LNG/NG Prices:

The Liquefied Natural Gas market is highly correlated with Natural Gas market trends and prices. Indeed, LNG is just NG but in a liquefied state. In other words, the amount of natural gas production, the amount of gas in storage and the volumes of imports/exports mean a great deal on the LNG global market.

Natural gas price that consumers pay is set based on two main components, which include various taxes and fees. First, you have the commodity cost itself either when it is produced or purchased. The second component are the transmission and distribution costs to move the natural gas by pipeline local natural gas distribution utilities and the cost of delivery to consumers. The shares of these two cost components vary according to natural gas market conditions.

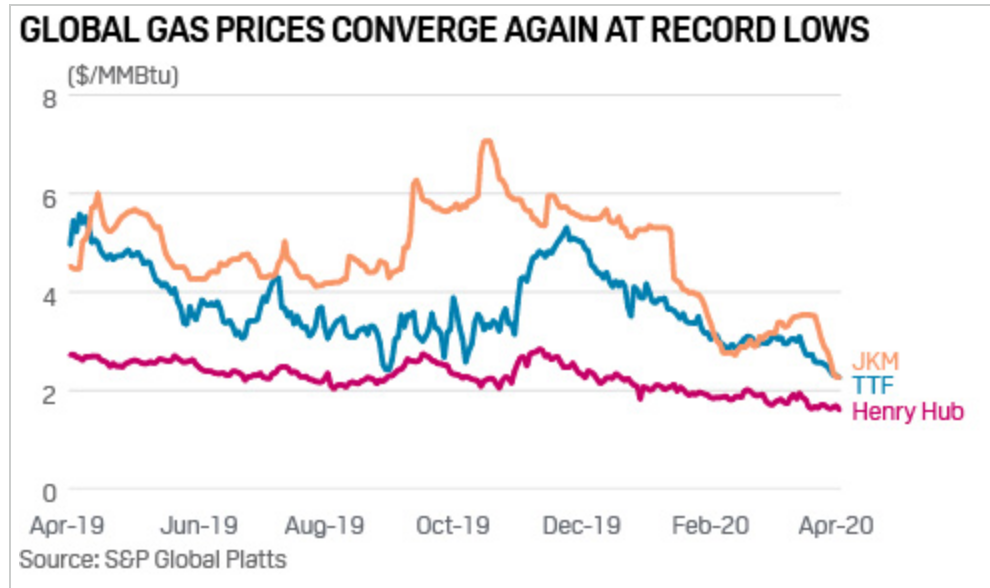

In this graph, we can observe three different price indexes:

JKM™ reflects the spot market value of cargoes delivered ex-ship (DES) into Japan, South Korea, China and Taiwan. Deliveries into these locations equate to the majority of global LNG demand.

The TTF (The Title Transfer Facility) Netherland price index is linked to the huge Groningen onshore gas field which is the center of a large pipeline network.

