Nickel in batteries

There are two classifications of batteries: primary batteries which are disposable meaning for single-use and secondary batteries which can be recharged and reused. Nickel is an essential component for the cathodes of many secondary battery designs, including lithium-ion (Li-ion) batteries that power much of the electric vehicle revolution.

Using nickel in car batteries offers greater energy density and storage at a lower cost, delivering a longer range for vehicles, currently one of the restraints to electrical vehicle uptake.

Further advances in nickel-containing battery technology mean it is set for an increasing role in energy storage systems, helping make the cost of each kWh of battery storage more competitive. It is making energy production from intermittent renewable energy sources such as wind and solar replace fossil fuels more viable. The challenge is that the wind doesn’t blow, and the sun doesn’t shine on demand. This is why batteries are being deployed to capture energy and release it when required, helping stabilize the complex and widespread electricity infrastructure.

The demand for nickel comes predominantly from the stainless-steel industry. Only 5 to 8 percent of the demand for nickel comes from batteries. However, the type of nickel separates the market. Indeed, to make stainless steel both Class 1 and Class 2 nickel can be used. For the battery industry, on the other hand, the type of nickel used is extremely important. It defines the quality and performance of the batteries. The battery industry can only use Class 1 nickel.

At best only 46 percent of the world’s nickel (Class 1) production can be used in batteries.

According to McKinsey, the global demand for Class 1 nickel could skyrocket. They expect the demand to increase from 2.2 million metric tons to 3.5 to 4 million metric tons by 2030.

A scarcity of sulfide deposits is contributing to a looming shortage of Class 1 nickel.

The current challenge is then to nearly double the supply of Class 1 nickel while meeting environmental, social, and corporate governance requirements. Indeed, the industry received a clear signal when Tesla’s Elon Musk stated that he would award a “giant contract for a long period of time if you mine nickel efficiently and in an environmentally sensitive way”.

Cobalt

Supply and demand outlook for Europe: From mining to recycling, is it going to be sufficient to counter the growing demand in batteries?

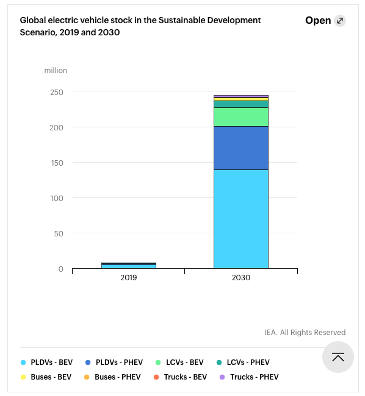

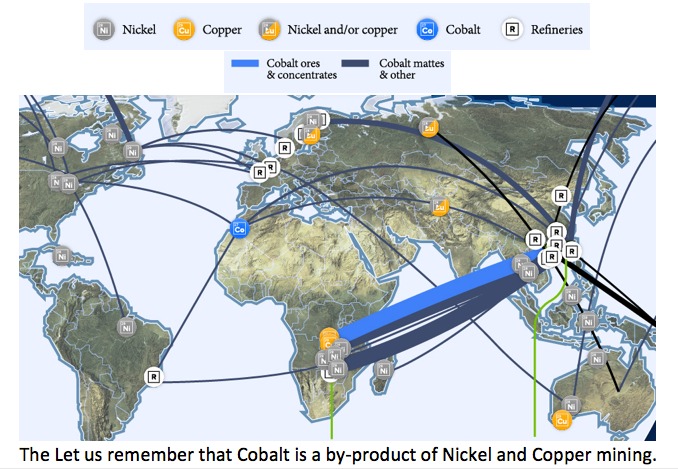

The EU has launched several project for mining exploration in order to depend less on the CHINA-DRC supply chain. In the long term, Cobalt is bound to become a fundamental resource as the EVs and electronical device market are growing every year (The number of EVs is expected to reach 250mio by 2030 compared to 8mio in 2019). Quick reminder: DRC stands for about 55% of the global raw Cobalt supply and China stands at an astonishing 80% of refined Cobalt supply. We had also seen that 8 out of the 14 main cobalt refineries are based in China.

https://www.iea.org/reports/global-ev-outlook-2020

We had seen in the previous bulletin that Canada, other than being one of the biggest Cobalt producers had built the very first North American Cobalt refinery for export and is doing mining exploration over the country in order to find new resources of Cobalt[1] and to disrupt the CHINA-DRC monopoly over the supply chain.

Image source from: https://www.visualcapitalist.com/ethical-supply-the-search-for-cobalt-beyond-the-congo/

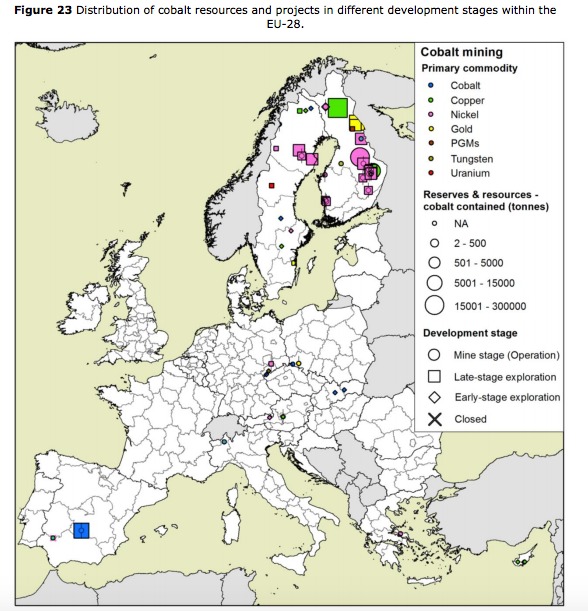

What about the EU?

