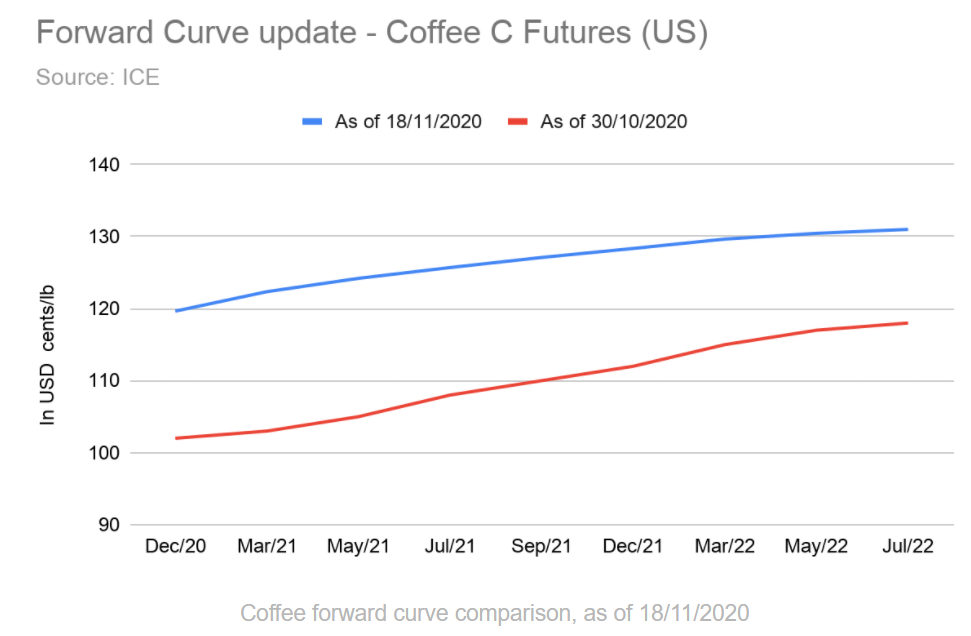

The coffee forward curve has significantly moved since the last bulletin. Indeed the price of the near term contract (DEC-20) has jumped from 102 to 119.65 cents/pound. This jump also affects the following contract, with an increase for JUL-22, from 118 to 131. This increase is believed to be due to diminished exports confirmed by the latest release of ICO report as well as increased demand from recovering economy. (ICO, 2020)

Besides, it is noticeable that the forward-curve has flattened a bit. Thus, indicating growth in immediate demand as the premium for late delivery decreases.

Cocoa

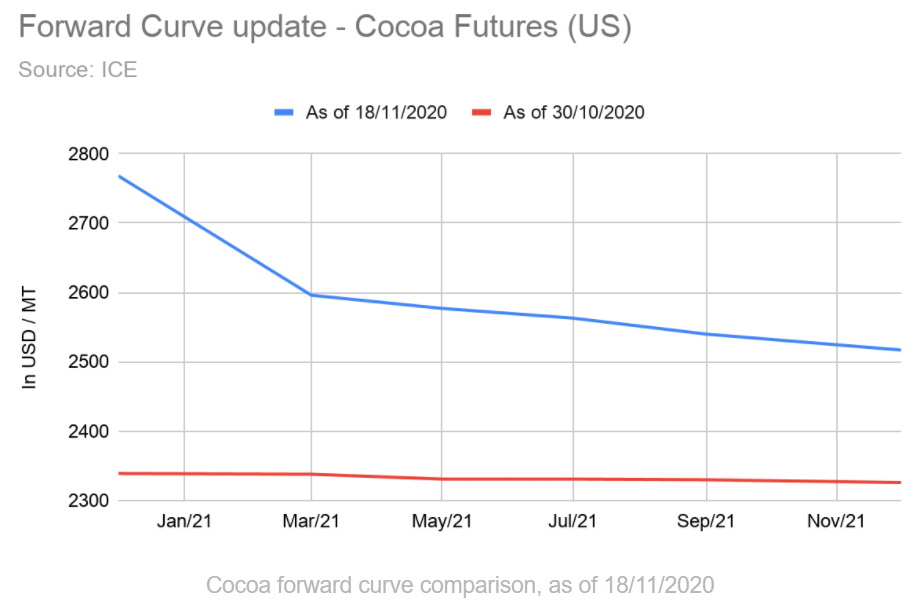

With regards to Cocoa forward curve, its shape has widely changed. It is now in a clear contango. The seasonality is probably in play here, paying a premium for immediate delivery of the recent 2020/2021 season harvest in November 2020.

Also, the overall price has increased. It can be related to the increase of farm-gate prices, decreed by Ghana and Côte d’Ivoire, as well as international recovery, knowing that exports are within predictions. (ICCO, 2020)

VSS-compliant Coffee and Cocoa

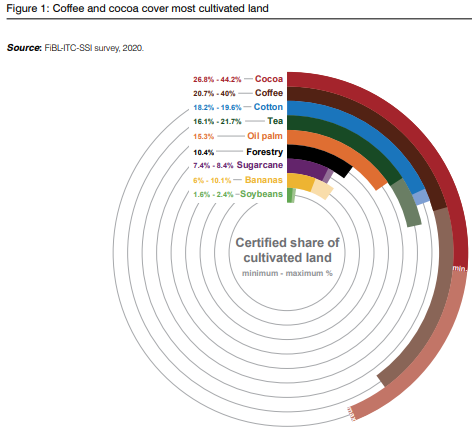

The International Trade Center recently published a report (2020) about sustainable commodities. This document highlights the increase in these last couple of years (2014-2018) of sustainably certified crop fields for several commodities including cocoa. According to the report, the demand for VSS-compliant cocoa (Voluntary sustainability standard) is rising especially in North America and Western Europe. This demand mainly comes from the desire of consumers to buy more ethical chocolate. The experts expect this trend to continue (+9.5% CAGR) until 2025 and to reach USD 620M in retail value by 2025.

Moreover, the ITC report states about Asia, to become in a not so far future “the world’s second-largest consumer market of cocoa-based ingredients” right behind Western Europe. This is bringing concerns about the capability of cocoa producers to meet the demand. Indeed, climate change and the low-yield of farmers are threatening the production of the commodity.

However, coffee is an exception to that. This commodity has seen a decrease in the estimation of the minimum area VSS certified between 2014-2018. The compliant areas decreased by 12.2% in the same given time (20.7% of global production area). This can be partially explained by the oversupply of VSS-compliant products. Research suggests the consumers in emerging economies are more price-sensitive than expected. So, the premium price of VSS-compliant coffee reduces product attractiveness. Nevertheless, data shows the demand for sustainable coffee is still growing (ITC, 2020).

Recommendation

Coffee

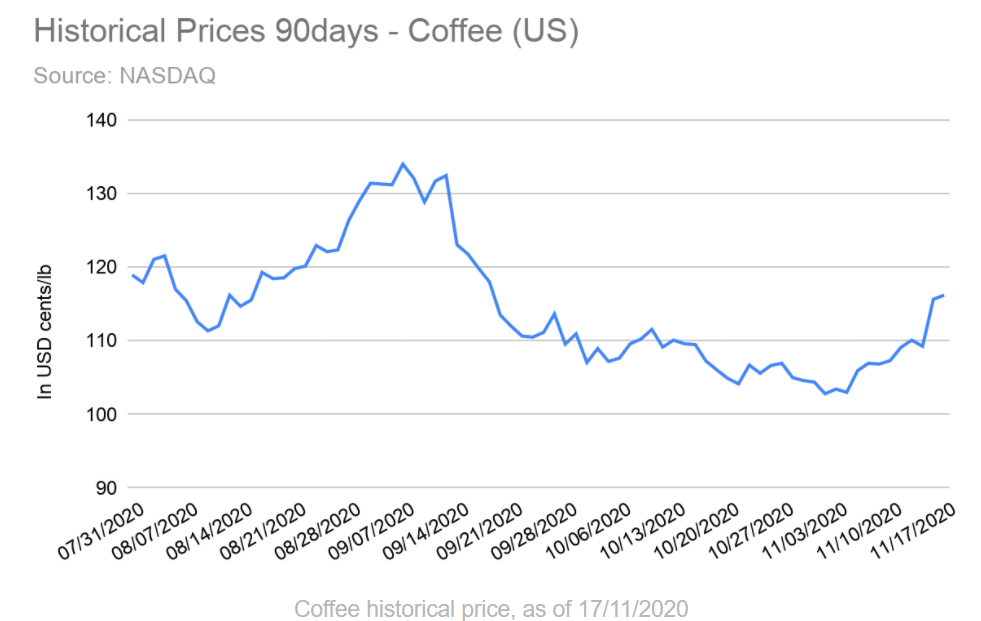

The latest results published by ICO are pushing the prices higher. The lower exports combined with the overall economic situation are impacting the short term. It is still expected that next season would hit record numbers. Therefore, we still remind cautious with coffee, as the price might soon come back to the lower tier.

Cocoa

The supply chain is impacted by the increase in farm-gate price. This premium will be mostly absorbed by intermediaries along the way. It still increases the price as production remains stable. The next report from ICCO concerning the harvest of November 2020 will provide more guidance with regards to the supply side. Therefore, we continue our forecast for a stable price of 2300-2500 USD/Ton.

Disclaimer

This publication is for your information only and is not intended as an offer, or a solicitation of an offer, to buy or sell any investment or other specific product. The analysis contained herein does not constitute a personal recommendation or take into account the particular investment objectives, investment strategies, financial situation and needs of any specific recipient. It is based on numerous assumptions

The International Trade Centre. The State Of Sustainable Markets 2020. The International Trade Centre, Geneva, 2020, https://www.intracen.org/uploadedFiles/intracenorg/Content/Publications/SustainableMarkets2020-layout_20201012_web.pdf. Accessed 18 Nov 2020.