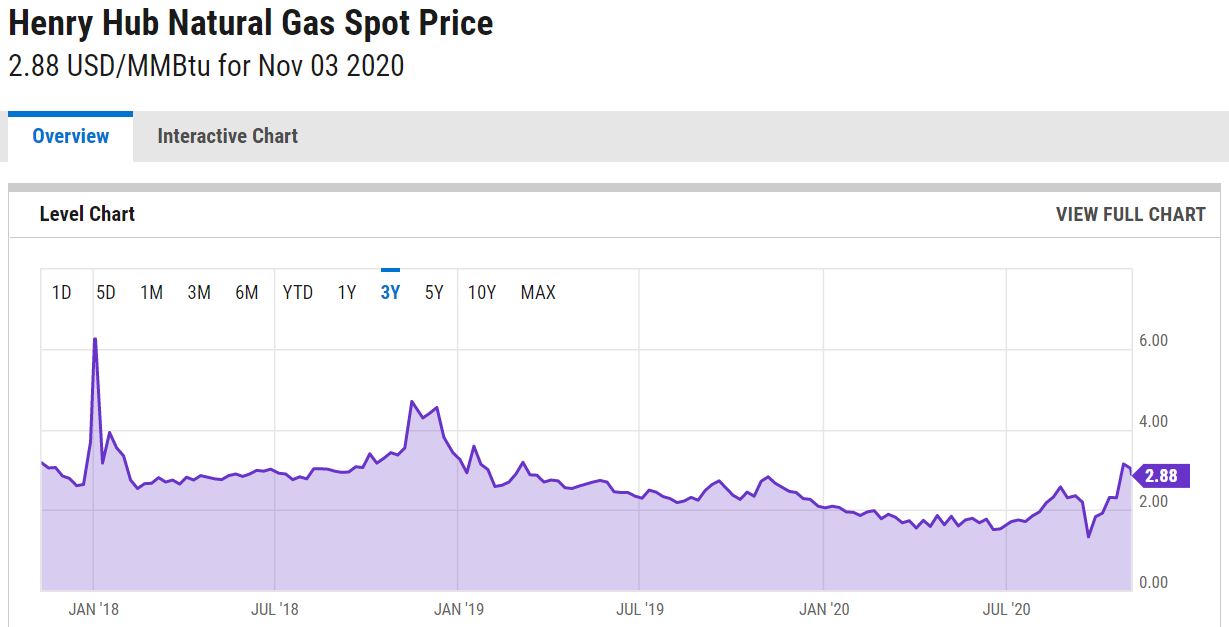

The Henry Hub price index is the US benchmark for natural gas and considered as the biggest natural gas hub.

Observation:

The JKM price refers to Japan Korea Marker, these countries are the main importers of LNG as they don’t have access to pipeline facilities. By definition, this price index is more expensive because it includes transportation costs from export countries (Australia and Qatar) highly correlated with the oil benchmark. We can observe that the two price indexes (JKM and TTF) are more volatile than the Henry Hub one.

That is to say, these indexes are linked to the seasonality and way more impacted by demand. As they are not producers, prices are not that steady throughout the year. The U.S. are big producers and exporters. Their production is close to being linear and as they export all over the world, the demand for their own LNG production does not vary that much, hence the more stable prices. Even if they have an excess of production, they can easily store it under a liquid state of matter (LNG storage facilities) or gas under depleted natural reservoirs.

We can observe on this graph the price evolution of Natural gas spots since 2018. We have to highlight the fact due to this overall unstable economic situation established with Covid pandemy, NG and LNG prices drastically decreased and reached a lowest price record achieved.

Forward Curve:

A therm (thm) equals 100’000 British thermal units (Btu).

There are many factors that can affect oil and gas prices. Some of these include the changing dynamics of supply and demand, the amount and cost of storage available, changes in interest rates, fluctuations in foreign exchange rates, the marginal cost of supply, assessment of geopolitical risk and supply shock and the market opinion and expectation and many more influences.

In this case, futures are highly dependent on seasonality of demand and result in a curve that is neither a contango or a backwardation curve but a mix of both depending on the period. We can see that the incentive in January 2021 will be to sell as much as possible whereas in August 2021, the market is telling producers to store.

Supply & Demand:

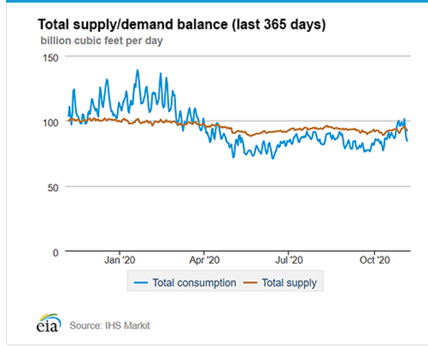

Daily supply/demand on the US market

LNG companies have been forced due to Covid19 to look for short-term contracts as securing long-term supply contracts have become a challenge. Moreover, the instability of the current economic scenario is causing LNG companies to think twice before making investment decisions. Thus, the overall situation impacted project financing and resulted in financial investment delays of several projects. Furthermore, by analyzing the graph thoroughly we understand that the level of supply is not manageable in the short term as LNG requires huge plants to be produced/extracted even though the pandemic has slowed production a bit.

