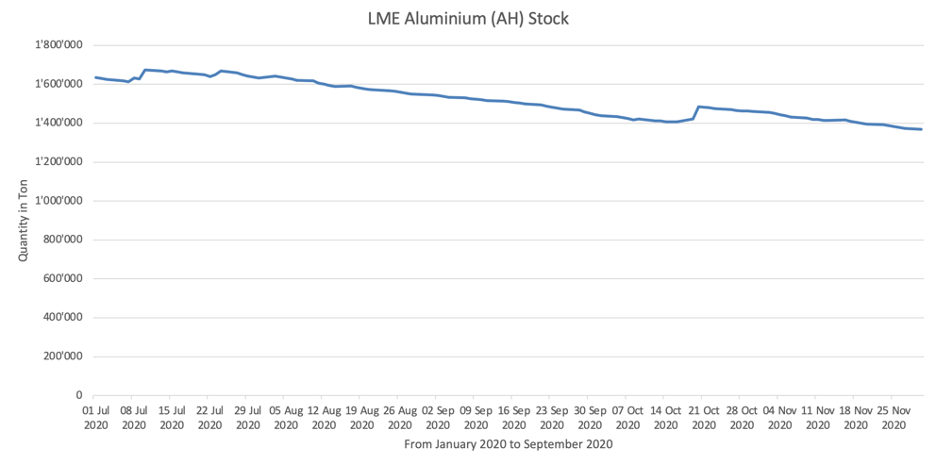

Inventory levels

The stock level of LME is still decreasing. China representing 55% of the global output has seen its production increase since April 2020 as its economy returns to normality after the COVID-19. Besides, China which was a net exporter is now a net importer of primary aluminium due to the increase of its own demand and a decrease of exports as the rest of the world struggles to recover from the global pandemic. The inventory on the Shanghai Metal Exchange keeps decreasing showing how tight the China aluminium market is and impacting directly the London Metal Exchange. Moreover, importation of aluminium became much more profitable in China, and as the demand in the country is high, companies tend to import more.

For a country producing a majority of the world’s supply, we would not expect them to become a net importer. One reason is a fluctuation for the US dollar, as the Chinese yuan became stronger against the dollar as well as the tight Chinese inventory.

Recommendations

As the contango is relatively flat, we cannot guarantee that storing and financing costs will be covered. Trading behaviour will be influenced by the forward curve, here the contango does not have an important slope, so it may not be worth it to store the goods.

Beatriz Ferreira Caetano, Virginie Gruaz and Mingxin Ma

References

Aluminum Futures Quotes – CME Group, [no date]. [online]. [Viewed 17 December 2020]. Available from: https://www.cmegroup.com/trading/metals/base/aluminum_quotes_globex.html

CHINA AUTO: Vehicle output growth bolsters raw material prices in November | Metal Bulletin.com, [no date]. [online]. [Viewed 17 December 2020]. Available from: https://www.metalbulletin.com/Article/3966588/Aluminium/CHINA-AUTO-Vehicle-output-growth-bolsters-raw-material-prices-in-November.html

Five More Rusal Facilities Certified By Aluminium Stewardship Initiative, 2020. Aluminium Insider[online]. [Viewed 17 December 2020]. Available from: https://aluminiuminsider.com/five-more-rusal-facilities-certified-by-aluminium-stewardship-initiative/

HORNER, Will, 2020. Aluminum Prices Surge as Chinese Demand Accelerates. Wall Street Journal[online]. 20 October 2020. [Viewed 17 December 2020]. Available from: https://www.wsj.com/articles/aluminum-prices-surge-as-chinese-demand-accelerates-11603200739

London Metal Exchange: LME Aluminium, [no date]. [online]. [Viewed 17 December 2020]. Available from: https://www.lme.com/en-GB/Metals/Non-ferrous/Aluminium#tabIndex=2

London Metal Exchange: Stocks summary, [no date]. [online]. [Viewed 17 December 2020]. Available from: https://www.lme.com/Market-Data/Reports-and-data/Warehouse-and-stocks-reports/Stocks-summary