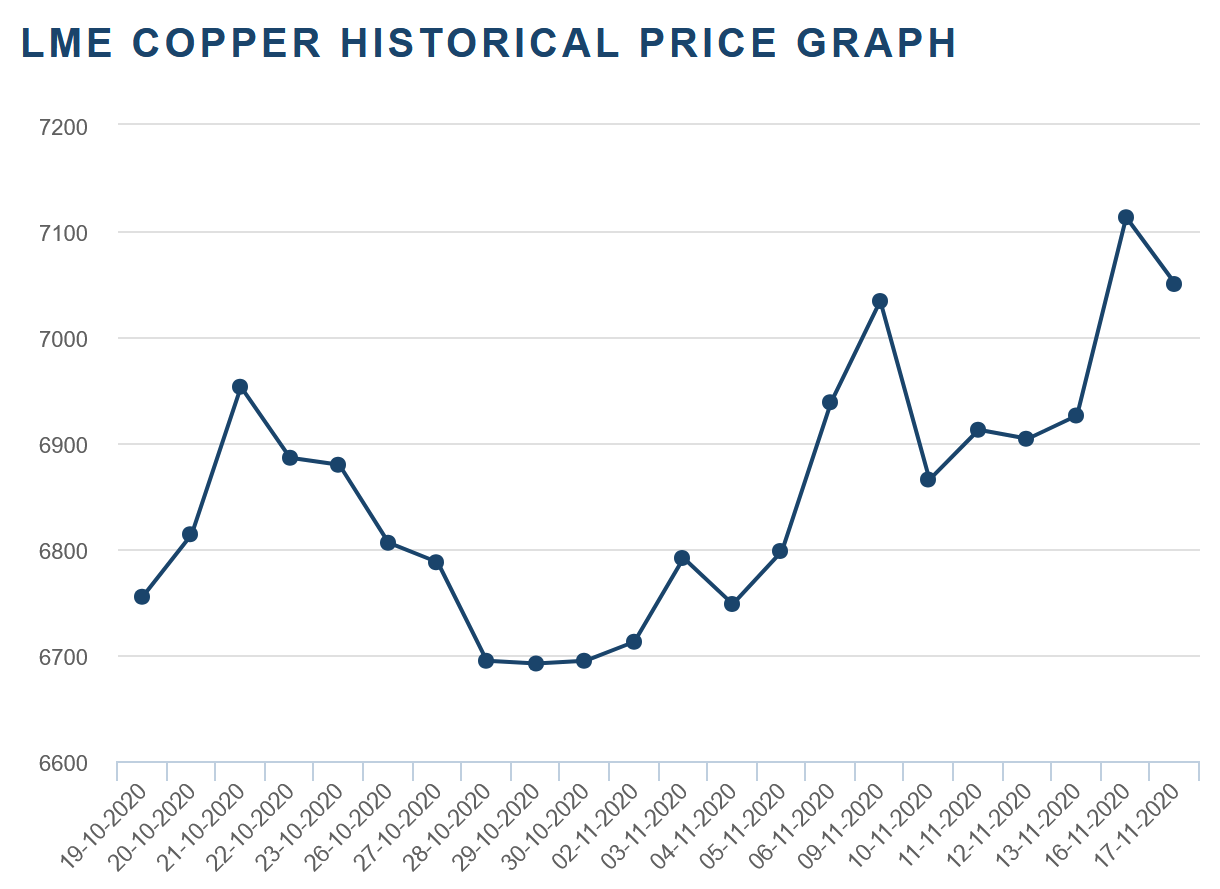

This graphic shows a certain level of volatility in the price for copper. It can be explained by the following:

The US elections have caused a certain political instability in the country which has led to a decrease of the US Dollar value. This decrease in the dollar has led to a decrease of the perceived price of copper since the commodity is mainly traded in US Dollars. Then come ups and downs showing the volatility of the US Dollar following Joe Biden’s victory and Donald Trump’s non-acceptance of this outcome.

Following the final outcome of the elections, the US Dollar has more or less stabilized but will still remain volatile as long as Donald Trump will not accept the US election results. This impacts the value of the dollar, and thus the perceived price of copper.

From a demand and supply perspective, however, demand is still in slight increase following the recovery post-first-covid-wave and supply is “late” compared to last year’s results with a 2.1% decrease in 2020 due to measures taken to decrease the spread of the virus in producing countries. However, supply is expected to catch up quickly and get back to usual levels (expectation to be shown in the forward curve below).

The graphic shows that the forward curve on the 18.11.2020 is clearly different from the one on the 29.10.2020. Since all the prices of the forwards got higher we can estimate that the market is doing better than expected. From December 2020 to February 2021, we have a contango which means that the market is expected to be well supplied for that period, followed by a small backwardation for the month of march, then the market has a contango up until December. We can conclude from that the view of the market as of today over the next year is pretty good, because the market is mostly contango which means an estimated good supply of the market over the next year.

Compared to the 29.10.2020 forwards, the period between November and January is no longer a backwardation but a contango, which means that the market view on the 18.11.2020 changed for a good supply over the next months. This can be related to the vaccine announcements made by Pfizer and Moderna.

It’s also related to the clarity over the situation of the USA, since now we have the results of the election, the dollar got stronger and more stable.

The fact that Joe Biden is elected as a president can explain the contango over the next year, that can be explained by a more stable political situation, specially with China.

ILLUSTRATION OF SUPPLY AND DEMAND / INVENTORY LEVELS

As explained in the last bulletin for copper, the stock of copper got higher due to the continuity in production and mining in the producing countries during the first wave of COVID-19. The stock from the 29.10.2020 and today dropped slowly but it doesn’t affect the market. As said before, the demand of copper is slightly increasing following the recovery after the first wave of COVID-19; yet the supply didn’t fully recover after a slow delay gained after the first wave of the virus which explains the small drop in copper inventories.

Because China is a big consumer of copper and didn’t suffer from a second wave of COVID-19, their production (and consequent need for copper) remained stable during this second wave that hit Europe and the US.

Yet this situation isn’t a sign of shortage on the market, it can be explained by a transitioning period.

Nevertheless, the price of copper is hugely impacted by the dollar stability that can explain why the stock got down a little since the dollar got weaker during the election period which might have encouraged the buy of copper.

RECOMMENDATIONS

We have a contango up until February, we advise for a strong buy in this period, to sell from February to March since we have a small backwardation, and buy in March since the year is going through a contango. We also advise buying strongly due to COVID-19 evolution many countries will start or have started already the mass vaccination which will help the economy to recover. Since copper is highly correlated with the economic activity we recommend a strong buy now.

— By Ismail MODAFFAR IDRISSI, Tashi JARON and Amélia REUSSER

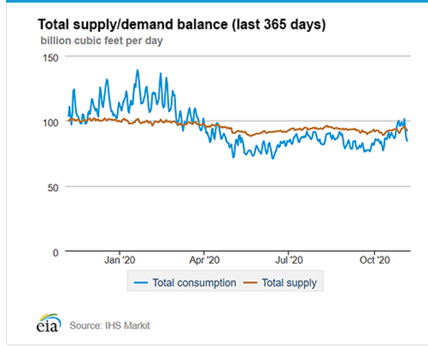

The Liquefied Natural Gas market is highly correlated with Natural Gas market trends and prices. Indeed, LNG is just NG but in a liquefied state. In other words, the amount of natural gas production, the amount of gas in storage and the volumes of imports/exports mean a great deal on the LNG global market.

Natural gas price that consumers pay is set based on two main components, which include various taxes and fees. First, you have the commodity cost itself either when it is produced or purchased. The second component are the transmission and distribution costs to move the natural gas by pipeline local natural gas distribution utilities and the cost of delivery to consumers. The shares of these two cost components vary according to natural gas market conditions.

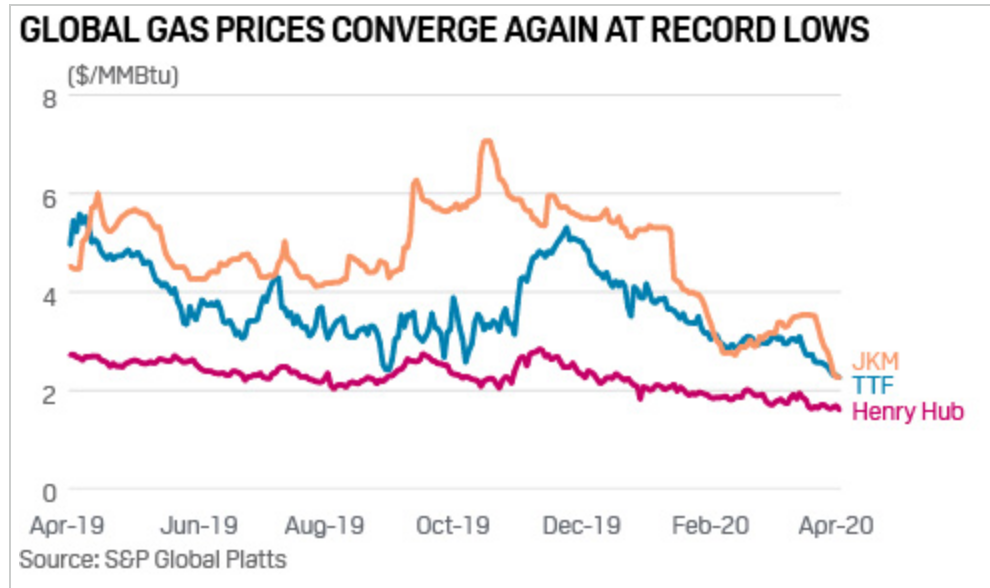

In this graph, we can observe three different price indexes:

JKM™ reflects the spot market value of cargoes delivered ex-ship (DES) into Japan, South Korea, China and Taiwan. Deliveries into these locations equate to the majority of global LNG demand.

The TTF (The Title Transfer Facility) Netherland price index is linked to the huge Groningen onshore gas field which is the center of a large pipeline network.

The Henry Hub price index is the US benchmark for natural gas and considered as the biggest natural gas hub.

Observation:

The JKM price refers to Japan Korea Marker, these countries are the main importers of LNG as they don’t have access to pipeline facilities. By definition, this price index is more expensive because it includes transportation costs from export countries (Australia and Qatar) highly correlated with the oil benchmark. We can observe that the two price indexes (JKM and TTF) are more volatile than the Henry Hub one.

That is to say, these indexes are linked to the seasonality and way more impacted by demand. As they are not producers, prices are not that steady throughout the year. The U.S. are big producers and exporters. Their production is close to being linear and as they export all over the world, the demand for their own LNG production does not vary that much, hence the more stable prices. Even if they have an excess of production, they can easily store it under a liquid state of matter (LNG storage facilities) or gas under depleted natural reservoirs.