Main factors of supply:

- Actual production

- Inventory storage

- Import/Export

Main factors of demand:

- Weather

- Government policy/regulation

- Petrol prices

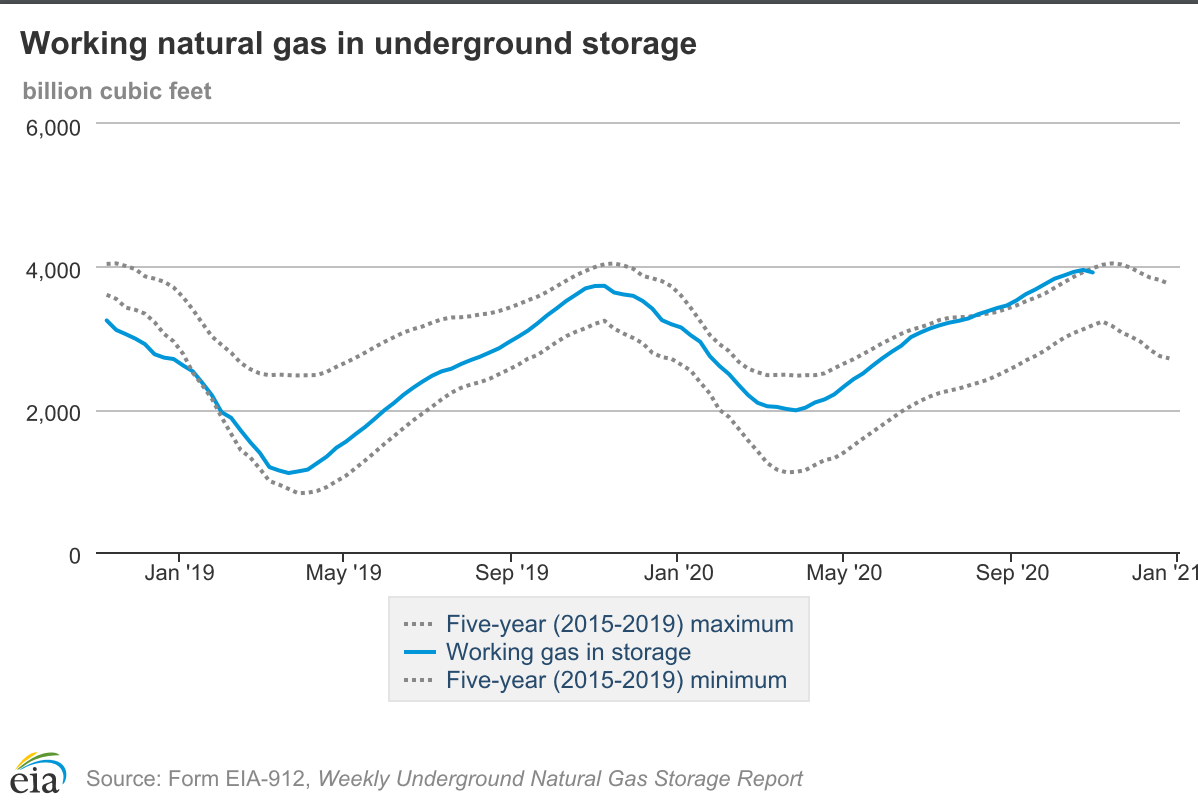

Inventory levels:

The graph above can illustrate the strategy of production and extraction of the US. Indeed, we can see that during the flat period of consumption of LNG and NG which appears during summer (April-October), they are storing the majority of their production in order to fulfil the demand beginning of the winter.