MARKETSCREENER, [no date]. China Nov aluminium output hits daily record high | MarketScreener. [online]. [Viewed 17 December 2020]. Available from: https://www.marketscreener.com/quote/commodity/LME-ALUMINIUM-CASH-16159/news/China-Nov-aluminium-output-hits-daily-record-high-32011792/

Metal stocks to gain from China’s rising demand, 2020. The Malaysian Reserve [online]. [Viewed 17 December 2020]. Available from: https://themalaysianreserve.com/2020/12/14/metal-stocks-to-gain-from-chinas-rising-demand/

Shanghai-bonded aluminium stocks plunge in Nov on open arb; zinc shows biggest increase | Metal Bulletin.com, [no date]. [online]. [Viewed 17 December 2020]. Available from: https://www.metalbulletin.com/Article/3964495/Aluminium/Shanghai-bonded-aluminium-stocks-plunge-in-Nov-on-open-arb-zinc-shows-biggest-increase.html

STAFF, 2020. Aluminum Association Report Emphasizes Aluminium Beverage Can’s Importance To Sustainability. Aluminium Insider [online]. 6 December 2020. [Viewed 17 December 2020]. Available from: https://aluminiuminsider.com/aluminum-association-report-emphasizes-aluminium-beverage-cans-importance-to-sustainability/

BULLETIN N°3 – INCREASED GLOBAL CORN TRADE,DRIVEN BY STRONG DEMAND FOR FEED IN CHINA

Source : bloomberg

PRICE

The strong demand from China has resulted in higher maize price over the past several months.

PRODUCTION

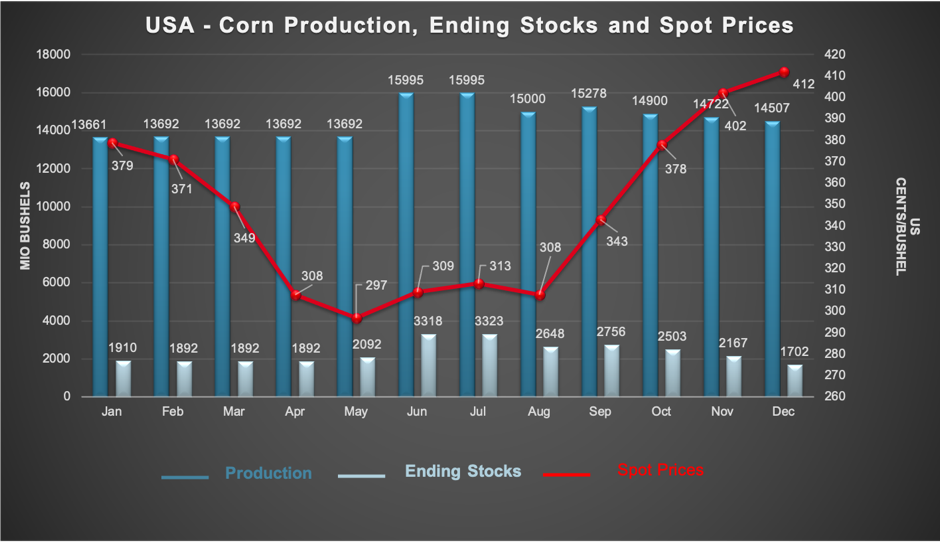

World maize production for 2020/2021 is forecast to a total of 1,143.6 million MT, down 1.1 million MT from the November forecast.