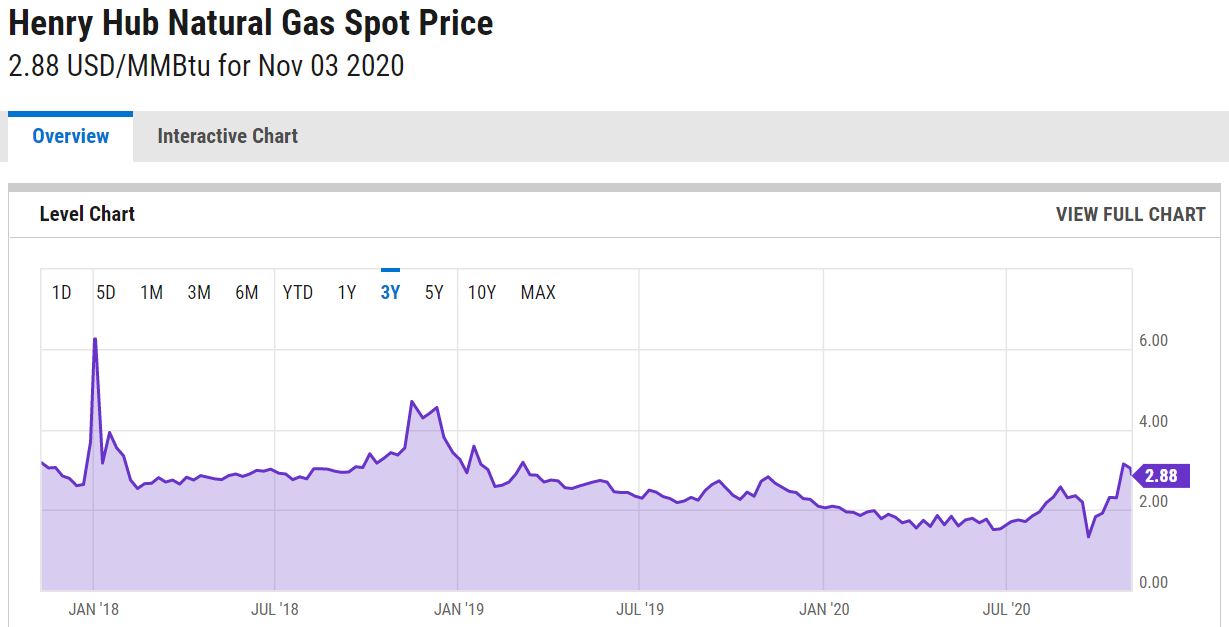

We can observe on this graph the price evolution of Natural gas spots since 2018. We have to highlight the fact due to this overall unstable economic situation established with Covid pandemy, NG and LNG prices drastically decreased and reached a lowest price record achieved.

Forward Curve:

A therm (thm) equals 100’000 British thermal units (Btu).

There are many factors that can affect oil and gas prices. Some of these include the changing dynamics of supply and demand, the amount and cost of storage available, changes in interest rates, fluctuations in foreign exchange rates, the marginal cost of supply, assessment of geopolitical risk and supply shock and the market opinion and expectation and many more influences.

In this case, futures are highly dependent on seasonality of demand and result in a curve that is neither a contango or a backwardation curve but a mix of both depending on the period. We can see that the incentive in January 2021 will be to sell as much as possible whereas in August 2021, the market is telling producers to store.

Supply & Demand:

Daily supply/demand on the US market

LNG companies have been forced due to Covid19 to look for short-term contracts as securing long-term supply contracts have become a challenge. Moreover, the instability of the current economic scenario is causing LNG companies to think twice before making investment decisions. Thus, the overall situation impacted project financing and resulted in financial investment delays of several projects. Furthermore, by analyzing the graph thoroughly we understand that the level of supply is not manageable in the short term as LNG requires huge plants to be produced/extracted even though the pandemic has slowed production a bit.

Main factors of supply:

Actual production

Inventory storage

Import/Export

Main factors of demand:

Weather

Government policy/regulation

Petrol prices

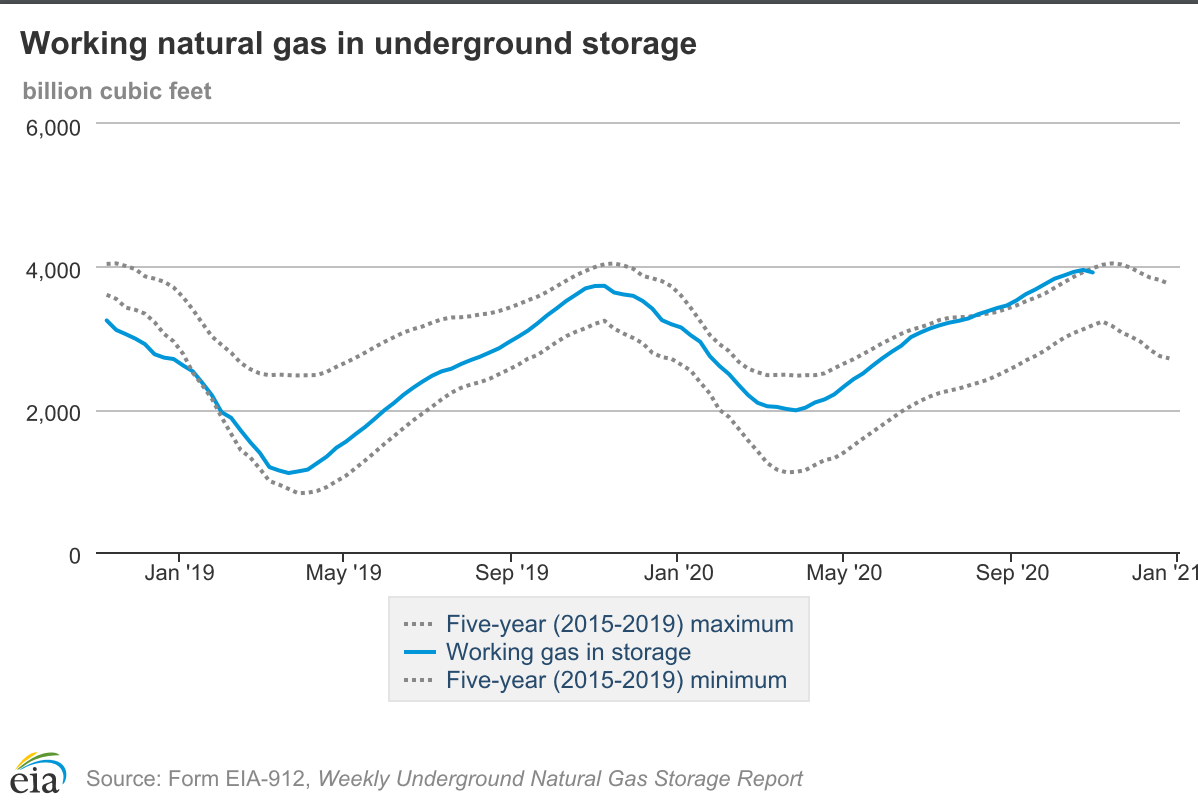

Inventory levels:

The graph above can illustrate the strategy of production and extraction of the US. Indeed, we can see that during the flat period of consumption of LNG and NG which appears during summer (April-October), they are storing the majority of their production in order to fulfil the demand beginning of the winter.

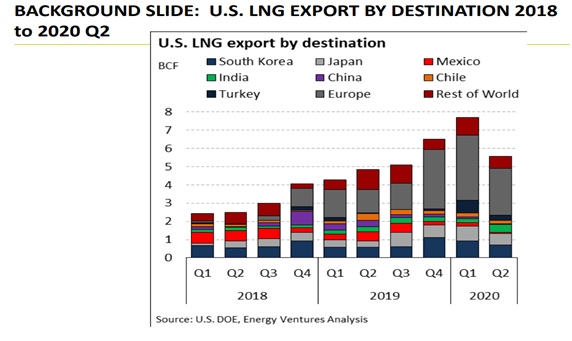

U.S. LNG Export:

The graph above represents the U.S LNG export from 2018 to 2020 Q2. We can observe that the U.S export of LNG over the year drastically increases in overall. Even though Japan is the world’s biggest importer of LNG accounting with 20% of the global consumption, we can see that South Korea is the main purchaser in the United states, South Korea were making massive effort of consuming cleaner energy (however they have long-planned nuclear and coal plants projects in the coming years-> consumption of LNG is expected to decrease over time). We can see that Korea is closely followed by Japan which uses LNG to generate nearly 40% of its power. Between Q1 and Q2 in 2020 we can see the massive drop for the U.S export globally due to the COVID-19 breakdown combined with a warmer winter affect the demand of LNG.

According to the NGSA, there are mainly 5 types of market pressure point that can influence the price of Natural Gas and thus LNG. Economy, Weather, Demand, Production, Storage are variables that have influence on market pressure. For this winter the forecast on average predict a upward market pressure in the U.S due to the following factors:

Economy: is a vital factor that influences the LNG market. For the current year, the GDP is expected to decline to -2.6 percent. Which will have a downward pressure.

Weather: The National Oceanic and Atmospheric Administration predicted an average winter 4 percent colder than last winter in the United states. This factor will affect consumption and put an upward pressure on the market.

Demand: Customer demand forecast an average 109.5 Bcf/day in 2020/2021 compared with 2019/2020 with an average of 110.6 Bcf/day . In global this will have a neutral pressure on the market.

Supply: NGSA, expected the production to decrease by substantial 9 percent. This will result in a higher price due to the fact that there is a lower supply with a constant demand.

Storage: The start of winter inventory is forecast to be 9 percent above the 5-year average with just over 4 Tcf of gas in storage, considerably more than last winter’s 3.7 Bcf levels. Higher capacity storage will result in a downward pressure on the market in the U.S.

Recommendation:

Since for this coming winter market is expected to go in backwardation with the analysis made by NGSA, we recommend to sell now and do not store the commodity. Furthermore, as we are in the second wave of the COVID-19 LNG market is becoming uncertain as every commodity we can only plan for the coming month.