U.S. LNG Export:

The graph above represents the U.S LNG export from 2018 to 2020 Q2. We can observe that the U.S export of LNG over the year drastically increases in overall. Even though Japan is the world’s biggest importer of LNG accounting with 20% of the global consumption, we can see that South Korea is the main purchaser in the United states, South Korea were making massive effort of consuming cleaner energy (however they have long-planned nuclear and coal plants projects in the coming years-> consumption of LNG is expected to decrease over time). We can see that Korea is closely followed by Japan which uses LNG to generate nearly 40% of its power. Between Q1 and Q2 in 2020 we can see the massive drop for the U.S export globally due to the COVID-19 breakdown combined with a warmer winter affect the demand of LNG.

According to the NGSA, there are mainly 5 types of market pressure point that can influence the price of Natural Gas and thus LNG. Economy, Weather, Demand, Production, Storage are variables that have influence on market pressure. For this winter the forecast on average predict a upward market pressure in the U.S due to the following factors:

Economy: is a vital factor that influences the LNG market. For the current year, the GDP is expected to decline to -2.6 percent. Which will have a downward pressure.

Weather: The National Oceanic and Atmospheric Administration predicted an average winter 4 percent colder than last winter in the United states. This factor will affect consumption and put an upward pressure on the market.

Demand: Customer demand forecast an average 109.5 Bcf/day in 2020/2021 compared with 2019/2020 with an average of 110.6 Bcf/day . In global this will have a neutral pressure on the market.

Supply: NGSA, expected the production to decrease by substantial 9 percent. This will result in a higher price due to the fact that there is a lower supply with a constant demand.

Storage: The start of winter inventory is forecast to be 9 percent above the 5-year average with just over 4 Tcf of gas in storage, considerably more than last winter’s 3.7 Bcf levels. Higher capacity storage will result in a downward pressure on the market in the U.S.

Recommendation:

Since for this coming winter market is expected to go in backwardation with the analysis made by NGSA, we recommend to sell now and do not store the commodity. Furthermore, as we are in the second wave of the COVID-19 LNG market is becoming uncertain as every commodity we can only plan for the coming month.

Bibliography:

Gulf Coast LNG (Platts) Last Day Future | ICE, [no date]. [online]. [Viewed 12 November 2020]. Available from: https://www.theice.com/products/63127250/Gulf-Coast-LNG-Platts-Last-Day-Future/data?marketId=5531712&span=2

National Oceanic and Atmospheric Administration, [no date]. [online]. [Viewed 12 November 2020]. Available from: https://www.noaa.gov/

CHUNG, Jane, 2019. South Korea’s LNG imports to fall on new nuclear, coal plants. Reuters [online]. 31 October 2019. [Viewed 12 November 2020]. Available from: https://www.reuters.com/article/us-southkorea-lng-power-analysis-idUSKBN1XA0LJ

NGSA, [no date]. [online]. [Viewed 12 November 2020]. Available from:

Reduced LNG demand delays FIDs, 2020. LNG Industry [online]. [Viewed 12 November 2020]. Available from: https://www.lngindustry.com/liquid-natural-gas/09112020/reduced-lng-demand-delays-fids/

Natural gas prices – U.S. Energy Information Administration (EIA), [no date]. [online]. [Viewed 12 November 2020]. Available from: https://www.eia.gov/energyexplained/natural-gas/prices.php

UK Natural Gas Futures Curve, [no date]. ERCE [online]. [Viewed 12 November 2020]. Available from: https://www.erce.energy/graph/uk-natural-gas-futures-curve/

Commodity Tracker: 6 charts to watch this week | Hellenic Shipping News Worldwide, [no date]. [online]. [Viewed 12 November 2020]. Available from: https://www.hellenicshippingnews.com/commodity-tracker-6-charts-to-watch-this-week-12/

Henry Hub Natural Gas Spot Price, [no date]. [online]. [Viewed 12 November 2020]. Available from: https://ycharts.com/indicators/henry_hub_natural_gas_spot_price