If we look at the map above, we can see that the EU has refineries but not a lot of production. Its few mining areas are situated in Finland. Here is a map of the mining places and the projects put in place by the EU in order to counter the future shortage of the commodity.

https://publications.jrc.ec.europa.eu/repository/bitstream/JRC112285/jrc112285_cobalt.pdf

(Between exploration and actual start of operation, a time frame of 10 years can occur)

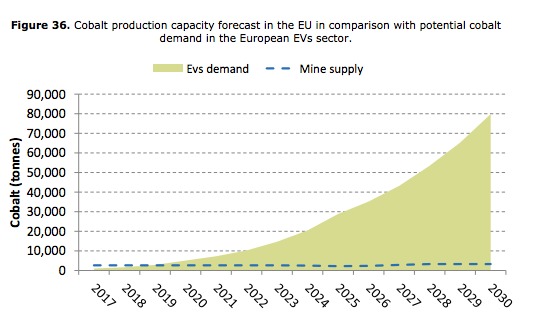

The EU cobalt demand is increasing over time and we can clearly see that it cannot supply itself currently making it highly dependent on the other suppliers.

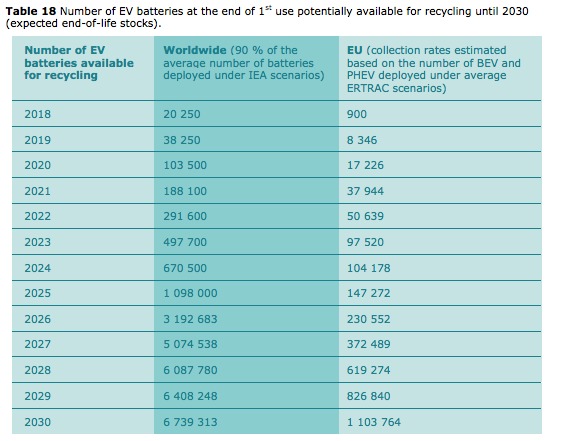

While waiting for the cobalt mining discoveries, the EU is trying to concentrate its effort in battery recycling. Right now, there is not enough old battery supply to make it really viable, but looking at the forecast of the EV market, recycling will definitely become an important source of cobalt supply. The estimate rate of used battery collection is 90%.

https://publications.jrc.ec.europa.eu/repository/bitstream/JRC112285/jrc112285_cobalt.pdf

The estimations in the table assume an average lifetime of 8 years for each vehicle battery placed on the market. The potential amounts of recycled cobalt generated from old vehicles deployed in the EU are estimated at 500 tonnes in 2025 and may amount, on average, to 5 500 tonnes in 2030. This would mean that in 2030, the recycling could provide for about 10 % of European cobalt consumption in the EVs sector (see graph figure 36 above).

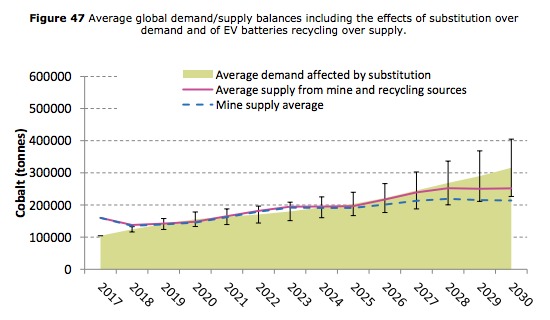

World cobalt demand may be subject to a growth rate of between 7 % and 13 % depending on the cobalt forecast usage for different areas (EVs, alloy, etc.). Between 2017 and 2030, the average cobalt consumption will amount at about 220 000 tonnes in 2025 and 390 000 tonnes in 2030. In the EU, cobalt demand will amount to 53 500 tonnes in 2025 and increasing to 108 000 tonnes in 2030.

Global

https://publications.jrc.ec.europa.eu/repository/bitstream/JRC112285/jrc112285_cobalt.pdf

Global

https://publications.jrc.ec.europa.eu/repository/bitstream/JRC112285/jrc112285_cobalt.pdf

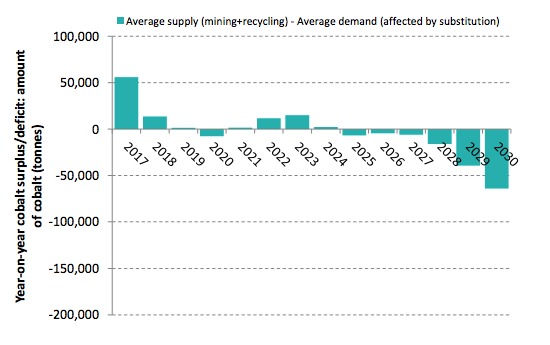

The report forecast a cobalt shortage in 5 years’ time. We can foresee an increase in the price of the Cobalt worldwide and mostly in the EU. Commodity companies such as Glencore (no1 in Cobalt mining) knowing this will surely profit to put higher margins as the product will become scarce.

Sources:

https://www.mining.com/chart-chinas-stranglehold-on-electric-car-battery-supply-chain/

https://campus.hesge.ch/commodity-trading/?p=1271

https://publications.jrc.ec.europa.eu/repository/bitstream/JRC112285/jrc112285_cobalt.pdf

https://publications.jrc.ec.europa.eu/repository/bitstream/JRC112285/jrc112285_cobalt.pdf

https://publications.jrc.ec.europa.eu/repository/bitstream/JRC112285/jrc112285_cobalt.pdf