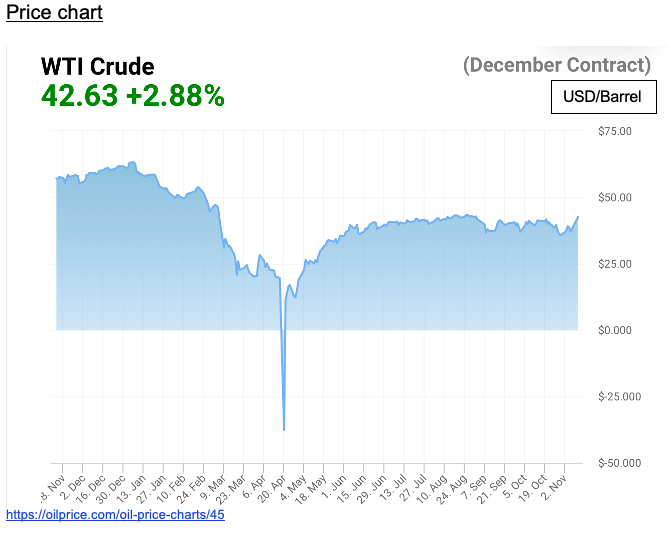

2014-2016 economic slow-down, and massive oversupply of oil by NON-OPEC countries essentially due to rising shale oil production by the US, combined with economic slow-down reducing demand for oil. Causing decrease in WTI spot price from USD105/barrel to USD36/barrel. [1]

2020 Coronavirus recession: economic slow-down reducing transport, air-traffic, affecting directly the global demand for oil which caused the price to fall drastically and for the first time, WTI trading to negative USD37/barrel. Agreement from OPEC+ to cut output by 10M barrels/day, allowed a recovery to come back positive and more or less stabilizing the price oil. [2]

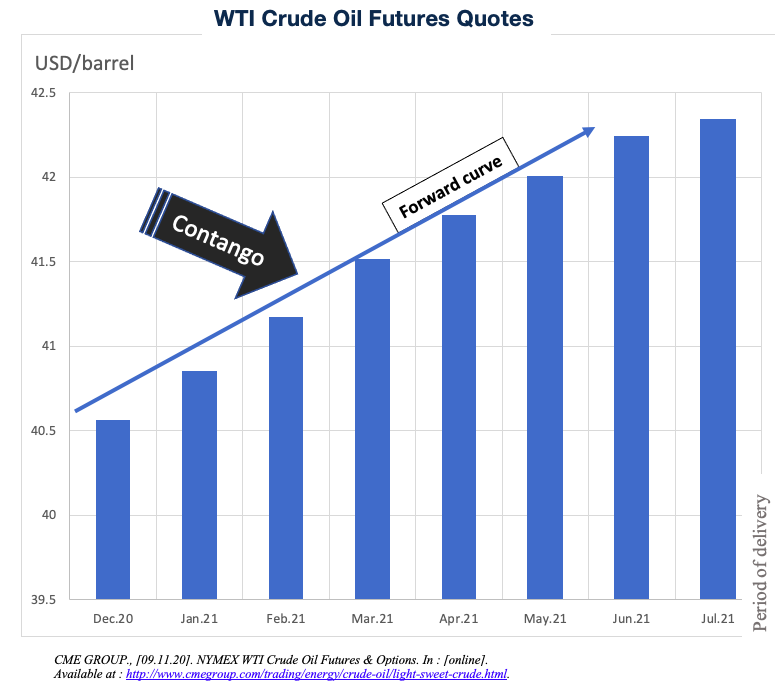

Forward curve 9.11.20

In this case the forward curve is in contango which means the spot price for delivery now is lower than today’s price for delivery in future. In other words, it means our market is relatively well supplied. Supply is greater than demand now,

In other words, today’s future contract prices for delivery today is lower than prices for delivery in future.This can be explained by the fact thattoday’s prices for future delivery include: Storage and finance cost.

The contango situation could be explained by the recent cut in oil production from OPEC+ and also the short recovery of the economy by the expected announcement of a potential vaccine. [2]

Supply and demand dynamic – Inventory levels [3]

Oil changed due to its fundamentals[3]

30th October: Oil rigs increase by 10 in the US. It’s used to happen when the market is doing well. OPEC increased its supply by releasing its weekly production per member[3]

3rd November: American Petroleum Institute announced for Inventory level a large drawdown of 8millions barrels. This lack in supply makes price increase[3]

4th November: Energy Information Administration’s weekly crude oil inventory announced another drawdown of 8milions barrels. [3]

Election in the US affect the oil market because of different points of view between Trump and Biden. Trump supports the current oil production and Joe Biden wants to invest USD2 trillion in green energy which doesn’t help the oil market. Politics and coronavirus created uncertainty because people don’t know if there’ll have a vaccine or lockdown. [3]

Recommendations:

On Monday, oil prices increased after the announcement of a vaccine effective at more than 90% against the coronavirus by Pfizer. With markets looking forward to the potential end of the pandemic sometime next year, optimism returned in a big way. We can already see that crude oil had its best day in months, rising more than 10%. The growth has contributed to significant increases in the share prices of many oil companies. [5]

Even though, compared to early November where the price was at $37.14 and now raising to $42.59 per barrel (price today for delivery in december) the recommendation is to be long (buy) for the next 3-6 months. Since with the announcement of the vaccine the future consumption of oil will tend to rise and the market being well supplied will be contango and therefore meaning that the price will be higher month after month in a year’s time to reach maybe the prices of last year. (Nov 2019 $57.03 and Jan 2019 $63.12). [5]

A decrease in oil price could result in an opportunity to produce more cotton at a lower price as the shipping and harvesting parts are high oil consumers. We can clearly see how the worldwide lockdown in March has lead to a huge drop in cotton’s prices.This crash is explained by the economy worsening off, and customers are less likely to buy cotton-based items. Furthermore, countries may have stopped stockpiling which could have led to artificially inflated prices that we had during the earliest month of 2020. Government policies and sustainable programs trying to shield the farmers and textile industries could have a big impact on production costs and may cause this uncertainty. Bad weather in some regions also influenced cotton prices, especially when there are drought periods as this year, which produce an automatic decrease in the price because of production issues.

After this crash, we can see that the price of cotton slowly recovered to the same level than before the pandemic, this may be explained by the countries trying to relaunch their economy by easing their restrictions on population. However, we can see that the price dropped again in October-November which could be linked to the current situation where many European countries re-entered in a lockdown.

Available from: https://tradingeconomics.com/commodity/cotton

Supply and demand dynamic of the commodity:

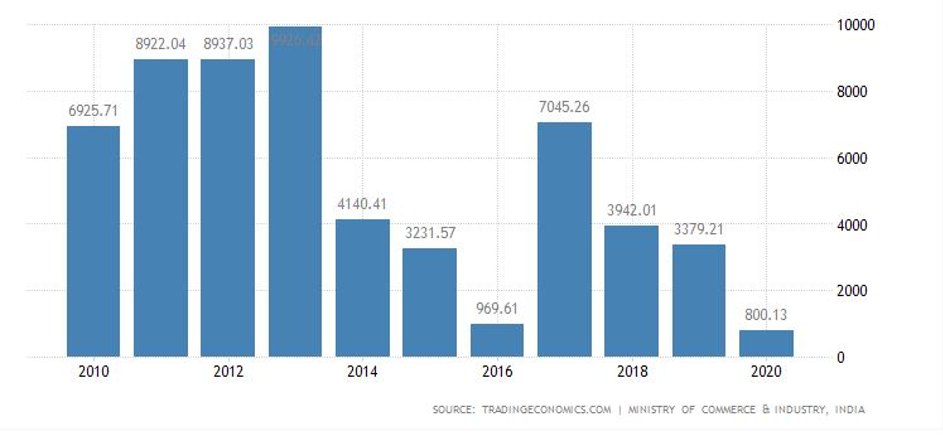

On a global scale until the end of 2019 the exports of cotton were stable. But in 2020 the cotton industry has been hit hard by the Covid-19 pandemic, large cotton producer such as India has seen its exports decreased to 800.13 USD Million in 2020 against 3379.21 USD Million in 2019.

According to the World Trade Organization, the World (based on available data for countries and represents 90% of world trade) cotton exports in March 2020 decreased by 12.5% while it decreased by 34.6% in April 2020 compared to the same months in 2019.

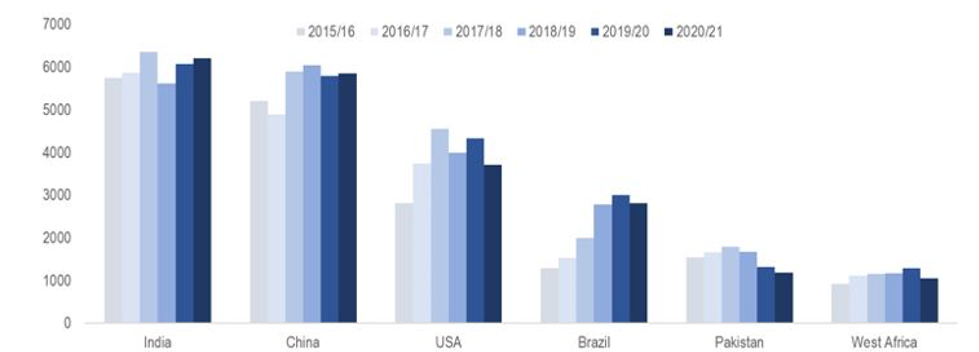

In contrast we can see that the cotton production has been more or less steady in India, China and USA but Brazil has seen a growth in its production since 2017 because the state of Mato Grosso has started to heavily grow cotton. It went from approximately 2000 tons to 3000 tons in a year. The cotton supply chain suffers from Covid, trade tensions and weak global economy and this is why most of the producing countries will see their production decrease for the 2020/21 projection.

Production Changes in Major Regions from 2015/16 to 2020/21 (tonnes per country)

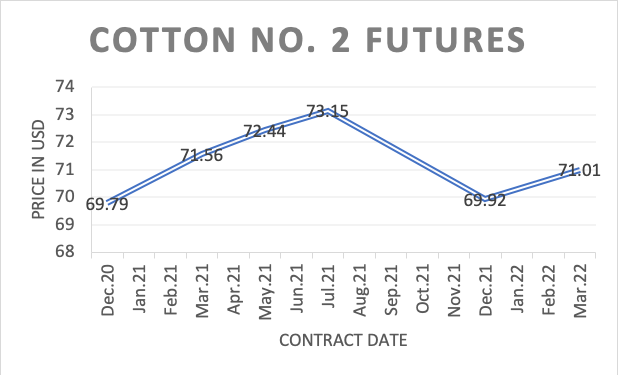

The cotton futures prices are going to be on the rise until July 2021 (73.310). Right now we are in a contango situation (Price on the 9th of Novembre 2020 : 69.0) and it may go further up with the lesser uncertainty surrounding the COVID-19 pandemic but we can also see a trend from December to July the price is on the up it’s in correlation of the harvesting periods of the different producers.

As long as the Coronavirus will remain active across the world, the demand should stay week. Indeed, due to this current situation, it becomes hard to shop due to the active lockdowns in several countries and a lot of people became unemployed. Therefore, the demand for cotton should remain week in the next few months while the supply is projected to outpace demand by 500’000 tonnes. Our recommendation for the next months will be to buy in order to make a profit by selling three months later.

Cobalt futures are traded in the London Metal Exchange (LME). The LME works closely with the Fastmarket MB, which is an international specialist and publisher of information about the global steel, non-ferrous and scrap metal market.

Forward curve for the LME Cobalt (Fastmarket MB) from Sept.2020 (they didn’t release the OCT. and NOV. yet). Prices are in USD per MT compared to the other Cobalt physical price which are in Tonnes (1000kg)

The forward curve graph shows a contango situation. As previously mentioned in class, a contango situation means that the futures price of a commodity is higher than the spot price. In the case of our Cobalt graph, the slope shows that the market is stable and nothing dramatic is affecting it. The almost straight line shows that the futures price is directly linked to the price of cobalt plus its cost of carry each and every month.