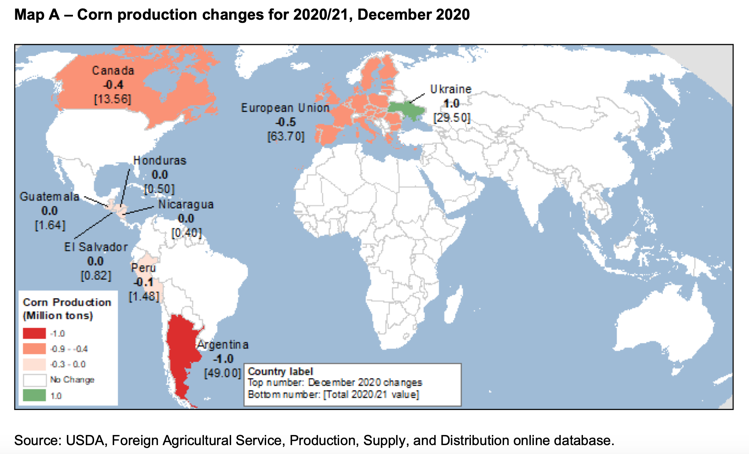

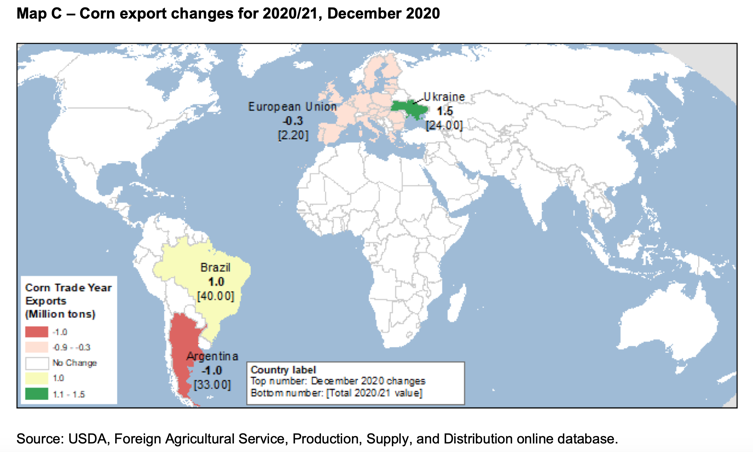

Argentina is suffering the consequences and the drought of “La Niña”. In fact, the area devoted to corn is expected to decrease by 2% compared to last month, from 50 million tons to 49 million tons. This is accounting for the largest decrease in production this month. The corn production in the EU has decreased by 0.5 million MT to 63.7 million MT because they experienced dry conditions during important parts of the crop development cycle in particular, in Bulgaria.

In the past Bulletin we saw that the corn production in Ukraine (4th largest exporter) for 2020/2021 has suffered from a severe drought which badly affected the production. This month corn production for 2020/21 has increased by 1.0 million MT from the previous month, compensating for some of the global declines. But the gap is still huge compared to last year -14%.

DEMAND

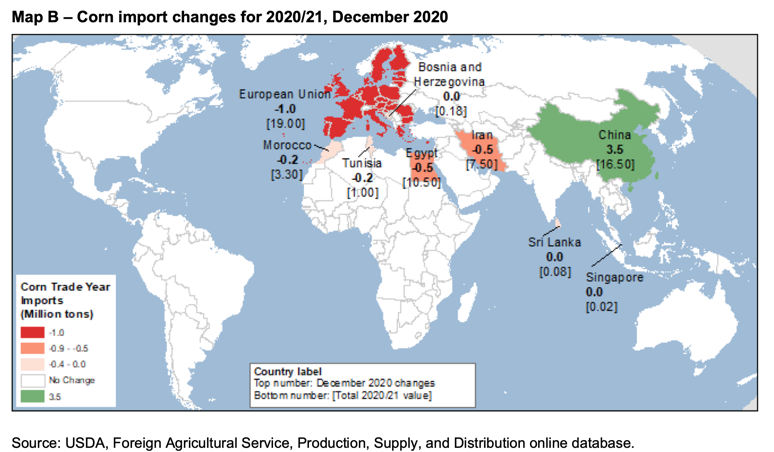

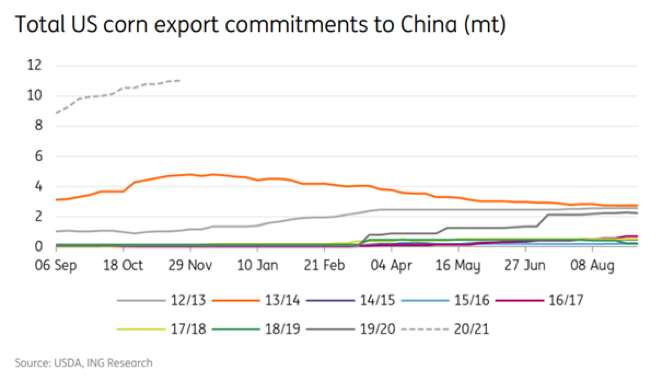

Despite the expected slowdown in feed usage due to COVID-19, several countries imported record volumes of corn in 2020. Corn imports are expected to increase in 2021 of 7% from last year’s record. This increase is largely due to China. China has been engaged since mid-year in securing corn and some substitutes (sorghum and barley) to meet the increasing demand for feed in the livestock sector.According to USDA International Agriculture Services, China’s corn imports are expected to triple to 22 million tons this season.