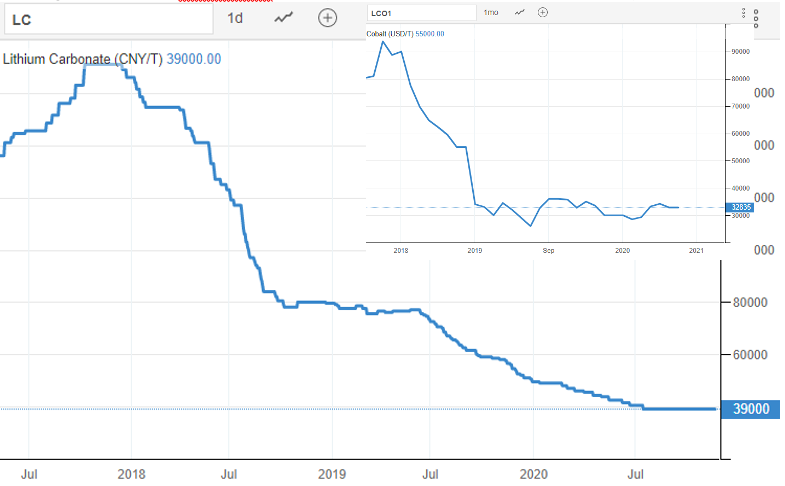

The LME only started to trade Cobalt in 2010, so this is the furthest we can go historically. Today (11.11.20) the price of Cobalt is 32’835$/T. What is interesting for Cobalt is what happened in the past: if we look at the graph, we can see that in 2018, the price went up to 95’000$/T, which is almost 3 time of today’s price. The reason behind this is especially because of a huge jump in EVs market growth between 2016 and 2018. The International Energy Agency (IEA) projected that by the end of the current decade, the EVs being used on roads would triple to reach 13 million in total and that by 2030, we would see about 125 million vehicles. Such growth projections have spurred very strong demand for lithium-ion batteries, which we know now, use cobalt for the batteries’ cathode components. Let us remember that such batteries are used not only on EVs but on smartphones, like the iPhone, PCs and so on. The demand had been then very anticipated to grow rapidly over the coming decades[1]. This created a high demand for cobalt, pushing the price higher and higher. This phenomenon inspired the miners to mine more in order to capitalise on higher price. What happened next was an increase in mining for cobalt: DRC, which stands for more than 60% of the global Cobalt mining, was suddenly mining a lot more to catch up with the demand, by the increasing creation of local artisanal mines. Moreover, Glencore, was building a massive cobalt mining infrastructure in Katanga, DRC ( https://goo.gl/maps/H4WmTGEJMy36d6GBA ), which would increase global Cobalt supply to 26’000tonnes/y[2]. These sudden supply rush created an oversupply in the market which pushed the price down.

On top of that, something that contributed to the crash was that Tesla, the leading company for EVs, stated in 2018 that they were “reducing cobalt content” in their new batteries for the next cars[3].

Another point was that Chinese manufacturers were stockpiling cobalt by buying more than needed, thinking that prices would keep going higher every month. They finally ended up buying less after the price dropped because they already had stocks.

All these points contributed to the 70% price crash that occurred in 2018-2019.

The price is still much correlated to these points but there were not such a high price up to today. In the graph below, we can see that price drop in March is very much correlated to the Coronavirus pandemic, which slowed the industry down.

We can see that in the second part of the year, the price resurged because of the summer de-confinement and restart of the businesses but also an increase due to the several news of the EV market. If we look at Tesla and Nio stock price, it sky rocked after news on new batteries technology (1mio mile Tesla battery[4][5).

Lithium has no futures contract yet but the LME, partnering with Fastmarkets MB, is projecting on creating the very first one, the LME lithium Hydroxide CIF futures contract, in H1 2021 (first half of the year), so we will have to wait for the Forward/futures curve.[6]

The lithium market is also much linked to the EV market and other consumer electronics. If we look at a historical price from the same dates as cobalt above (in the small graph), we will see the same trends:

This is the chart of lithium Carbonate 99.5% LiCO3, battery grade, spot price China. Warning: this chart is in ChineseYuan/tonne (39’000CNT = 5890.70USD dated 12.11.20)

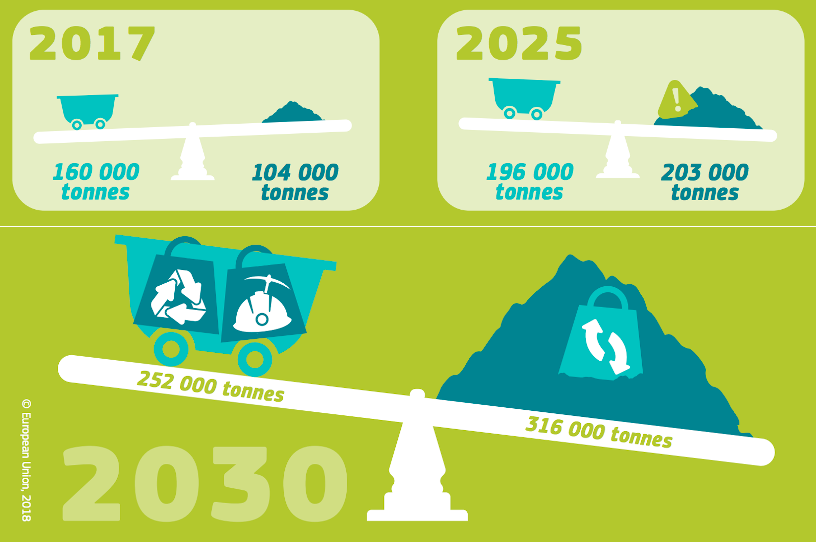

Cobalt is a main component used to produce batteries. The biggest growth in the batteries sector will come from electrical cars. The sector is forecasted to grow from 3.2 million electric vehicles in 2017 to 130 million by 2030. The forecast is that by 2030 65 percent of cobalt demand will be needed for the electrical cars market. Additionally, the growth in the electrical cars industry will be heavily influenced by different countries’ regulations.

Supply and demand dynamics

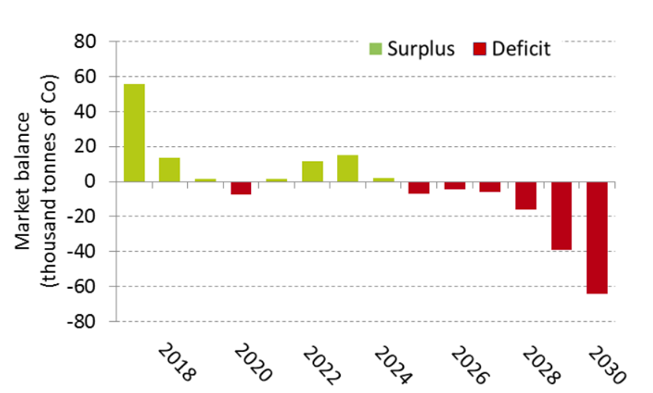

The European Commission published a rapport in 2018 where they forecasted how the supply and demand dynamic of cobalt will evolve.

The forecast states that we will experience a shortage of cobalt by 2025. The deficit will keep on growing. Their study shows that even by adding back into the supply chain recycled cobalt, the forecast is that by 2030 the supply of cobalt will be short of 66 000 tonnes.

What is being done to try to remedy the situation?

In the European Union the focus is on battery recycling and additional mining activities. Together they could increase endogenous supply, which could then cover about 15 percent of the European electric-vehicle sector demand in 2030.[7]

Australia is also expected to become an important cobalt-producing country, potentially accounting for 14 % of the world production in 2030. Today, 55 percent of the world production comes from the Democratic Republic of Congo.

And tesla in all this?

On September 22, Tesla held its annual meeting of shareholders and battery day. Tesla’s CEO promised all kinds of battery improvements geared at reducing costs per KWh, increasing range and lowering investment per GWh. Despite the company’s efforts to eliminate cobalt, many still believe the battery metal will be needed for some time to come. However, one thing is for sure the cobalt supply chain is critical and if new batteries without cobalt in them aren’t created soon, the world will run out of cobalt pushing the price of all electronic devices and electrical vehicules upward.

Inventory levels

China & COVID-19

China’s refiners, which dominate global output of cobalt are heavily reliant on material that comes from Democratic Republic of Congo mines via ports in South Africa. COVID-19 lockdowns in southern Africa have created bottlenecks, delaying cobalt shipments from Zambia and the Democratic Republic of Congo.[8][9]

China’s state stockpiling agency has drawn up plans to buy 2,000 tons of cobalt after the coronavirus pandemic highlighted the fragility of supplies of the strategic mineral. Bloomberg stated that the National Food and Strategic Reserves Administration in China could put its purchasing plan into action by the end of this year, according to two people familiar with the matter. The move is in response to supply disruptions from top producer, the Democratic Republic of Congo, and is in line with China’s future economic and strategic needs. [10]

3. Recommendations to be short (sell) or long (buy) for the next 3 or 6 months.

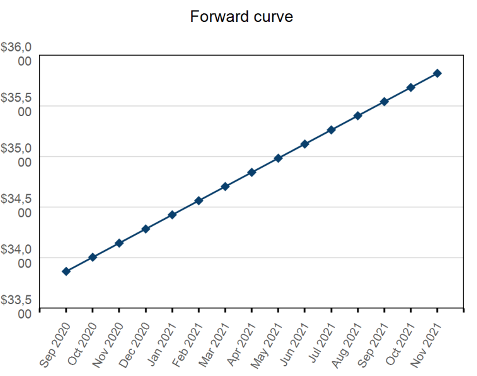

As far as it concerns the cobalt commodity, we can see that the forward curve is a contango. This is showing us the market as seen today. The Prices for future delivery is higher due to cost of carry and interest. Historically, cobalt production has been consistently growing in the last 50 years and in any event, accelerating since the 2000’s. The price has additionally been increasing. However, it has been firmly impacted by supply (crisis in DR Congo) and demand (from Asia) interruptions. China being the largest consumer, it’s been found that Lithium and cobalt refineries have sufficient inventories to sustain their production for the time being, with lithium refineries particularly well-stocked due to raw material overstocked in 2019.[11]The sharp increase in the demand was largely driven from Chinese consumption and EVs but also aerospace industry for whom the cobalt is an essential irreplaceable element as well as within power generation with gas turbines using cobalt. These all reasons explain the high demand for cobalt. Therefore, the demand would be much higher than supply meaning the producers will be increasing the price due to shortage of supply. In addition, looking at supply side, much before the year 2020, critical metals, such as cobalt and lithium, were growing concerns because of the uncertainty over their reliable supply for the technology and renewable energy industries.[12] Furthermore, it would give incentives to firms like Apple and Tesla securing their supply by investing directly in processing and mining or acquiring critical metals mines.[13] So, in the case of cobalt the message and recommendation is to go ahead and store.

Price in USD per bushel (60 pounds) From May 28 2020 to November 6 2020 source: Macro trends

China is the biggest importer of Soybeans and since the number of Chinese pigs is increasing in China, more soybeans are purchased in order to feed them. China is concerned about the COVID-19; thus, they have decided to increase its stock of soybean in order to not experience a shortage. The price increases since the demand has increased rapidly and the supply is decreasing. China imports principally soybeans from Brazil but when the supply is running low in this region, China buys them from the US.

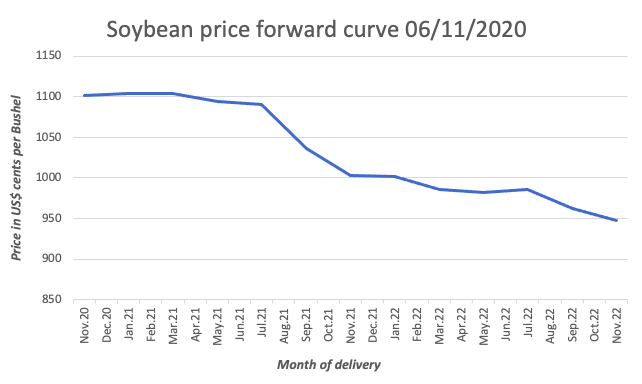

FORWARD CURVE

source: CME Group

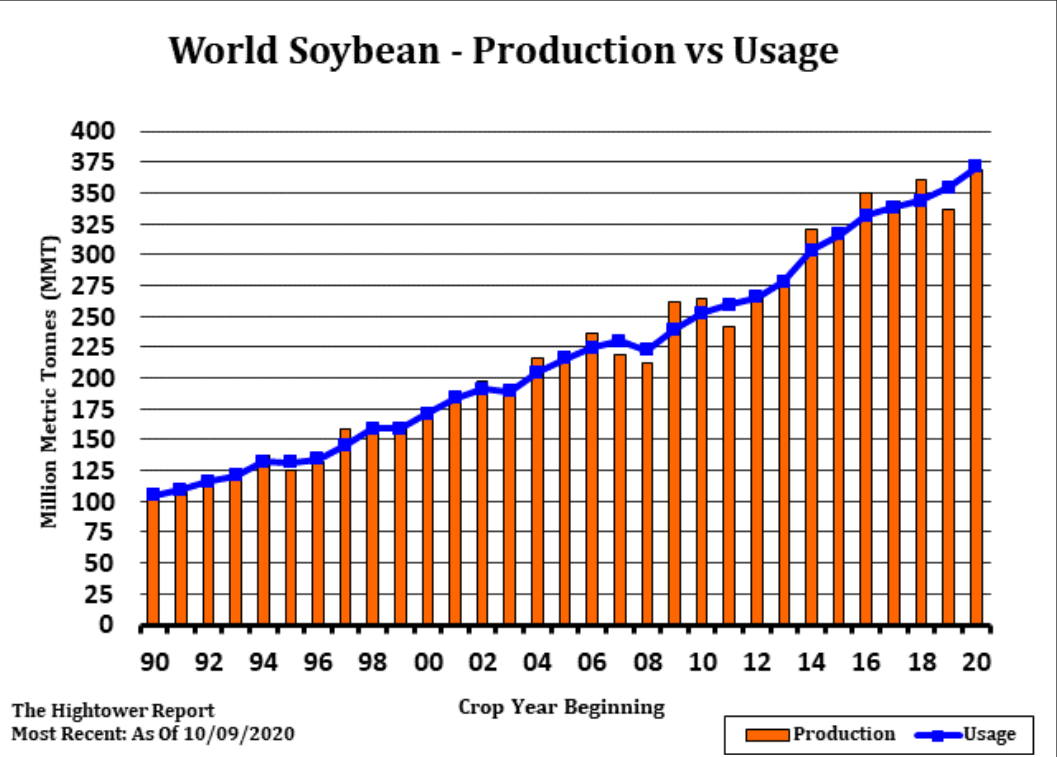

As we can see, the forward curve is generally inverted. This trend can be explained by the weather concerns in South America. Irregular rainfalls caused by the La-Nina phenomenon could cause a shortage due to a decrease in productivity, which would explain why buyers are willing to pay a premium for delivery now. Furthermore, the demand for soybean is high due to Chinese mass pig farming. It is forecasted to go up to 2,7 million of bushels for the marketing year 20-21, while it was 2,4 million of bushels for marketing year 19-20. SUPPLY & DEMAND CHART

source: CME Group

As we can see the supply and demand are in constant increase since the 90s. As populations, income levels, and urbanisation expand worldwide, the demand for soybeans is boosted. Another major soybean trade driver is the different governments policies. The 3 main drivers of soybean’s supply are weather, protein demand and Chinese demand.

What is interesting is the 2018-2019 decrease. It coincides with the start of the US-China Trade War which led to a decrease in production. Nowadays the situation got better and China started to import from the US again.

On the demand side, China is the biggest importer. The recovery of China’s pork industry from the African swine fever has stimulated imports in 2020. Mainly because soybean is used as a source of feedstock in animal production.

INVENTORY LEVEL (STOCK) CHART

source: CME Group

Brazil and the U.S. are the main soybean exporters and there have been supply issues in both countries. Due to COVID-19 Brazilian supplies have been limited.

Due to drier conditions in Brazil and Argentina, the future supplies might be lower. Dry conditions have negatively affected U.S. yields as well.

RECOMMENDATIONS

The Chinese economy is back to normal and there is a forecasted increase in demand. Therefore, importers are ready to pay a premium for delivery now as the supply is uncertain given the weather conditions coupled with COVID-19. Moreover, China imports first from Brazil and then from the US, since the harvest season happens at the beginning of the year in Brazil and at the end, in the US. From an importer’s point of view, we would recommend it to be long over the next few months as the supply will remain low.

REFERENCES

A Supply Drop and Demand Pickup Pushed Soybeans to a Three-Year High, [no date]. [online]. [Viewed 10 November 2020]. Available from: https://www.spglobal.com/en/research-insights/articles/a-supply-drop-and-demand-pickup-pushed-soybeans-to-a-three-year-high

Blog: World Soybean Production Projected to Rebound, 2020. IHS Markit [online]. [Viewed 10 November 2020]. Available from: https://ihsmarkit.com/research-analysis/blog-world-soybean-production-projected-rebound.html

SAEFONG, Myra P., [no date]. Why soybeans may be headed for their highest price in 6 years. MarketWatch[online]. [Viewed 10 November 2020]. Available from: https://www.marketwatch.com/story/why-soybeans-may-be-headed-for-their-highest-price-in-6-years-11600450312

Soybean Reports – CME Group, [no date]. [online]. [Viewed 10 November 2020]. Available from: https://www.cmegroup.com/content/cmegroup/en/trading/agricultural/soybean-reports.htm

USDA ERS – Major Factors Affecting Global Soybean and Products Trade Projections, [no date]. [online]. [Viewed 10 November 2020]. Available from: https://www.ers.usda.gov/amber-waves/2016/may/major-factors-affecting-global-soybean-and-products-trade-projections/

China’s Oct soybean imports jump 41% on year on swine fever recovery | S&P Global Platts, 2020. [online]. [Viewed 10 November 2020]. Available from: https://www.spglobal.com/platts/en/market-insights/latest-news/agriculture/110720-chinas-oct-soybean-imports-jump-41-on-year-on-swine-fever-recovery

Chinese 2019-20 soybean imports to total 88 mil mt, up 6% on year: USDA | S&P Global Platts, 2020. [online]. [Viewed 10 November 2020]. Available from: https://www.spglobal.com/platts/en/market-insights/latest-news/agriculture/021220-chinese-2019-20-soybean-imports-to-total-88-mil-mt-up-6-on-year-usda

Soybean Futures Quotes – CME Group, [no date]. [online]. [Viewed 10 November 2020]. Available from: https://www.cmegroup.com/content/cmegroup/en/trading/agricultural/grain-and-oilseed/soybean_quotes_globex.html

Soybean Futures Quotes – CME Group, [no date]. [online]. [Viewed 10 November 2020]. Available from: https://www.cmegroup.com/trading/agricultural/grain-and-oilseed/soybean_quotes_globex.html

Soybean Prices – 45 Year Historical Chart, [no date]. [online]. [Viewed 10 November 2020]. Available from: https://www.macrotrends.net/2531/soybean-prices-historical-chart-data

TAN, Huileng, 2020. Soybean futures have been surging on Chinese demand, trade group CEO says buying could continue. CNBC [online]. 10 September 2020. [Viewed 10 November 2020]. Available from: https://www.cnbc.com/2020/09/10/soybeans-have-been-surging-on-chinese-demand-and-purchases-could-continue.html

Group 3 – K Maxime DOLLA, Mahona PENNA, Romane POUCHON

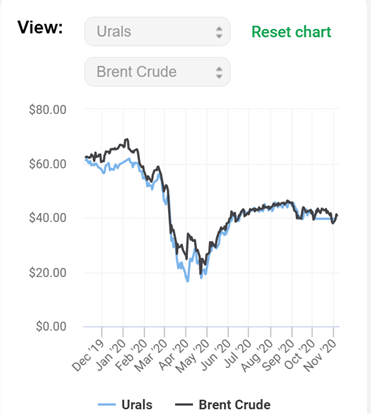

The price of oil fell more sharply in March 2020 than in 2018. The covid-19 health situation has created uncertainty about demand, which has declined globally as a result of lockdowns that have limited the mobility and operation of economic activities, as well as overproduction caused by Russia’s refusal to cut production and Saudi Arabia’s increasing production to drive prices down until April. However, in May, prices rose significantly due to the recovery in business activity, a decrease in production, and inventories, as demand exceeded supply.

Then, in September and October, uncertainty about the second wave of covid-19 and the return of Libyan production caused prices to fall despite reductions in supply and increased Chinese imports.

Finally, there was great volatility at the beginning of November, affected by the American election and the possibility of maintaining the current OPEC+ restrictions.

The events that will be important to follow are the meetings of the OPEC + on 30 November and 1st December which will discuss the measures to be taken to stabilise oil prices.

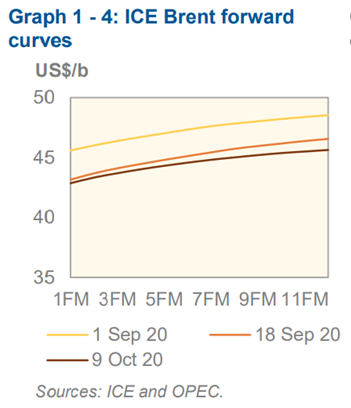

Forward curves

The events that will be important to follow are the meetings of the OPEC + on 30 November and 1st December which will discuss the measures to be taken to stabilise oil prices. As far as the forward curve is concerned, the market is currently in a contango situation, which is getting stronger due to demand predictions.