Total imports of maize from China increased by 3.5 million MT to 16.5 million this month. The main explanation for China’s increased demand for corn for animal feed is that pigs’ herds in China are beginning to recover from the African swine fever. One of their key resources are pigs, so the government has made the increasing of pork’s production in the country a high priority.

Globally, China’s increased imports of maize are offset in part by lower imports from several other major import markets.

Corn imports are subject to the tariff quota set by the World Trade Organization on a calendar year basis, but imports are already above the quota of 7.2 million tons only with the January-October period.

There is a trade war between the two big players but if we take a closer look, the relationship between the U.S. and China was never better, and the quantity of imports/exports of corn was never as considerable as it is now. Corn has risen to nearly 30% of US export sales.

China has submitted a draft law to ensure national food security and to reform the management of the key grain reserves in China. This project also includes the United States. Indeed, Trump had made an agreement with China for “phase 1”, which includes commitment purchases by China of agricultural products in 2020-2021.

ENDING STOCK

As we explain above the demand is superior to the supply side. The overall decrease for corn production and the growing demand from China lead to an urgent need for the ending stock. The production was estimated lower than the last month we lost almost 1million tons mainly caused by Argentina. Even if the South American countries did not suffer from the climate, the other producer countries (North hemisphere), registered a lower production and the harvest period is almost over now. The consumption is estimated to increase for 1.5 millions tons this month compared to November, largely sustained by China. The consumption in a month has increased to 2.5 millions tons. With a basic calculation we found that the demand exceeds the supply side to 14.5millions tons and that is why we assist to a decrease in ending stock. From November the ending stock lost almost 2.5 millions tons. All these factors explain the positive fluctuation for corn price.

FORWARD CURVE

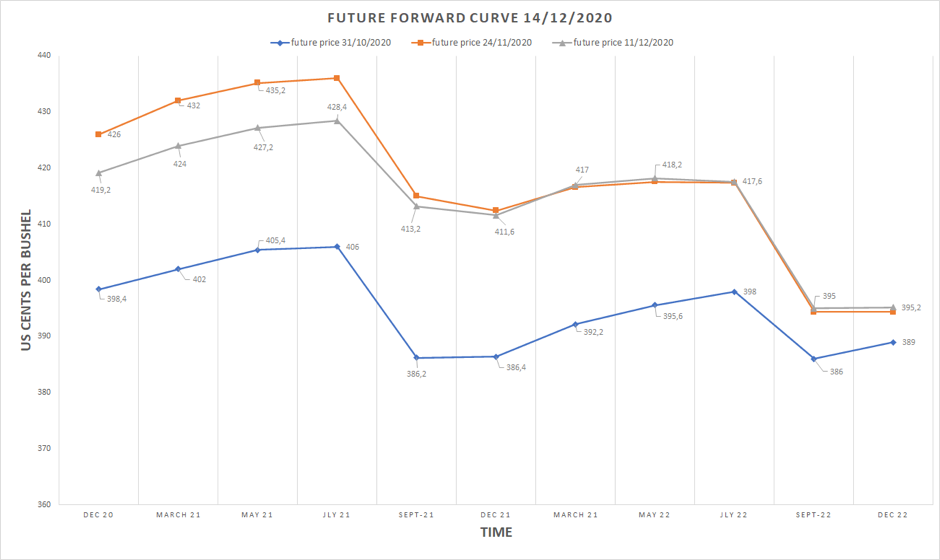

The shape of the forward curve for our three bulletins are almost identical due to seasonality. It is a normal curve (it is well supplied) from december to july (the message is to store) and goes into an inverse curve (the demand is hot) from july to december (the message is to deliver).

The prices agreed on the 11th of December are lower than the price agreed on the 24th of November for the seven upcoming contracts.