Supply and Demand dynamic of the commodity:

As for all the oil industry on these troubled times, the Russian industry has been affected as well by the covid-19 pandemic. According to Russia’s energy minister, Alexander Novak, the global oil demand could fall by 9 to 10 million bpd because of the pandemic. Exports are still going down, causing Russia to call for a global response regarding the oil demand crisis. As matter of fact, the fuel demand went down by 30%, this may also be caused by a sudden decrease of trucking activity. The situation is most likely not going to get any better, considering that a lot of countries are again taking drastic measures to limit transit through countries and even within their own territories. This will again lower oil products demand, as less will be needed, be it for plane, car, or even boat.

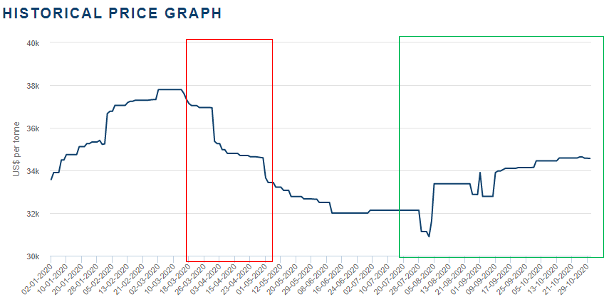

The following graphs shows the Russian oil production, and how it drastically drops in 2020, mostly due to the global pandemic of covid-19

Russian oil production. Source: TakeProfit.org

Finally, Russia’s crude oil supply going down may also be explained by the OPEC+ deal. This deal aimed to limit the commodity production, by reducing it by 7.7 million bpd and so increase oil price, by limiting its supply. The deal was to be eased starting January 2021, by limiting the production by 5.7 million bpd instead of 7.7 million. However, the situation probably won’t improve, as a second wave of covid-19 arises, and Russia is asking to extend the deal to March 2021, without reducing the production cut by the planned 2 million bpd, and keeping it as intended instead.

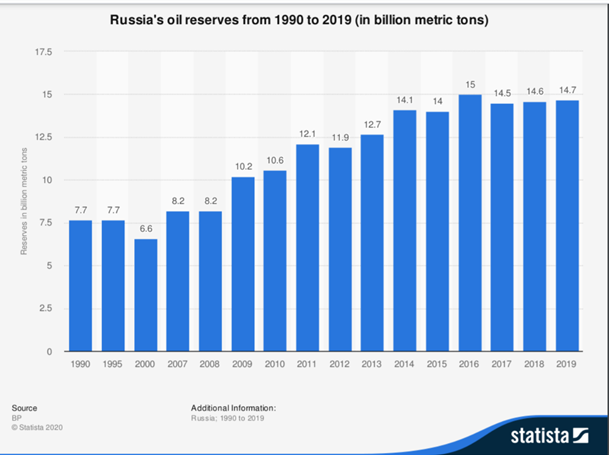

Russian oil reserves:

As for Russian oil reserves, the graph below shows what amount they possessed up until 2019. Its reserve were of 14,7 billion metric tons in 2019, amounting to 6% of the global oil reserves. However, the reserves dropped these last month, in fact, it dropped by almost 10 million metric tons from June to August. If this trend keeps on going, Russia’s oil reserves should keep going down. However, there is an oil supply deficit, and if the situation gets better, the oil market could recover from this pandemic quite quickly.

Source: Statista

Recommendation:

The situation being extremely unstable due to the covid-19 situation, it is hard to make good predictions, but demand should still keep go down because of the second wave, considering this, it would be better to be short for the upcoming months. Then, crude being at a low, and the market in contango, it might be an interesting choice to be long on the long run. In fact, if all the measures taken by the OPEC+ are indeed efficient in limiting supply, and demand also increases, the market should improve, and oil prices go up.

“Oil Recovery Expected to Falter Though Supply Glut Shrinks”. Consulté le 3 novembre https://www.wsj.com/articles/oil-recovery-expected-to-falter-though-supply-glut-shrinks-11602664747

“Oil Prices Close Higher After Volatile Session”. Consulté le 3 novembre https://www.wsj.com/articles/oil-prices-slide-to-five-month-lows-as-lockdowns-hit-demand-11604325947

“OPEC and Russia study deeper oil cuts – two sources”. Consulté le 4 novembre https://www.reuters.com/article/opec-algeria/opec-and-russia-study-deeper-oil-cuts-two-sources-idUSKBN27J27X

https://www.opec.org/opec_web/en/311.htm. Consulté le 4 novembre

https://www.opec.org/opec_web/en/publications/338.htm (monthly report p.5). Consulté le 4 novembre

“Russia’s Novak says 2020 oil demand could fall by up to 10 mln bpd”. Consulté le 1 novembre https://energy.economictimes.indiatimes.com/news/oil-and-gas/russias-novak-says-2020-oil-demand-could-fall-by-up-to-10-mln-bpd/77942150

“OPEC and non-OPEC allies urge ‘full conformity’ with production cuts as oil prices falter”. Consulté le 2 novembre https://www.cnbc.com/2020/09/17/opec-meeting-saudi-russia-review-oil-output-cuts-amid-demand-concerns.html

“Russia Discusses Three-Month Extension Of OPEC+ Oil Production Cuts”. Consulté le 3 novembre https://oilprice.com/Latest-Energy-News/World-News/Russia-Discusses-Three-Month-Extension-Of-OPEC-Oil-Production-Cuts.html

“Russian Oil Minister: Global Oil Inventories Are In Decline”. Consulté le 3 novembre https://oilprice.com/Energy/Crude-Oil/Russian-Oil-Minister-Global-Oil-Inventories-Are-In-Decline.html

https://www.statista.com/statistics/264390/oil-reserves-in-russia-since-1990/ Consulté le 3 novembre

By Lyticia Wouguia, Christopher Delfin and Piratharsan Poologanathan

Price movement recap

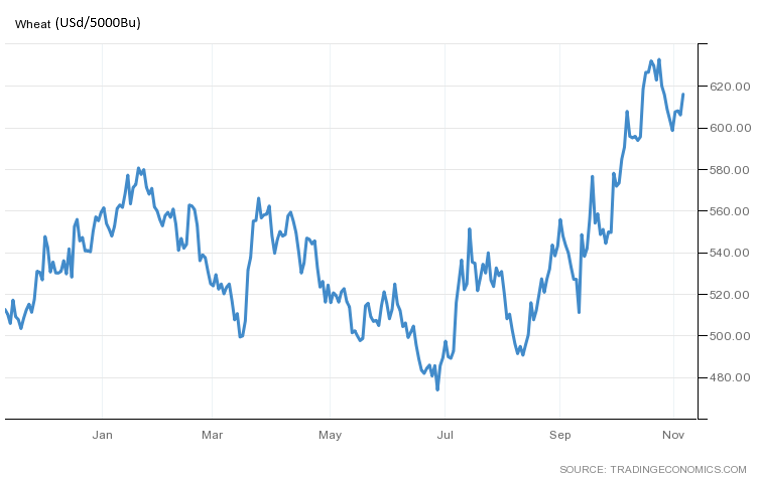

The graph above represents wheat prices of the year 2020. To begin with, due to the outbreak of COVID-19, some major commodities have been highly affected. However, wheat has seen minimal direct impact from this pandemic. This is because wheat has a relatively stable demand and is considered one of the most inelastic commodities. But, by looking at the first part of the pandemic outbreak (Feb-April), prices are dropping continuously due to disruptions in demand from the worldwide lockdown. Meaning also that there are less exports and less production happening. Then, there is a peak by mid-March which is due to new harvests from farmers. Furthermore, coming at the end of the year, prices are rising as there is a continued reduction in production in the EU and the Black Sea due to scorching weather and this is a big risk for tighter supplies in those nations that dominate the international export market.

Supply & demand

By reaching the end of the year, USDA forecast world wheat production at 768.48 MT in 2020-21. A difference of 4.17 MT from 764.32 MT in 2019-20 which is the current record. Overall, the EU, Ukraine and the United States will be producing and export less as they will be facing unfavorable weather conditions. Meanwhile, Argentina, Australia and Canada and some Asian Countries will have better performances as exporters.

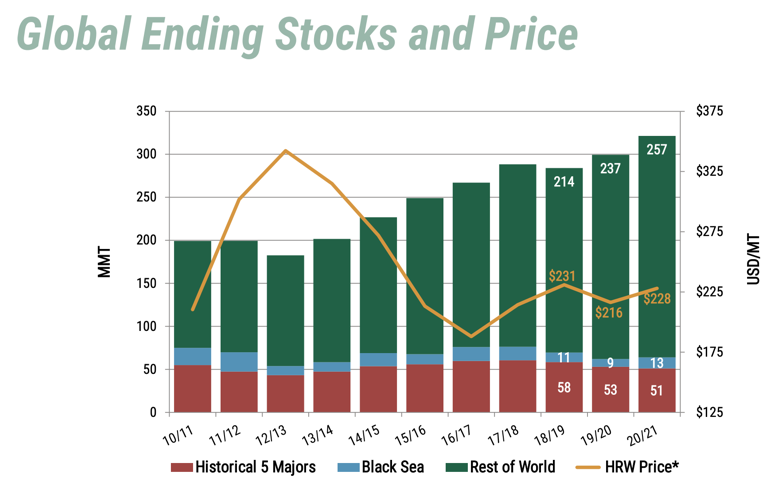

In addition, due to the second wave of the virus, countries are focusing more on domestic consumption rather than foreign trade, which also increases their own wheat stocks. As seen below, world ending stocks is at 321MT and half of these stocks is held by China, around 163MT. Regarding the influence of the Covid-19 pandemic and the panic buying of long-term storage food products, such as pasta, has not greatly affected the demand curve worldwide. It has only affected local demand at small fluctuation.

Here below is a graph:

Global ending stock has a major effect on the supply. As you can see on the graph below, the ending stock is increasing each year. This increase is explained by the fact that China and India have increased their stock due to the government’s encouragement through subsidiaries. However, as we can see on the graph the price tends to increase, because China and India do not export wheat.

Chicago SRW Wheat Futures Quotes

The Chicago soft red wheat, which is the largest wheat derivative, the futures are above the spot price. We can observe that today the market is not supposed to lack in production, and it will stick to the growing demand.

Recommendations

Due to the seasonality that the wheat market depends on, the price varies a lot on the harvest period or. Actually, we are facing here, a normal curve from December to March, and then the price stays stable till May and finally decrease. This cycle seems to repeat itself on year 2021 and 2022. In an investment perspective for the next 3 months, it is in the best interest to store.

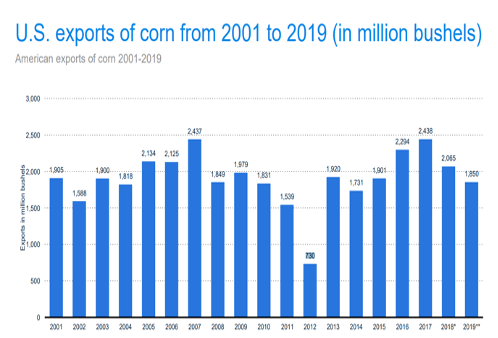

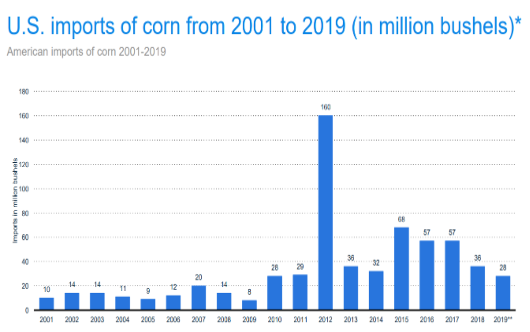

-#3 In 2012, there was severe dryness in the USA, (USA, largest producers and exporters, had to import 5 times more than the 2 previous years. The importation was 160 million bushel against 28-29 million in 2010-2011.

Source : statista, from USDA, economic research service.

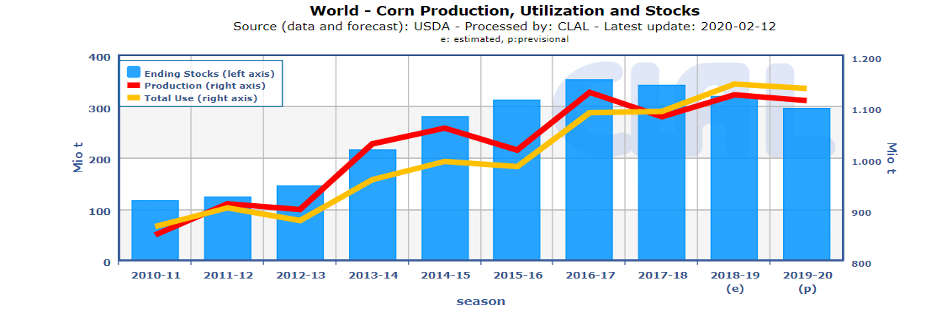

-#4 Between 2012 and 2017, the production was higher than demand and at the same time stocks were increasing resulting in low prices. Since 2017, demand has become higher than supply. To satisfy this demand, it was necessary to use the stocks. Therefore, the stocks decreased and it explains that the impact on price was quite low.

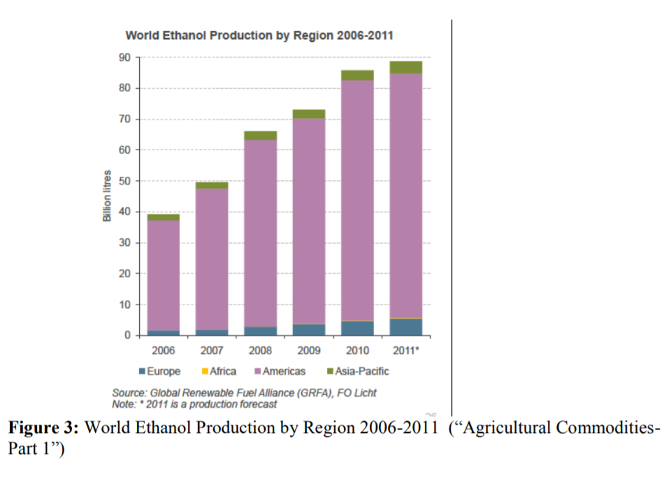

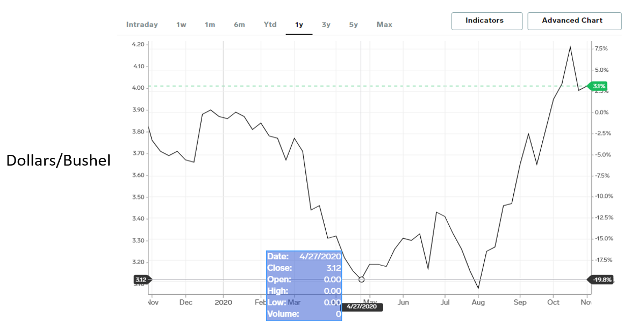

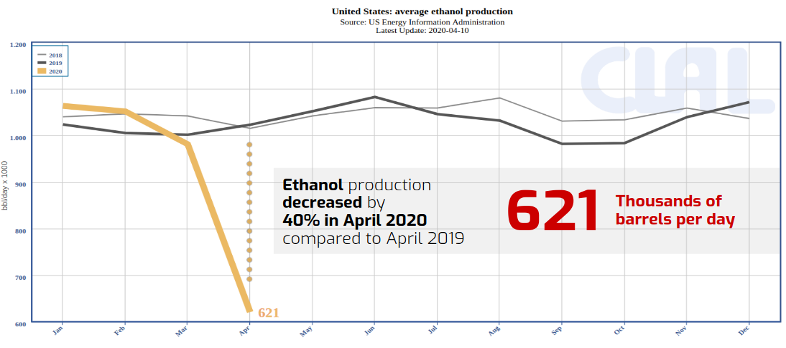

On this chart we can see that the price collapsed in the first months of the year, mainly caused by the covid-19. The lockdown in many countries led to a collapse of diesel and gasoline demand and ethanol is no exception. The production has fallen and decreased by almost 50%. And we know that more than 1/3 of corn production is used to make ethanol. After that, we can see that the price started to increase linked to the end of the first wave of covid-19. And when we approach August the price tends to increase. The explanation is climate in the US; a storm in Iowa (the main state to produce corn in the US) has damaged the crop. We can also add the low rainfall in the corn belt during the month of August. All these events have affected the quality and the quantity of corn.

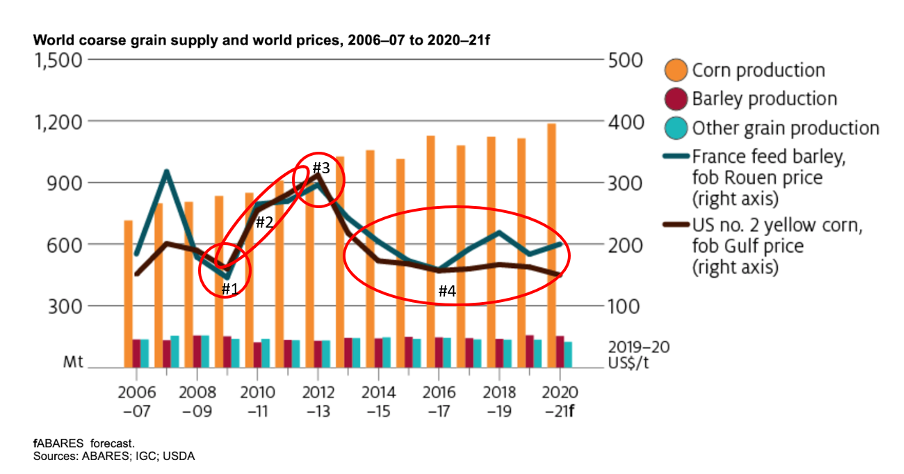

The world price of corn is forecast to drop by 8% to US$150 per tonne in 2020-21, representing the lowest price since 2006-07. The fall in the price is due to a record global planting and expectations of record average yields. The mixed outlook for demand due to the COVID-19 pandemic worsened the impact of record production on prices.

Global production

Global corn production is expected to reach 1.2 billion tonnes in 2020-2021, an increase of 6.5% over the previous year. Corn production is forecast to reach record peaks in the United States and Brazil. An almost record production is also forecast in China, backed by favourable seasonal conditions.

Global demand

Because of the ongoing COVID-19 impact, the global demand outlook for corn remains unclear. As a consequence of COVID-19 measures, industrial and food use of corn is expected to decline in 2020.

Also due to COVID-19 impacts on travel, the use of corn for bioethanol in the United States decreased by 8 % compared to the previous year.It is also expected that the use of corn as food will have decreased over the COVID-19 period, due to ongoing disruptions to the food service industry.

On the other hand, despite the ongoing impact of COVID-19, the use of corn as animal feed is expected to increase.

As we are still in this COVID-19 period and potential future waves of it still represent a big risk for the industrial and food use of corn.

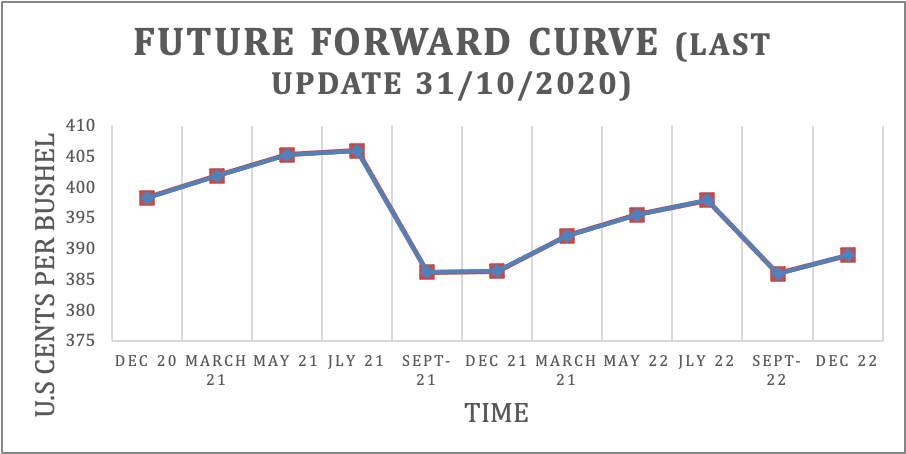

From December ‘20 to July ‘21, it is a normal curve. Then, it goes into an inverse curve until September ‘21. From September ‘21 to july ‘22 it goes into a normal curve again and then falls into an inverse curve and goes back to a normal curve again. We can see a pattern here. Indeed, it is a normal curve (the market is well supplied) but always drops into an inverse curve between July and September which is due to the harvest period for the two main producers, USA and China. Prices reflect the seasonal breakdown of supply.At this time, the supply/demand is in favor of demand.

From December to July, the message is to store because the demand doesn’t need as much. From July to September, the message is to deliver (don’t store) because the demand is willing to pay for it.

Recommendation

We prefer to give a recommendation for 3 months because of the uncertainty due to COVID-19. Indeed, the situation is constantly changing. The recommendation is to go short for the 3 upcoming months based on the price’s forecast.