It is odd because supply decreases this month and demand increases which would normally result in higher price for the spot and future. We think that it is because the supply has decreased a lot because of Ukraine and the demand increased because of China resulting in higher prices agreed on the 24th November. And for the price agreed on the 11th of December, the supply of Ukraine increased from last month. It can also be hypothesized that the market overreacted last month. One of the reasons for this strong reaction is that the gap between production and demand between October and November tripled from almost -4 million tons (=lack of supply) to -12 million tons (+300% increase). Whereas this month we went from -12 to -14.5 million tons (20.8%).

RECOMMENDATION

As mentioned above, supply decreased this month and there is an increase in the demand from China. The gap between supply and demand has increased by 2.5Millions tons since last month. Therefore we assume that the spot price will increase too. We are still on a normal curve this month. Furthermore, the news of COVID-19 vaccine and the end of the lockdown in some countries will reassure the economics agents. Our recommendation from a trader point of view is to buy physically in the spot market, and sell futures on a later date if the slope is sufficient to overlap the storing and financing costs. The trader will make profit thanks to his benefit from the physical result and paper result.

Léo Millet, Maike Da Silva, Patrice Correia Cardoso & Cassandra Kirchhoff

SOURCE

cmd-strong-chinese-agri-purchases-likely-to-continue-in-2021.pdf, [sans date]. [en ligne]. [Consulté le 17 décembre 2020]. Disponible à l’adresse : https://think.ing.com/downloads/pdf/article/cmd-strong-chinese-agri-purchases-likely-to-continue-in-2021

Corn | USDA Foreign Agricultural Service, [sans date]. [en ligne]. [Consulté le 17 décembre 2020]. Disponible à l’adresse : https://www.fas.usda.gov/commodities/corn

Corn Futures Settlements – CME Group, [sans date]. [en ligne]. [Consulté le 17 décembre 2020]. Disponible à l’adresse : https://www.cmegroup.com/content/cmegroup/en/trading/agricultural/grain-and-oilseed/corn_quotes_settlements_futures.html

grain__1_.pdf, [sans date]. [en ligne]. [Consulté le 17 décembre 2020]. Disponible à l’adresse :https://downloads.usda.library.cornell.edu/usda-esmis/files/zs25x844t/5425m323c/ns064z89z/grain__1_.pdf

grain.pdf, [sans date]. [en ligne]. [Consulté le 17 décembre 2020 a]. Disponible à l’adresse :https://apps.fas.usda.gov/psdonline/circulars/grain.pdf

grain.pdf, [sans date]. [en ligne]. [Consulté le 17 décembre 2020 b]. Disponible à l’adresse :https://downloads.usda.library.cornell.edu/usda-esmis/files/zs25x844t/7h14bd24q/gq67kf77r/grain.pdf

grain.pdf, [sans date]. [en ligne]. [Consulté le 17 décembre 2020 c]. Disponible à l’adresse :https://downloads.usda.library.cornell.edu/usda-esmis/files/zs25x844t/6w925260x/8049gw97t/grain.pdf

International Grains Council, [sans date]. [en ligne]. [Consulté le 17 décembre 2020]. Disponible à l’adresse :https://www.igc.int/en/markets/marketinfo-sd.aspx

Latest News | S&P Global Platts, [sans date]. [en ligne]. [Consulté le 17 décembre 2020]. Disponible à l’adresse : https://www.spglobal.com/platts/en/market-insights/latest-news

McConnell et Olson – 2020 – No Changes to the 202021 U.S. Corn Market Outlook.pdf, [sans date]. [en ligne]. [Consulté le 17 décembre 2020]. Disponible à l’adresse :https://www.ers.usda.gov/webdocs/outlooks/100046/fds-20l.pdf?v=5690.1

production.pdf, [sans date]. [en ligne]. [Consulté le 17 décembre 2020]. Disponible à l’adresse :https://apps.fas.usda.gov/psdonline/circulars/production.pdf

snd_cbt.pdf, [sans date]. [en ligne]. [Consulté le 17 décembre 2020]. Disponible à l’adresse :https://www.cmegroup.com/trading/agricultural/files/ht_charts/snd_cbt.pdf

wasde1220.pdf, [sans date]. [en ligne]. [Consulté le 17 décembre 2020]. Disponible à l’adresse :https://www.usda.gov/oce/commodity/wasde/wasde1220.pdf